Most taxpayers panic when they receive an income tax notice. However, receiving a notice does not automatically mean tax evasion or wrongdoing. Today, the Income Tax Department uses advanced technology, artificial intelligence, and data-matching systems to monitor financial transactions. Information from banks, employers, stockbrokers, mutual funds, registrars, crypto exchanges, and foreign reporting systems is automatically compared with the details reported in your Income Tax Return (ITR). As a result, even a small mismatch between your return and the department’s records can trigger a notice.

In this guide, we explain:

Why income tax notices are issued

The technology behind notice generation

The 8 most common notice triggers

Different types of income tax notices

Real-life case studies

Steps to avoid notices altogether

How Does the Income Tax Department Know About Your Financial Transactions?

Many taxpayers assume the department only sees information that they declare in their tax return. That is no longer true. The modern tax system relies on multiple reporting mechanisms that automatically collect and process financial data.

The Income Tax Data Flow

Banks, Brokers, Mutual Funds, Registrars, Employers ↓ Form 61A / SFT Reporting ↓ Income Tax Insight Portal ↓ Annual Information Statement (AIS) ↓ Taxpayer Information Summary (TIS) ↓ Form 26AS ↓ Central Processing Centre (CPC) ↓ Income Tax Notice

Because of this automated system, taxpayers often receive notices before any manual assessment takes place.

Understanding AIS, TIS and Form 26AS

Annual Information Statement (AIS)

AIS acts as your financial transaction ledger.

It contains:

Salary income

Interest income

Dividend income

Mutual fund transactions

Share transactions

Property purchases

Foreign remittances

Tax payments

AIS provides the department with a complete picture of your financial activities.

Taxpayer Information Summary (TIS)

TIS is a simplified version of AIS.

It:

Removes duplicate entries

Consolidates income categories

Generates accepted values

Supports ITR pre-filling

The TIS is often the actual dataset used by the department while processing returns.

Form 26AS

Form 26AS remains the primary tax credit statement.

It includes:

TDS

TCS

Advance tax

Self-assessment tax

A common mistake taxpayers make is relying only on AIS and ignoring Form 26AS.

When there is a conflict, Form 26AS generally takes precedence for tax credit verification.

High-Value Transactions That Can Trigger an Income Tax Notice

1. Mismatch Between ITR and Form 26AS

One of the most common reasons taxpayers receive notices is claiming TDS credit that does not appear in Form 26AS.

This often occurs due to:

Incorrect PAN reporting

Delayed TDS filings

Employer reporting mistakes

Bank reporting errors

The CPC automatically compares all claimed credits with Form 26AS records.

How to Avoid It

Always perform Form 26AS tax credit verification before filing.

2. AIS Income Not Reported in the ITR

AIS records many income sources that taxpayers often forget.

Examples include:

Savings account interest

Fixed deposit interest

Dividend income

Capital gains

Bond interest

If AIS shows income that is missing from your return, a mismatch notice may be generated.

How to Avoid It

Review AIS thoroughly before filing your return.

3. Changing Jobs During the Financial Year

Employees who switch employers frequently receive notices due to underreported salary income.

This happens when:

Salary from previous employer is omitted

Form 12B is not submitted

Standard deduction is claimed twice

The department combines salary information from all employers.

How to Avoid It

Disclose salary from every employer while filing your return.

4. Incorrect Deduction or Exemption Claims

The department actively reviews deductions under:

Section 80C

Section 80D

Section 80G

HRA exemptions

Unusually high claims often attract scrutiny.

How to Avoid It

Keep supporting documents for every deduction claimed.

5. Excessive Refund Claims

Large refund claims are automatically subjected to risk assessment.

The department may seek additional evidence before releasing the refund.

How to Avoid It

Ensure all refund claims are backed by accurate calculations and supporting documents.

6. High-Value Transactions Not Supported by Declared Income

The department compares:

Income reported in ITR

SFT transaction records

AIS information

If a taxpayer reports low income but purchases property, mutual funds, or makes large cash deposits, the system may flag the discrepancy.

How to Avoid It

Maintain proper documentation showing the source of funds.

7. Failure to Report Foreign Assets

Resident and Ordinarily Resident taxpayers must disclose foreign assets in Schedule FA.

Examples include:

Foreign bank accounts

US stocks

RSUs

ESOPs

Overseas real estate

Failure to disclose can attract severe penalties.

How to Avoid It

Report all foreign assets even if they generated no income.

8. Misreporting Cryptocurrency Transactions

Crypto transactions are now monitored through:

Section 194S TDS reporting

Exchange reporting

AIS integration

Taxpayers who fail to disclose crypto gains may receive notices.

How to Avoid It

Report all transactions in Schedule VDA.

Income Tax Notices by Taxpayer Type

Salaried Employees

Common triggers:

Salary mismatch

Incorrect HRA claims

Undeclared interest income

Freelancers

Common triggers:

Bank credits exceeding declared receipts

Foreign remittances

Presumptive taxation mismatches

Business Owners

Common triggers:

GST turnover mismatch

Cash deposits

Inconsistent profit margins

Investors

Common triggers:

Capital gains omission

Dividend mismatch

Mutual fund transactions

NRIs

Common triggers:

NRO interest income

Non-filing despite TDS deductions

Foreign asset disclosure issues

Crypto Investors

Common triggers:

Missing VDA schedules

Incorrect gain calculations

Unreported exchange transactions

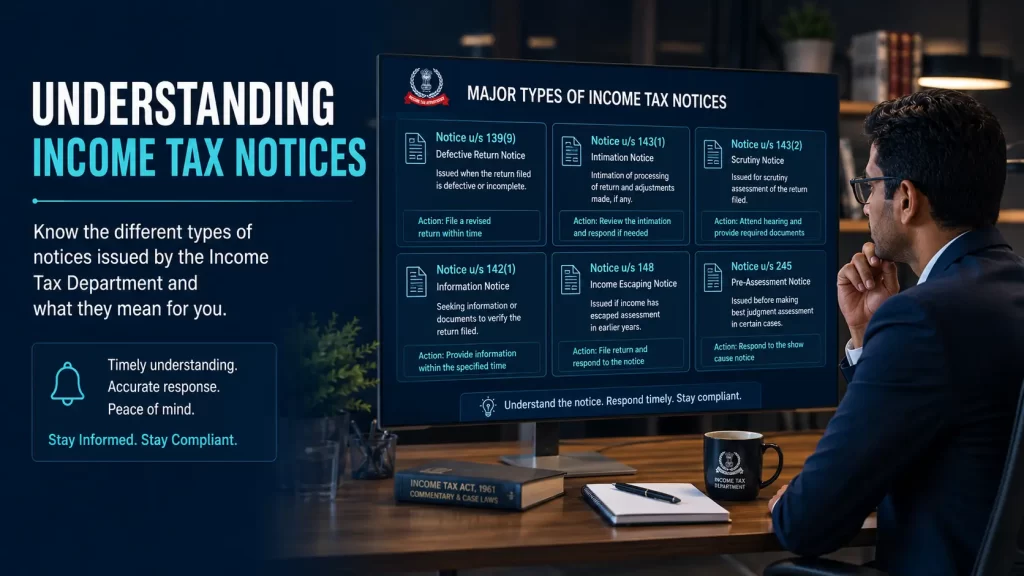

Major Types of Income Tax Notices

Section 139(9) – Defective Return Notice

Issued when your return contains structural errors.

Section 143(1) – Processing Intimation

Generated during CPC processing.

Section 143(2) – Scrutiny Notice

Issued when detailed verification is required.

Section 142(1) – Inquiry Notice

Requests information and supporting documents.

Section 148 – Reassessment Notice

Issued when income is believed to have escaped assessment.

Section 245 – Refund Adjustment Notice

Issued when refunds are adjusted against outstanding demands.

Income Tax Notice Timeline

Notice Type

Typical Timeline

Section 143(2)

Within 3 Months from End of Filing FY

Section 143(1)

Within 9 Months

Section 148

Up to 3 Years 3 Months

Section 148 (₹50L+)

Up to 5 Years 3 Months

Real-Life Case Studies

Salaried Employee

Received a Section 143(1) notice after failing to report salary from a second employer.

Freelancer

Received a Section 142(1) notice because bank credits exceeded declared professional receipts.

Investor

Received a scrutiny notice after failing to report capital gains from stock trading.

NRI

Received a notice after not filing returns despite earning NRO FD interest.

Crypto Investor

Received a notice due to VDA transactions reported through exchange data.

Income Tax Notice Prevention Checklist

Before filing:

✅ Download AIS

✅ Download TIS

✅ Verify Form 26AS

✅ Reconcile salary income

✅ Verify capital gains

✅ Report interest income

✅ Verify deductions

✅ Reconcile GST turnover

✅ Report foreign assets

✅ Report crypto income

Frequently Asked Questions (FAQs)

Can I ignore an income tax notice?

No. Ignoring a notice can lead to penalties, interest, and recovery proceedings.

Can salaried employees receive scrutiny notices?

Yes. Salary income mismatches frequently trigger scrutiny.

What is DIN in an income tax notice?

DIN is the Document Identification Number used to verify authenticity.

Can an AIS mismatch trigger a notice?

Yes. AIS mismatches are among the most common notice triggers.

Can I correct mistakes after receiving a notice?

In many cases, taxpayers can respond, rectify, or revise information depending on the notice type.

Conclusion

Income tax notices are increasingly generated through automated systems rather than manual investigations. The Income Tax Department now cross-checks information from AIS, TIS, Form 26AS, SFT reports, employers, banks, mutual funds, registrars, and even cryptocurrency exchanges. The best way to avoid notices is to reconcile all financial information before filing your return. By reviewing AIS, verifying tax credits, disclosing all income sources, and maintaining supporting documentation, taxpayers can significantly reduce the risk of receiving an income tax notice.