Most mismatch notices happen because taxpayers skip steps or do them in the wrong order. Follow this sequence:

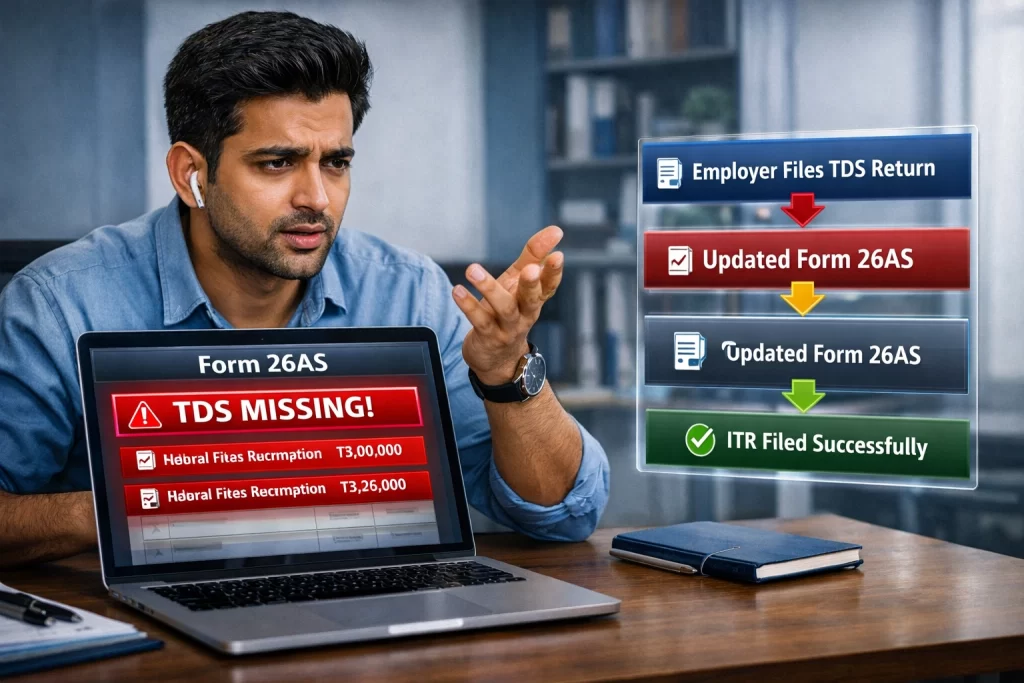

Step 1 — Form 26AS first. Verify every TDS and TCS entry against your Form 16 (salary), Form 16A (non-salary TDS), and other TDS certificates. If anything is missing or wrong, contact the deductor. This must be clean before you move forward.

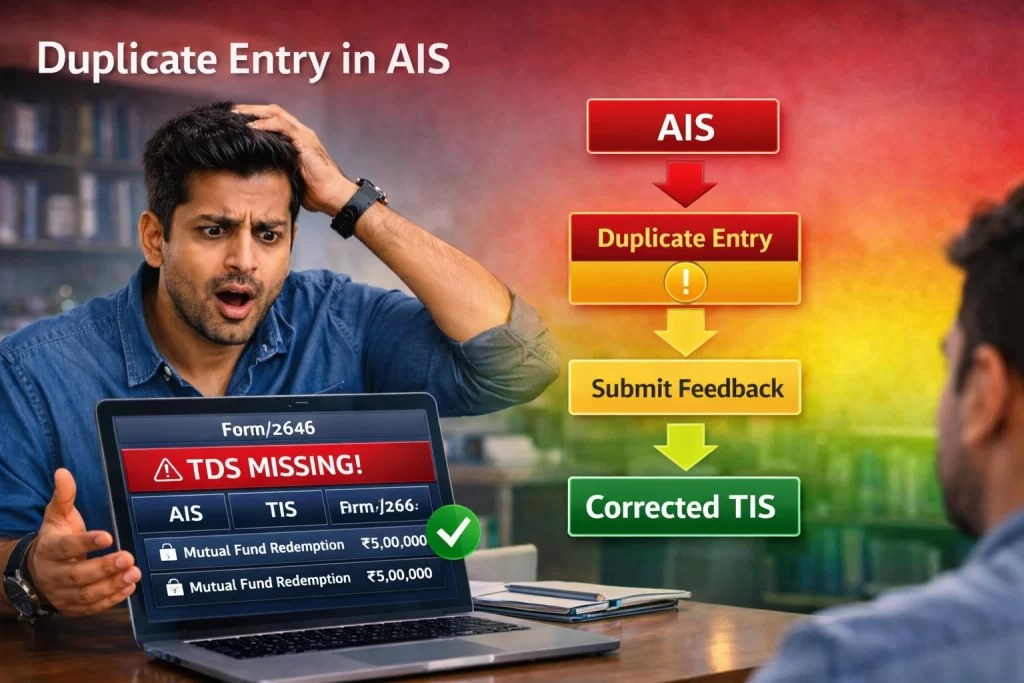

Step 2 — AIS second. Go through every AIS category: TDS/TCS, salary, interest, dividends, mutual fund transactions, capital gains, property, GST turnover, foreign remittances, cash deposits. Submit feedback on every entry that is incorrect, duplicate, or not applicable to you.

Step 3 — Wait 24 to 48 hours. AIS feedback flows to TIS within approximately 24 hours. Do not rush — let the system update before you check TIS.

Step 4 — TIS third. Review TIS aggregated values. Confirm they match your own income calculations. If the ITR pre-fill still looks wrong, go back and fix AIS feedback — do not manually override pre-fill values without first correcting AIS.

Step 5 — Cross-check against your own records. Compare AIS and TIS figures against your bank statements, broker statements, MF consolidated account statement (CAS), salary slips, rent receipts, and Form 16/16A. Declare what is correct per your own verified records not blindly based on AIS.

Step 6 — File ITR. The pre-fill should now be accurate. If any minor discrepancy still exists, declare what is correct per your documents and retain all supporting records. Never suppress income to match AIS — if AIS is wrong, submit feedback and document the reason.