India’s cryptocurrency taxation framework has evolved rapidly over the last few years. While most investors focus on the 30% tax on crypto gains, many overlook another critical compliance requirement—the 1% Tax Deducted at Source (TDS) under Section 194S of Income Tax Act. Whether you trade Bitcoin, Ethereum, NFTs, stablecoins, or other virtual digital assets (VDAs), understanding Section 194S is essential. A mistake in TDS compliance can result in interest, penalties, notices, and even prosecution in certain cases. This guide explains Section 194S in simple language, provides real-world examples, compares it with 194A of Income Tax Act and 194IA of Income Tax Act, and covers the latest 2026 compliance requirements.

What Is Section 194S of Income Tax Act?

Section 194S of Income Tax Act requires a buyer to deduct TDS at 1% when paying consideration to a resident for the transfer of a Virtual Digital Asset (VDA). The provision was introduced to create a transparent reporting trail for cryptocurrency and NFT transactions and to help the Income Tax Department monitor digital asset activity.

Why Was Section 194S Introduced?

Before Section 194S, crypto transactions often occurred outside traditional financial reporting systems. The government introduced TDS to:

Track digital asset transactions

Improve tax compliance

Reduce unreported crypto gains

Create transaction-level reporting

What Is a Virtual Digital Asset (VDA)?

Under the Income Tax Act, a Virtual Digital Asset includes:

Bitcoin (BTC)

Ethereum (ETH)

Solana (SOL)

Ripple (XRP)

Stablecoins such as USDT and USDC

Non-Fungible Tokens (NFTs)

Similar blockchain-based digital assets

Virtual digital assets do not include traditional Indian currency or foreign currency recognized as legal tender.

Section 194S TDS Rate and Threshold Limits

TDS Rate Under Section 194S

Particulars

TDS Rate

Standard Rate

1%

PAN Not Available

20%

Threshold Limits

Category

Threshold

Specified Person

₹50,000

Other Taxpayers

₹10,000

Once the threshold is crossed, TDS must be deducted on the transaction value.

Who Is a Specified Person Under Section 194S?

A specified person generally includes:

Salaried individuals

Pensioners

Small taxpayers

Individuals or HUFs with limited business turnover

Specified persons enjoy higher threshold limits and simplified compliance requirements.

When Is TDS Deducted Under Section 194S?

TDS must be deducted at the earlier of:

Credit of consideration to the seller

Actual payment to the seller

This rule applies regardless of whether payment is made through:

Bank transfer

Exchange wallet

Crypto-to-crypto transfer

Other digital settlement methods

How Section 194S Works in Real-Life Crypto Transactions

Example – Bitcoin Purchase Through Exchange

Suppose an investor purchases Bitcoin worth ₹5,00,000.

Particulars

Amount

Purchase Value

₹5,00,000

TDS @1%

₹5,000

The exchange deducts ₹5,000 and deposits it with the government.

Example – Peer-to-Peer Crypto Transaction

A buyer purchases USDT worth ₹1,00,000 directly from another resident individual.

Particulars

Amount

Transaction Value

₹1,00,000

TDS @1%

₹1,000

The buyer must deposit ₹1,000 with the government before completing the transaction.

Example – NFT Purchase

An NFT is purchased for ₹2,50,000.

Particulars

Amount

NFT Value

₹2,50,000

TDS @1%

₹2,500

The buyer deducts and deposits ₹2,500 as TDS.

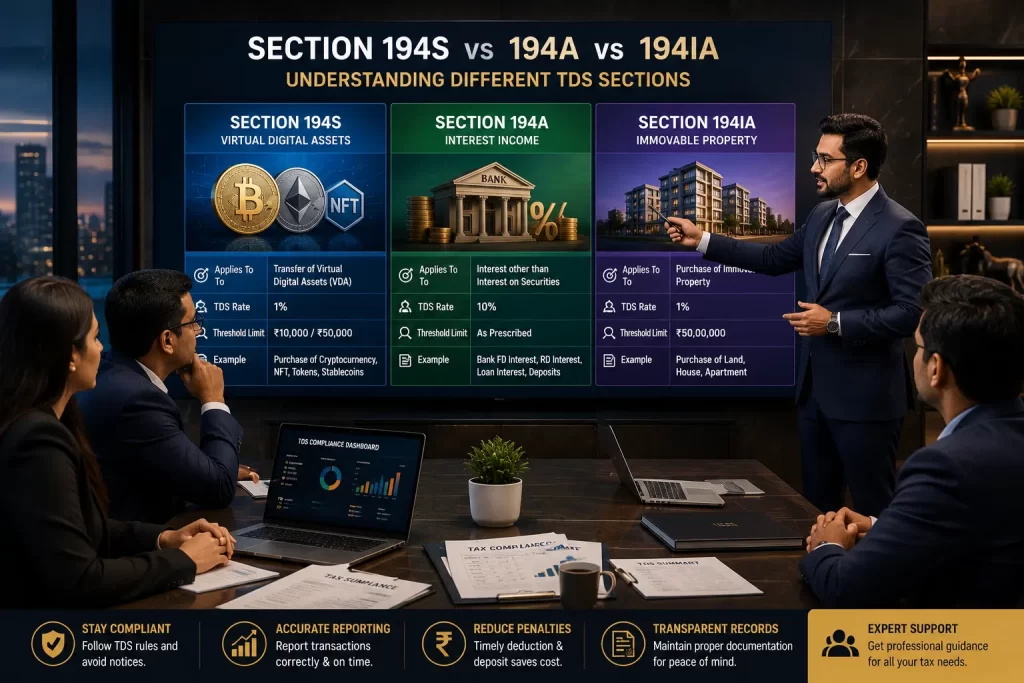

Section 194S vs Section 194A vs Section 194IA

Many taxpayers confuse these provisions.

Comparison Table

Particulars

Section 194S

Section 194A

Section 194IA

Purpose

Crypto & VDA Transactions

Interest Income

Property Purchase

TDS Rate

1%

10%

1%

Threshold

₹10,000 / ₹50,000

As Prescribed

₹50 Lakh

Asset Type

Digital Assets

Interest

Immovable Property

Applicability

VDA Transfer

Interest Payment

Property Transfer

This comparison helps users searching for 194 a of income tax act, 194 ia of income tax act, and sec 194 of income tax act understand the differences quickly.

Section 194A of Income Tax Act – Brief Overview

Section 194A deals with TDS on interest other than interest on securities.

Common examples include:

Fixed Deposit Interest

Recurring Deposit Interest

NBFC Interest

Corporate Deposits

Banks and financial institutions deduct TDS when interest exceeds prescribed thresholds.

Section 194IA of Income Tax Act – Brief Overview

Section 194IA applies when purchasing immovable property.

Key Rule

If the property value is ₹50 lakh or more, the buyer must deduct TDS at 1%.

Example

Property Value = ₹80,00,000

TDS = ₹80,000

The buyer deposits this TDS using the prescribed form before completing compliance.

Penalties for Non-Compliance Under Section 194S

Failure to comply with Section 194S can result in significant consequences.

Interest for Failure to Deduct

1% per month or part thereof.

Interest for Late Deposit

1.5% per month or part thereof.

Penalty

The penalty may be equal to the amount of tax not deducted.

Late Filing Fee

₹200 per day until compliance is completed.

Common Mistakes Taxpayers Make Under Section 194S

Many crypto investors unknowingly violate TDS provisions.

Common mistakes include:

Ignoring peer-to-peer transactions.

Assuming exchanges handle all compliance.

Not checking threshold limits.

Failing to obtain PAN details.

Missing filing deadlines.

Not maintaining transaction records.

2026 Updates for Section 194S

The transition to the Income Tax Act, 2025 has streamlined various TDS reporting requirements.

Key changes include:

Consolidated reporting mechanisms

Improved digital compliance

Greater AIS integration

Enhanced transaction tracking

Stronger reporting obligations for VDA transactions

Taxpayers should ensure their records align with AIS and TDS reporting systems.

Compliance Checklist for Section 194S

Before filing your return, ensure:

✅ All VDA transactions recorded

✅ TDS deducted correctly

✅ PAN details verified

✅ Threshold limits reviewed

✅ Returns filed on time

✅ TDS certificates obtained

✅ AIS reviewed

✅ Crypto exchange statements reconciled

Frequently Asked Questions (FAQs)

What is Section 194S of Income Tax Act?

Section 194S requires deduction of 1% TDS on consideration paid for transfer of virtual digital assets such as cryptocurrencies and NFTs.

Who has to deduct TDS under Section 194S?

The buyer, exchange, or specified intermediary involved in the transaction is generally responsible for deducting TDS.

What is the TDS rate under Section 194S?

The standard TDS rate is 1%. If PAN is not available, the rate may increase to 20%.

Does Section 194S apply to NFTs?

Yes. NFTs are classified as Virtual Digital Assets and fall within the scope of Section 194S.

What is the difference between Section 194S and Section 194A?

Section 194S applies to virtual digital assets, whereas Section 194A applies to interest income.

What is the difference between Section 194S and Section 194IA?

Section 194S covers crypto and digital assets, while Section 194IA applies to property transactions.

Can I claim credit for TDS deducted under Section 194S?

Yes. TDS deducted can generally be claimed as credit while filing your income tax return.

Final Thoughts

The 194S of Income Tax Act has become one of the most important compliance provisions for cryptocurrency investors, NFT traders, exchanges, and digital asset businesses in India. While the 1% TDS may appear small, non-compliance can lead to penalties, interest, and reporting issues. Understanding how Section 194S, 194A of Income Tax Act, and 194IA of Income Tax Act operate helps taxpayers remain compliant while avoiding unnecessary tax disputes. As digital asset regulation continues to evolve, maintaining proper records and following TDS obligations will be essential for every investor and business participating in India’s growing digital economy.