Many partnership firms in India end up paying more tax than necessary—not because their profits are high, but because they fail to structure partner remuneration correctly, miss deductions under Section 40(b), or overlook compliance requirements under Section 184.In 2026, partnership firm taxation has become more important than ever. The Income Tax Department now uses advanced compliance systems, AIS reporting, GST data matching, and digital scrutiny tools to identify mismatches and non-compliance. A simple mistake in tax planning or income tax return filing for a partnership firm can result in additional tax liability, penalties, or scrutiny notices.Whether you operate a trading business, consultancy, manufacturing unit, agency, or professional services firm, understanding income tax for partnership firm can help you optimize tax liability, remain compliant, and avoid costly mistakes.

What Is a Partnership Firm Under Income Tax Law?

A partnership firm is a business structure where two or more individuals agree to carry on a business and share profits according to a partnership deed. For income tax purposes, a partnership firm is treated as a separate taxable entity.

Income Tax for Partnership Firm: Tax Rate in India (2026)

One of the most searched questions is:

What is the partnership firm tax rate in India?

Unlike individuals, partnership firms do not receive slab benefits. They are taxed at a flat rate.

Particulars

Tax Rate

Income Tax

30%

Surcharge (Income Above ₹1 Crore)

12%

Health & Education Cess

4%

Effective Tax Rate for Partnership Firms

Taxable Income

Effective Tax Rate

Up to ₹1 Crore

31.20%

Above ₹1 Crore

Approximately 35%

This makes tax planning extremely important for partnership firms.

How Income Tax for Partnership Firm Is Calculated

Understanding partnership firm tax calculation is essential for proper compliance.

Example 1: Small Partnership Firm

Profit Before Partner Remuneration = ₹20,00,000

Partner Salary Allowed = ₹5,00,000

Taxable Income = ₹15,00,000

Income Tax @30% = ₹4,50,000

Health & Education Cess @4% = ₹18,000

Total Tax Liability = ₹4,68,000

Example 2: Medium-Sized Firm

Profit = ₹80,00,000

Allowable Partner Remuneration = ₹18,00,000

Taxable Income = ₹62,00,000

Income Tax @30% = ₹18,60,000

Cess @4% = ₹74,400

Total Tax = ₹19,34,400

Section 184: Conditions for Partnership Firm Tax Benefits

Section 184 is one of the most important provisions for partnership firm taxation in India.

A firm can claim deductions for:

Partner salary

Partner remuneration

Interest on capital

only if Section 184 conditions are satisfied.

Requirements Under Section 184

Written Partnership Deed

The partnership must be governed by a written deed.

2. Profit Sharing Ratio

The partnership deed must clearly specify the profit-sharing ratio.

3. Certified Copy Submission

A certified copy of the partnership deed must be available for tax purposes.

4. Changes Must Be Updated

Any changes in partners or profit-sharing ratios should be documented properly.

5. Consequences of non-compliance

Failure to comply with Section 184 may result in:

Disallowance of partner remuneration

Disallowance of partner interest

Increased taxable income

Higher tax liability

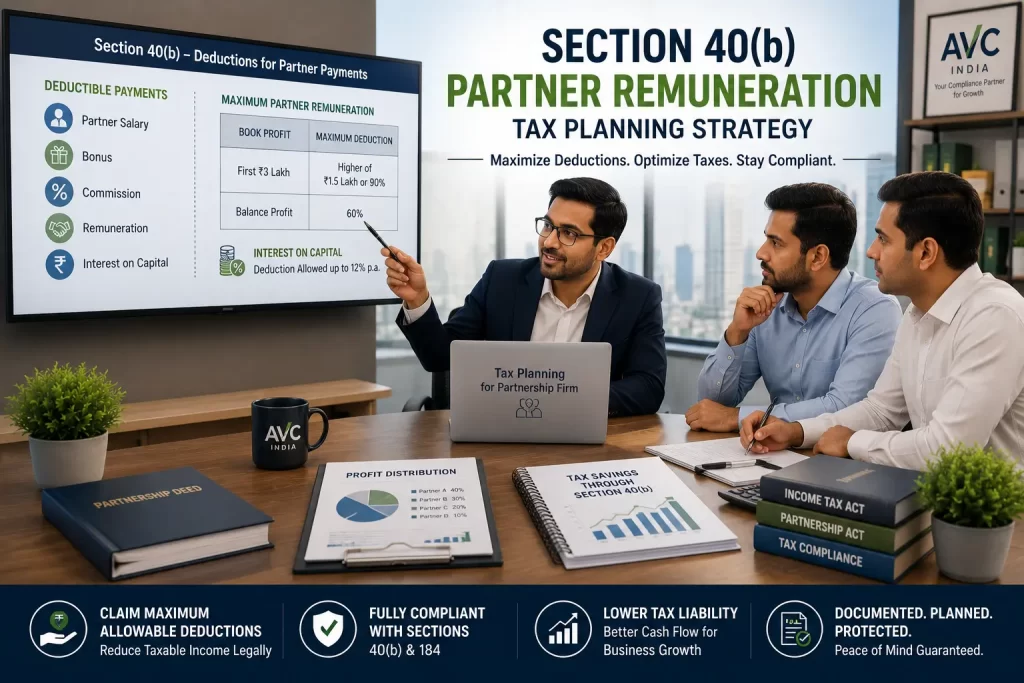

Section 40(b): Deductions Available to Partnership Firms

Section 40(b) allows partnership firms to deduct payments made to partners under specified conditions.This is one of the biggest tax-saving provisions available.

Deductible Payments

A partnership firm may claim deductions for:

Partner salary

Bonus

Commission

Remuneration

Interest on capital

provided these are authorized by the partnership deed.

Maximum Partner Remuneration Allowed Under Section 40(b)

Book Profit

Maximum Deduction

First ₹3 Lakh

Higher of ₹1.5 Lakh or 90%

Balance Profit

60%

Example

Book Profit = ₹10 lakh

First ₹3 lakh: 90% = ₹2.7 lakh

Remaining ₹7 lakh: 60% = ₹4.2 lakh

Maximum Remuneration Deduction = ₹6.9 lakh

Interest on Capital Deduction

Interest paid to partners on capital is deductible up to:

12% Per Annum

Any interest above 12% is disallowed.

Example

Capital Contribution = ₹10 lakh

Interest Paid = ₹1.5 lakh

Allowed Interest = ₹1.2 lakh

Disallowed = ₹30,000

Partner Remuneration vs Partner Drawings

Many business owners confuse remuneration and drawings.

Particulars

Partner Remuneration

Partner Drawings

Deductible to Firm

Yes

No

Taxable to Partner

Yes

No

Covered under Section 40(b)

Yes

No

Reduces Firm Profit

Yes

No

Proper classification is essential during income tax return filing for partnership firm.

Section 194T: New TDS Rules for Partnership Firms

One of the biggest changes affecting partnership firms is Section 194T.

This section introduces TDS obligations on certain payments made to partners.

Covered Payments

Salary

Remuneration

Bonus

Commission

Interest

Compliance Risks

Many firms fail to recognize that TDS may be triggered when income is credited to the partner’s account, even if no actual payment is made.

This makes bookkeeping and compliance more important than ever.

Income Tax Return Filing for Partnership Firm

Another frequently searched topic is income tax return filing for partnership firm.

Which ITR Form Is Used?

Partnership firms must generally file:

ITR-5

ITR-5 is applicable to:

Partnership firms

LLPs

Associations of Persons

Documents Required

Before starting the income tax return filing process for a partnership firm, it is important to gather all relevant financial and compliance documents to ensure accurate reporting and avoid delays. Key documents generally include the firm’s PAN card, a valid partnership deed, balance sheet, profit and loss account, GST returns, bank statements, and TDS certificates. These records help in calculating taxable income, claiming eligible deductions, reconciling financial transactions, and verifying tax credits. If the partnership firm is subject to a tax audit, the audit report should also be kept ready before filing the return. Having these documents organized in advance makes the ITR-5 filing process smoother, reduces the risk of errors, and helps maintain compliance with income tax regulations.

Step-by-Step ITR Filing Process

Step 1

Prepare financial statements.

Step 2

Calculate taxable income.

Step 3

Compute allowable deductions.

Step 4

File ITR-5 online.

Step 5

Verify return through DSC or electronic verification.

Due Date for Income Tax Return Filing for Partnership Firm

Type of Firm

Due Date

Non-Audit Cases

As Notified by CBDT

Audit Cases

As Notified by CBDT

Always verify current-year deadlines before filing.

Tax Audit for Partnership Firms

Tax audit is mandatory in certain situations.

When Is Audit Required?

Generally, audit may become applicable when turnover exceeds prescribed limits or specific tax provisions require verification.

Why Audit Matters?

A tax audit plays a crucial role in ensuring the accuracy and reliability of a partnership firm’s financial records. It helps verify whether the financial statements and books of accounts have been maintained correctly and in accordance with applicable tax laws. An audit also strengthens overall tax compliance by identifying reporting errors, inconsistencies, or omissions before the return is filed. In addition, properly audited financial records can reduce the likelihood of receiving scrutiny notices from the Income Tax Department and improve the accuracy of financial reporting. For growing businesses, a tax audit not only supports regulatory compliance but also enhances transparency and credibility in financial management.

Can Partnership Firms Opt for Presumptive Taxation?

Yes, certain partnership firms may choose presumptive taxation unde

Section 44AD

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Ut elit tellus, luctus nec ullamcorper mattis, pulvinar dapibus leo.

Applicable to eligible businesses.

Important Limitation

If a firm opts for presumptive taxation, separate deductions for:

Partner salary

Partner remuneration

Interest on capital

may not be available.

This is a major area where taxpayers make mistakes.

Tax Saving Strategies for Partnership Firms

Optimize Partner Remuneration

Structure remuneration within Section 40(b) limits.

Claim Interest on Capital Correctly

Stay within the 12% limit.

Maintain Proper Documentation

Keep books updated and reconciled.

Claim Legitimate Business Expenses

Document all expenses properly.

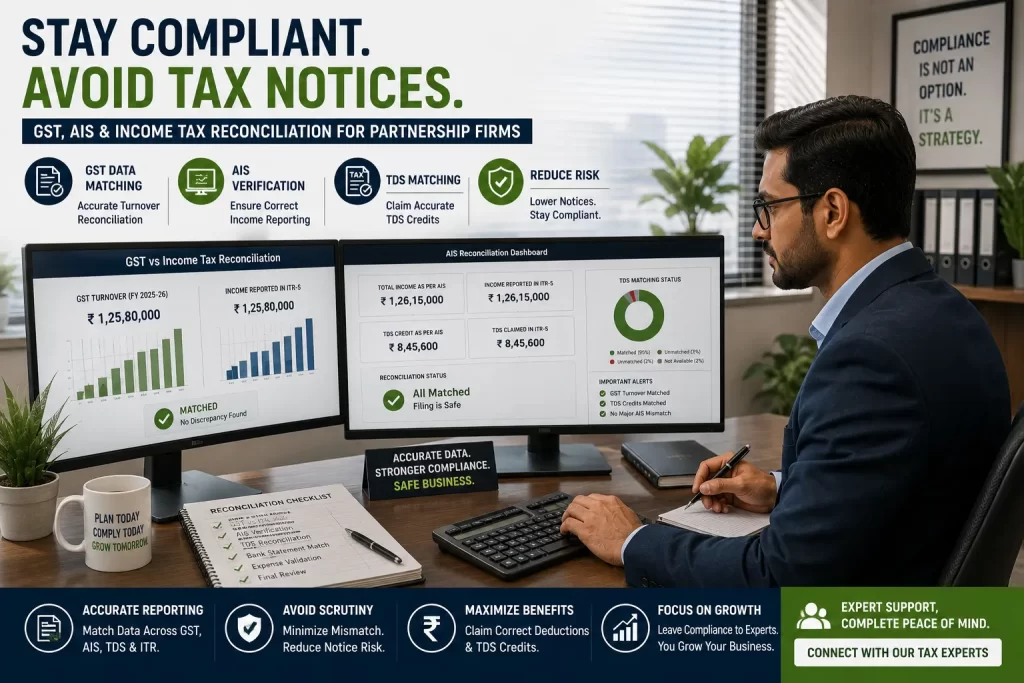

Reconcile GST and Income Tax Data

Avoid mismatch notices.

Plan Advance Tax

Prevent interest liabilities.

Income Tax Notices Received by Partnership Firms

Partnership firms increasingly receive notices due to:

AIS Mismatch

Income reported differently in AIS and ITR.

GST Turnover Mismatch

Differences between GST turnover and reported income.

TDS Mismatch

Incorrect reporting of TDS credits.

Scrutiny Notices

Issued when discrepancies are identified.

Proper compliance significantly reduces these risks.

Penalties for Non-Compliance

Default

Consequence

Late Filing

Late fee and interest

Audit Non-Compliance

Penalty exposure

TDS Default

Interest and penalties

Incorrect Reporting

Scrutiny and reassessment

Partnership Firm vs LLP vs Private Limited Company

Particulars

Partnership Firm

LLP

Private Limited

Tax Rate

30%

30%

Corporate Rate

Compliance Burden

Moderate

Moderate

High

Audit Requirements

Applicable

Applicable

Extensive

Startup Benefits

Limited

Moderate

Highest

Partnership Firm Compliance Checklist for 2026

Before proceeding with income tax return filing for partnership firm, businesses should complete a final compliance review to ensure accurate reporting and avoid penalties. This checklist can help firms meet partnership firm compliance India requirements, perform proper partnership firm tax calculation, and comply with applicable partnership firm taxation India rules before filing ITR-5.

• Partnership deed updated • PAN active • GST reconciled • Books maintained • Partner remuneration calculated correctly under Section 40(b) partnership firm provisions • Interest on capital verified • TDS compliance completed • AIS checked • Audit completed (if applicable under the partnership firm audit limit) • ITR-5 filed on time in accordance with income tax for partnership firm requirements and the applicable partnership firm tax rate India provisions

Frequently Asked Questions (FAQs)

What is the income tax rate for a partnership firm in India?

A partnership firm is taxed at a flat rate of 30% plus applicable surcharge and 4% Health & Education Cess.

Is partner salary taxable?

Yes. Partner salary or remuneration received from a partnership firm is taxable in the hands of the partner.

Which ITR form is used for partnership firms?

Partnership firms generally file their income tax return using ITR-5.

Can a partnership firm claim deductions for partner remuneration?

Yes. Deductions are allowed under Section 40(b), subject to prescribed limits and compliance with Section 184.

What is Section 184?

Section 184 lays down conditions that partnership firms must satisfy to claim deductions for partner salary, remuneration, and interest.

What is the maximum interest on capital allowed?

Interest on capital is deductible up to 12% per annum. Any excess amount is disallowed.

Is audit compulsory for partnership firms?

Audit requirements depend on turnover, receipts, and applicable tax provisions. Firms should evaluate audit applicability each year.

Can partnership firms use presumptive taxation?

Yes, eligible firms may opt for presumptive taxation under Section 44AD, subject to conditions.

Final Thoughts

Here’s a naturally optimized version of your conclusion with all the target keywords incorporated without sounding forced:

Understanding income tax for partnership firm is no longer just about knowing the applicable tax rate. In 2026, businesses must have a clear understanding of the partnership firm tax rate India, Section 184 requirements, Section 40(b) partnership firm deductions, partner remuneration planning, TDS obligations, GST reconciliation, and accurate income tax return filing for partnership firm operations. Effective partnership firm taxation India requires careful tax planning, proper bookkeeping, and a thorough understanding of partnership firm tax calculation methods to minimize tax liability while remaining compliant with the law.

In addition, firms should regularly assess the applicable partnership firm audit limit, maintain updated records, and complete ITR filing for partnership firm within the prescribed deadlines. Strong partnership firm compliance India practices not only help businesses avoid penalties, notices, and scrutiny but also improve long-term financial efficiency and operational transparency. By claiming eligible deductions, maintaining proper documentation, and following the latest tax regulations, a partnership firm can optimize its tax position and achieve sustainable growth. If you need assistance with partnership firm taxation, tax planning, audit support, or income tax return filing for partnership firm, professional guidance can help ensure maximum tax benefits while maintaining full compliance with evolving Indian tax laws.