-

-

Tax Services

-

Audit & Assurance

-

Business Setup

-

Accounting & Payroll

-

Advisory

-

Your bank just deducted tax from your fixed deposit interest and you have no idea why. This is one of the most common tax surprises faced by Indian investors, salaried employees, and senior citizens. The mechanism behind it is 194 A of Income Tax Act, a statutory provision that quietly withholds 10% of your interest income before it ever reaches your account. Understanding section 194A is not just useful — it is financially important. Knowing the exact threshold limits, the applicable rates, and the right forms to submit can put thousands of rupees back in your pocket every year. This guide covers everything: the TDS rate structure, threshold limits updated for FY 2025-26, step-by-step calculation examples, the Form 15G and Form 15H process, all legal exemptions, penalty consequences, and the upcoming transition to the Income Tax Act, 2025.

| Parameter | Details |

|---|---|

| Applicable Section | Section 194A, Income Tax Act, 1961 (Transitioning to Section 393(1), Income Tax Act, 2025 from April 1, 2026) |

| TDS Rate | 10% with valid PAN; 20% without PAN |

| Threshold – Banks / Post Offices (Senior Citizens 60+) | ₹1,00,000 per financial year (FY 2025-26 onwards) |

| Threshold – Banks / Post Offices (Other Individuals) | ₹50,000 per financial year (FY 2025-26 onwards) |

| Threshold – Other Payers (Companies, NBFCs, Firms) | ₹10,000 per financial year (FY 2025-26 onwards) |

| Form to Avoid TDS | Form 15G / Form 15H (Form 121 from April 1, 2026 under new Act) |

| Applicable Payees | Resident Individuals, HUFs, Firms, LLPs, and Companies |

Section 194A of the Income Tax Act, 1961 is a withholding tax provision that makes it mandatory for certain payers to deduct tax at source on interest payments made to resident individuals and entities — but specifically on interest other than interest on securities. The phrase “other than interest on securities” is the defining boundary of this section. Interest on securities — such as government bonds, listed debentures, and public debt instruments — falls under Section 193 of the Act and follows different withholding rules. Section 194A, by contrast, governs the everyday interest income that millions of Indians earn from fixed deposits, recurring deposits, and private loans. To understand what is section 194A of income tax act fully, it also helps to distinguish it from three commonly confused provisions: Section 194 governs TDS on dividend distributions made by domestic companies on equity shares — not interest income at all. Section 194-IA (often referred to as 194 i a of income tax act) mandates a 1% TDS deduction by a buyer when purchasing immovable property valued at ₹50 lakhs or more. This is a property transaction provision, entirely separate from interest income. Section 194JA (a sub-division of Section 194J) prescribes a 2% TDS on fees paid for professional or technical services — again, a completely different category. In plain terms: if a resident taxpayer earns interest from a bank fixed deposit, a corporate deposit with an NBFC, a personal loan extended to a business, or even delayed payment interest on a commercial invoice, TDS under section 194A becomes applicable once the interest crosses the prescribed annual threshold. One important forward-looking development: effective April 1, 2026, the Income Tax Act, 1961 is being replaced by the consolidated Income Tax Act, 2025. Under this new framework, Section 194A is remapped to Section 393(1), where all non-salary TDS provisions are consolidated into a single table-driven structure. The core rates and thresholds remain continuous, but the statutory numbering changes.

The legal obligation to deduct TDS under section 194A does not fall on every interest-paying entity. The law carefully designates specific categories of payers — called deductors — who are personally responsible for calculating, withholding, and depositing the tax.

| Class of Payer | TDS Deduction Requirement | Statutory Basis |

|---|---|---|

| Banking Companies (Public, Private, Foreign) | Mandatory | All branches operating in India |

| Cooperative Societies Engaged in Banking | Mandatory | Those carrying on cooperative banking business |

| National Post Offices | Mandatory | On deposit schemes notified by Central Government |

| Companies and LLPs | Mandatory | Applicable to corporate deposits, inter-company loans, and public deposits |

| Partnership Firms | Mandatory | On third-party commercial loans and unsecured advances |

| Individuals and HUFs | Conditional | Only if subject to tax audit under Section 44AB |

An individual or a Hindu Undivided Family (HUF) is generally exempt from deducting TDS under section 194A — this is the default position. However, this exemption is withdrawn when the individual or HUF crosses the Section 44AB tax audit threshold. This happens when business turnover exceeds ₹1 crore (which may extend to ₹10 crore where at least 95% of receipts and payments are digital) or when professional gross receipts exceed ₹50 lakhs in the immediately preceding financial year. Once these thresholds are crossed, the individual or HUF becomes a mandatory deductor under section 194A for all eligible interest payments they make. A salaried individual paying interest on a home loan to another individual, for instance, is not liable to deduct TDS. But a business owner who crosses the audit threshold and pays interest on a private loan must comply fully.

Section 194A casts a wide net. It covers most forms of interest income that residents earn outside of securities markets, including:

Bank Fixed Deposits (FDs): Interest on standard term deposits, cumulative deposits, and tax-saving FDs (except ELSS) is covered. This is the most common TDS scenario for retail investors.

Recurring Deposits (RDs): Periodic interest credited on systematic RD accounts is equally subject to TDS once the annual threshold is crossed.

Interest on Private Loans and Advances: When a company, firm, or audit-liable individual pays interest on a loan received from another person — whether a friend, relative, director, or business associate — section 194A applies.

Inter-Corporate Deposits: Interest paid by one corporate entity to another on surplus fund deposits or short-term placements falls under this section.

NBFC Deposits: Interest paid on corporate fixed deposits held with Non-Banking Financial Companies is covered under section 194A.

Delayed Payment Interest (Penal Interest): Interest paid in commercial transactions due to delayed settlement of invoices is treated as “interest” under Section 2(28A) of the Act. This means firms that charge or pay interest for late invoice payments must account for TDS under section 194A — a compliance point that is frequently missed in practice.

Court Compensation Interest: Under the Income Tax Act, 1961, interest on Motor Accident Claims Tribunal (MACT) awards was exempt up to ₹50,000. Under the Income Tax Act, 2025 (effective April 1, 2026), interest on MACT compensation paid to a natural person is fully exempt from both income tax and TDS — removing the ₹50,000 ceiling entirely.

Two important exclusions deserve specific mention: interest earned on a standard savings bank account is completely exempt from TDS under section 194A (though it remains taxable income), and interest on income tax refunds is similarly not subject to withholding under this section.

The Finance Act, 2025 introduced significant upward revisions to the TDS threshold limits under section 194A, effective from April 1, 2025. These higher limits are designed to reduce unnecessary tax deductions for small savers, senior citizens, and micro-entrepreneurs.

| Category of Payer | Category of Payee | Threshold (FY 2024-25) | Threshold (FY 2025-26 Onwards) |

|---|---|---|---|

| Banks, Cooperative Societies, Post Offices | Resident Senior Citizens (60+ Years) | ₹50,000 | ₹1,00,000 |

| Banks, Cooperative Societies, Post Offices | Other Resident Individuals and HUFs | ₹40,000 | ₹50,000 |

| Any Other Payer (Companies, NBFCs, Firms, Audit-Liable Individuals) | All Resident Payees | ₹5,000 | ₹10,000 |

A point that most taxpayers misunderstand: the TDS threshold is not calculated per branch but across all branches of the same bank, aggregated under a single PAN. With the integration of Core Banking Solutions (CBS), banks automatically pool all interest credits to every FD, RD, or deposit account linked to one PAN across all their branches. If a taxpayer below 60 years holds three separate fixed deposits of ₹3,00,000 each across three different branches of the same bank at 8% per annum, the annual interest would be ₹24,000 per branch — amounting to ₹72,000 in total. Because ₹72,000 exceeds the ₹50,000 bank-wide threshold, TDS will be deducted on the full ₹72,000, not just the excess. Maintaining deposits across different banks, however, keeps each bank’s threshold independent — a legal and commonly used planning approach.

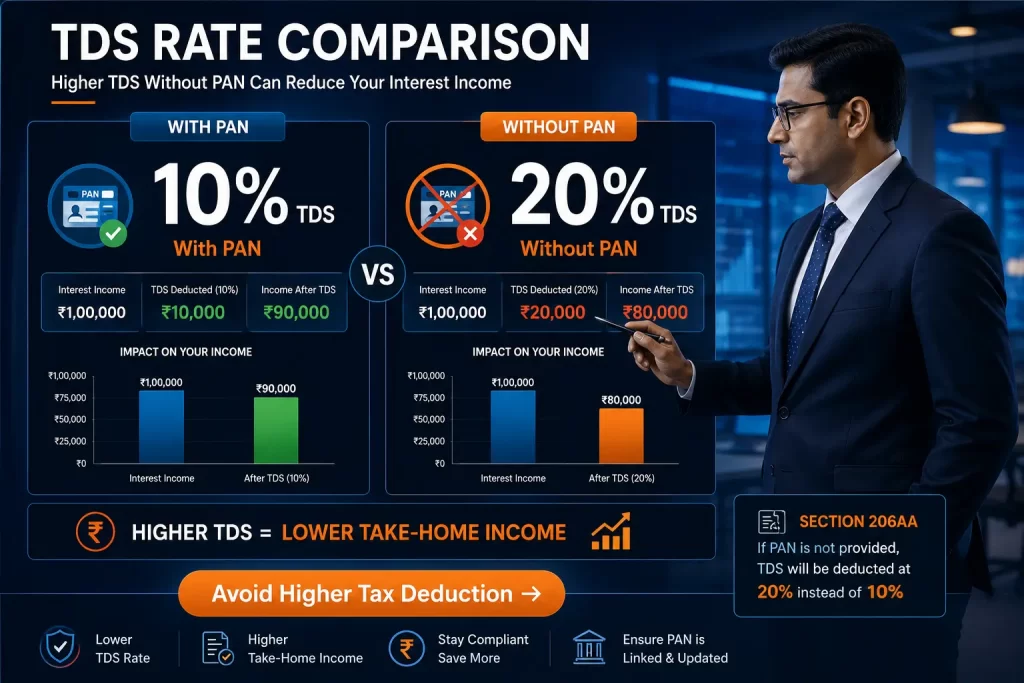

The withholding tax rate under section 194A is straightforward, but it shifts significantly based on one factor: whether the payee has furnished a valid PAN.

| Scenario | Applicable TDS Rate |

|---|---|

| Valid PAN provided by the payee | 10% |

| PAN not provided or invalid (Section 206AA applies) | 20% |

| Valid Form 15G or Form 15H submitted | NIL |

| Lower or NIL deduction certificate obtained under Section 197 | As specified in the certificate |

| Non-resident payee | Section 195 applies — Section 194A does not |

Two aspects of this rate structure deserve attention. First, there is no surcharge, health and education cess, or any other additional levy on TDS rates under section 194A when payments are made to domestic residents. The rate is flat — 10% is 10%, not 10.4% or any higher effective rate. Second, the 20% penalty rate under Section 206AA applies even if the payee submits Form 15G or Form 15H without a valid PAN. In that scenario, the self-declaration is treated as legally invalid and the higher rate is enforced regardless.

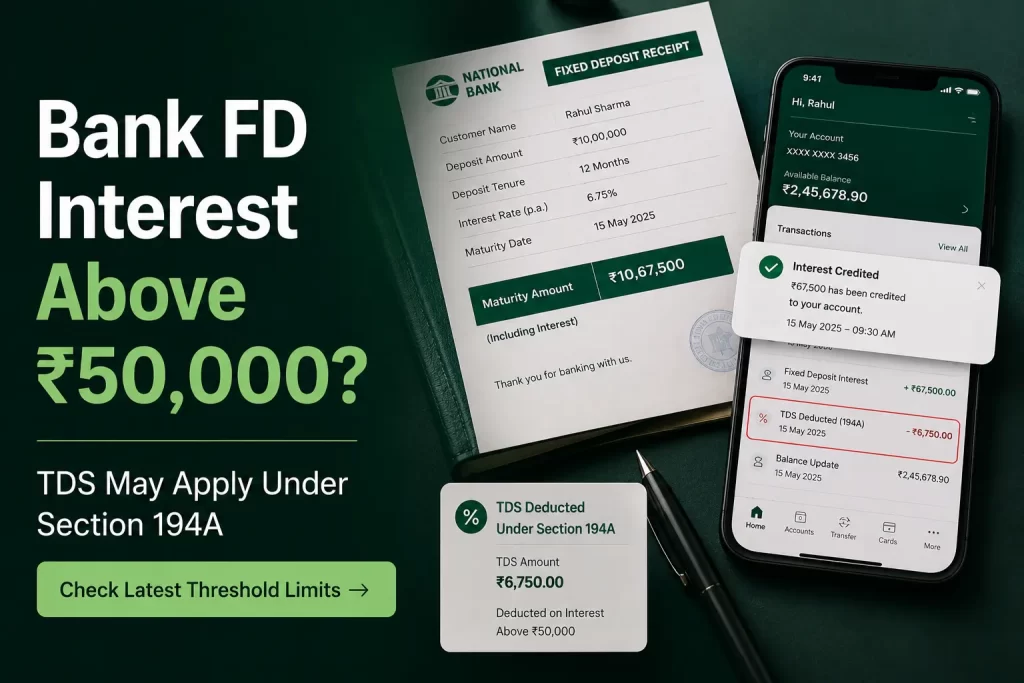

Mr. Ravi, aged 35, holds fixed deposits totalling ₹8,00,000 at State Bank of India at an annual interest rate of 8%.

Annual interest = ₹8,00,000 × 8% = ₹64,000

Applicable threshold for non-senior citizens (banking payer) in FY 2025-26 = ₹50,000

Since ₹64,000 exceeds ₹50,000, TDS is applicable. Importantly, TDS is deducted on the entire interest amount, not just the portion exceeding the threshold.

TDS = 10% × ₹64,000 = ₹6,400

Net interest received by Ravi = ₹64,000 − ₹6,400 = ₹57,600

Mrs. Sunita, aged 65, earns ₹90,000 as annual interest from cumulative bank fixed deposits.

Applicable threshold for senior citizens (banking payer) in FY 2025-26 = ₹1,00,000

Since ₹90,000 is below ₹1,00,000, TDS is not applicable.

TDS deducted = NIL

Mrs. Sunita receives the full ₹90,000, though she must still declare this income under “Income from Other Sources” in her ITR.

ABC Pvt Ltd pays ₹15,000 as annual interest on a loan borrowed from Mr. Amit, who provides a valid PAN.

Applicable threshold for non-banking payers in FY 2025-26 = ₹10,000

Since ₹15,000 exceeds ₹10,000, TDS applies on the full ₹15,000.

TDS = 10% × ₹15,000 = ₹1,500

Net amount paid to Mr. Amit = ₹15,000 − ₹1,500 = ₹13,500

Same parameters as Example 3, but Mr. Amit fails to provide his PAN to ABC Pvt Ltd.

The rate doubles to 20% under Section 206AA.

TDS = 20% × ₹15,000 = ₹3,000

Net amount paid to Mr. Amit = ₹15,000 − ₹3,000 = ₹12,000

The difference between providing and not providing PAN is ₹1,500 in additional TDS on a single ₹15,000 payment. On larger loan amounts, this penalty effect becomes substantial.

Under section 194A, the obligation to deduct tax arises at whichever of the following two events occurs first: The time of credit of interest to the payee’s account in the books of the deductor — this includes credit to any account, regardless of whether it is labelled “Interest Payable Account,” “Suspense Account,” or any similar ledger head. The time of actual payment of interest in cash, by cheque, by bank transfer, or by any other mode. This timing rule has a practical implication that catches many businesses off-guard. A company that accrues and credits loan interest to a lender’s account at the end of the financial year (March 31) but physically transfers the money only in May must deduct and deposit TDS based on the March credit entry — not the May payment date. For banks, this means TDS must be deducted at each quarterly interval when interest is credited to cumulative fixed deposits, even though the depositor does not receive any physical payout until maturity.

Section 194A(3) provides a statutory list of situations where tax deduction at source is not required, regardless of the interest amount involved.

Payments to Banking Institutions: Interest paid or credited to any banking company or cooperative society engaged in banking is exempt. Banks paying interest to other banks do not deduct TDS.

Payments to Public Financial Institutions: Interest paid to the Life Insurance Corporation of India (LIC), the Unit Trust of India (UTI), or Central Government-notified public insurance companies is exempt.

Payments to the Central or State Government: Direct interest credits to government entities require no TDS.

Interest Below Threshold Limits: As detailed in the threshold table above — ₹50,000 for banks (non-senior citizens), ₹1,00,000 for banks (senior citizens), and ₹10,000 for other payers in FY 2025-26.

Motor Accident Claims Tribunal Awards: Under the 1961 Act, interest on MACT compensation was exempt only up to ₹50,000. Effective April 1, 2026, the Income Tax Act, 2025 makes this exemption unlimited for natural persons — all MACT interest is fully exempt.

Valid Form 15G or Form 15H Submission: When a qualifying resident submits a valid self-declaration confirming zero net tax liability.

Payments to the Reserve Bank of India: Interest paid directly to the RBI carries no TDS obligation.

Interest Under Section 194LC: Interest paid by Indian companies to non-residents on certain approved foreign borrowings follows the concessional TDS rules under Section 194LC and is exempt from section 194A.

Partnership Firm to Partners — Important Change from April 2025: Historically, under Section 194A(3)(iv), interest paid by a partnership firm to its partners was fully exempt from TDS. This changed with the Finance Act, 2024. Effective April 1, 2025, a new Section 194T requires partnership firms to deduct 10% TDS on salary, interest, commission, bonus, or remuneration paid to partners if the aggregate exceeds ₹20,000 in the financial year. The exemption under Section 194A(3)(iv) effectively no longer applies for partner interest — it has migrated to Section 194T.

If a resident taxpayer’s total annual income is below the basic exemption limit and their net tax liability for the year is NIL, they can submit a self-declaration to the interest-paying institution, requesting that no TDS be deducted.

| Feature | Form 15G | Form 15H |

|---|---|---|

| Who can submit | Resident Individuals Below 60 Years; HUFs | Resident Senior Citizens Aged 60 Years or Above |

| Estimated Tax Liability Condition | Must Be NIL for the Financial Year | Must Be NIL for the Financial Year |

| Gross Income Condition | Aggregate Interest Income Must Not Exceed the Basic Exemption Limit | No Condition on Gross Income — Net Tax Liability Must Be NIL |

| Applicable to HUFs | Yes | No |

| Validity | One Financial Year; Must Be Renewed Annually | One Financial Year; Must Be Renewed Annually |

which you receive interest income. Once submitted, the bank or institution is legally prohibited from deducting TDS on your interest for that year.

Submitting Form 15G or Form 15H when your income is actually above the exemption limit or your tax liability is not zero is a criminal offense under Section 277 of the Income Tax Act. For amounts where the tax evaded exceeds ₹25 lakhs, punishment includes rigorous imprisonment from 6 months to 7 years plus a fine. For smaller amounts, imprisonment ranges from 3 months to 2 years, plus a fine.

Under the Income Tax Act, 2025, both Form 15G and Form 15H are replaced by a single unified declaration called Form 121, effective April 1, 2026. Form 121 consolidates the self-declaration process for all resident taxpayers regardless of age. It can be used to request NIL TDS on interest, dividends, and rent in a single submission. The key change for senior citizens: under Form 121, they must satisfy the same condition as other individuals — their total income must fall below the basic exemption limit (₹4,00,000 under the default new tax regime). The earlier relaxation under Form 15H that allowed senior citizens to submit a declaration even when gross income exceeded the exemption limit (provided deductions brought net tax to zero) has been removed.

When a taxpayer does not qualify for Form 15G or Form 15H — perhaps because their income marginally exceeds the exemption limit — they can apply to their Assessing Officer (AO) for a lower or NIL TDS certificate under Section 197. The application is made online through Form 13 on the TRACES portal. The AO reviews the taxpayer’s estimated income for the year, their tax filing history, and any outstanding tax dues. If satisfied, the AO issues a certificate specifying a reduced TDS rate or NIL deduction. The deductor must honor this certificate from the date of its issuance — it cannot be applied retroactively, and it is valid only for the financial year and period stated on the certificate.

Once TDS is deducted, the deductor must transfer the withheld amount to the Central Government’s account within prescribed timelines.

| Deduction Period | Deposit Due Date |

|---|---|

| Tax deducted from April to February | 7th of the following month |

| Tax deducted in March | 30th April of the same year |

| Government deductors (payment without challan) | Same day as the deduction |

| Government deductors (payment with ITNS 281 challan) | 7th of the following month |

Missing these deadlines triggers interest under Section 201(1A), calculated at 1.5% per month from the date of deduction to the actual date of deposit.

Under the Income Tax Act, 1961, all non-salary TDS deductions — including those under section 194A — are reported quarterly in Form 26Q. Starting from the first quarter of FY 2026-27 (transactions from April 1, 2026 onwards), Form 26Q is replaced by Form 140 under the Income Tax Act, 2025.

| Quarter | Period | Filing Due Date |

|---|---|---|

| Q1 | April 1 to June 30 | 31st July |

| Q2 | July 1 to September 30 | 31st October |

| Q3 | October 1 to December 31 | 31st January |

| Q4 | January 1 to March 31 | 31st May (of the following year) |

After filing the quarterly return, the deductor must issue a TDS certificate — currently Form 16A (to be renamed Form 131 under the Income Tax Rules, 2026) — within 15 days of the return filing due date. Payees can cross-verify the TDS credited against their account through Form 26AS, the Annual Information Statement (AIS), or the new Form 168 statement on the Income Tax e-filing portal.

Non-compliance with the TDS obligations under section 194A carries both financial and criminal consequences. The penalty framework is comprehensive and strictly enforced.

| Nature of Default | Consequence | Applicable Section |

|---|---|---|

| Failure to deduct TDS at all | Interest at 1% per month from the due date of deduction to the actual date of deduction | Section 201(1A) |

| TDS deducted but not deposited | Interest at 1.5% per month from the date of deduction to the actual date of deposit | Section 201(1A) |

| Late filing of quarterly TDS return | ₹200 per day of delay, capped at the total TDS amount | Section 234E |

| Non-filing of quarterly return (beyond 1 year) | Monetary penalty from ₹10,000 to ₹1,00,000 | Section 271H |

| Failure to issue Form 16A (Form 131) | ₹100 per day per certificate, capped at ₹10,000 | Section 272A(2)(g) |

| Interest paid without TDS deduction (business context) | 30% disallowance of the interest expense in the deductor's own tax computation | Section 40(a)(ia) |

| Intentional non-deposit of TDS (serious cases) | Rigorous imprisonment from 3 months to 7 years, plus fine | Section 276B |

The Section 40(a)(ia) disallowance is particularly impactful for businesses. If a company pays ₹5 lakhs in interest on an unsecured loan without deducting TDS, it loses the deduction on ₹1.5 lakhs (30%) of that expense when computing its taxable business income — an effective double penalty.

Many taxpayers and even some financial professionals confuse Section 194A with Section 194. The distinction matters because misclassifying the nature of income leads to incorrect TDS treatment.

| Feature | Section 194A | Section 194 |

|---|---|---|

| Type of Income Covered | Interest other than interest on securities (FDs, private loans, RDs, corporate deposits) | Dividend distributions on equity shares by domestic companies |

| Standard TDS Rate | 10% (with PAN); 20% (without PAN) | 10% (with PAN); 20% (without PAN) |

| Applicable Threshold | ₹50,000 (banks, non-senior); ₹1,00,000 (banks, senior); ₹10,000 (others) — FY 2025-26 | ₹10,000 per shareholder per financial year |

| Who Deducts | Banks, companies, firms, audit-liable individuals | Domestic companies paying dividends |

| Nature of Payment | Interest on financial instruments and loans | Corporate dividend distribution |

The similarity in TDS rates can cause confusion, but the underlying income categories are entirely different. Section 194A is about interest income; Section 194 is about dividend income.

A common question from taxpayers is: 194A which head of income does the interest fall under when filing the ITR? Interest income covered by TDS under section 194A is taxed under the head “Income from Other Sources” as per Section 56(2)(id) of the Income Tax Act, 1961. This is the default classification for interest earned from bank deposits, private loans, and corporate deposits. There is one exception: if the taxpayer’s business involves systematic money lending, or if the deposit generating interest is a direct business asset, the interest income may instead be reported under “Profits and Gains of Business or Profession” (PGBP). This classification, however, requires a clear business nexus. One critical point that every TDS payee must understand: the 10% TDS deducted under section 194A is not a final tax settlement. It is a prepayment toward your total tax liability. You must still declare the full interest income in your annual ITR, where it is taxed at your applicable slab rate. If your effective tax rate is 30%, you will owe an additional 20% beyond what was already withheld. If your effective tax rate is lower than 10%, you are entitled to claim a refund for the excess TDS by filing your return.

These errors occur repeatedly in practice and each one has a compliance or financial cost.

Splitting FDs across branches of the same bank to avoid TDS. Banks aggregate interest PAN-wide across all their branches through their core banking systems. The threshold is bank-wide, not branch-specific. This approach does not prevent TDS deduction.

Not deducting TDS on inter-company or director loans. Businesses frequently overlook TDS on interest paid to promoters, directors, or related-party lenders. This triggers the 30% disallowance under Section 40(a)(ia).

Assuming partner interest is still exempt under Section 194A. Since April 1, 2025, interest paid by a partnership firm to its partners is covered by Section 194T, not Section 194A. Firms that continue to treat this as exempt are non-compliant.

Missing TDS on penal or delayed payment interest. Commercial transactions often generate interest on delayed invoice payments. The Income Tax Act treats this as “interest” under Section 2(28A), making it fully subject to section 194A.

Submitting Form 15G or Form 15H after interest has already been credited. Banks cannot reverse TDS already deducted. Submitting declarations after the fact does not help — the taxpayer must wait to claim a refund when filing the ITR. Submit these forms at the very start of each financial year.

Submitting Form 15G when income exceeds the exemption limit. This is not just a mistake — it is a criminal offense under Section 277.

Deducting TDS despite a valid Form 15G/15H submission. Deductors sometimes overlook submitted declarations due to internal processing delays. Taxpayers should follow up to confirm their declaration is registered and request the bank to refrain from deducting TDS for that year.

Misclassifying penal bank interest as a non-TDS-applicable charge. Banks that charge penal interest on overdrawn accounts or delayed EMIs are subject to reporting obligations. Recipients of such interest credits may also have TDS implications.

The past two budgetary cycles have introduced consequential changes to the section 194A framework.

Finance Act, 2025 — Threshold Revisions (Effective April 1, 2025): The senior citizen bank interest threshold doubled from ₹50,000 to ₹1,00,000. The general bank interest threshold increased from ₹40,000 to ₹50,000. The threshold for non-banking payers rose from ₹5,000 to ₹10,000. These revisions reduce compliance friction for small depositors and senior citizens significantly.

Transition to Income Tax Act, 2025 (Effective April 1, 2026): The Income Tax Act, 1961 is being replaced by the new Income Tax Act, 2025. Section 194A transitions to Section 393(1) in this new framework. The change is structural — the table-driven approach consolidates multiple TDS provisions — but the applicable rates and thresholds remain continuous with the 1961 Act’s current parameters.

Form 121 Replaces 15G and 15H (Effective April 1, 2026): A single unified declaration replaces both forms. Senior citizens lose the additional flexibility they had under Form 15H, where gross income could exceed the exemption limit provided deductions brought the net tax to zero.

Form 140 Replaces Form 26Q (Effective April 1, 2026): Quarterly non-salary TDS statements for resident payees must be filed in the modernised Form 140 from Q1 of FY 2026-27 onward.

Cooperative Bank Exemption Change: The Income Tax Act, 2025 removes the institutional exemption on interest paid to cooperative banks, limiting it to scheduled commercial banking companies only. Cooperative societies engaged in banking no longer enjoy this exemption from April 1, 2026.

Section 194A is the provision under the Income Tax Act, 1961 that mandates Tax Deducted at Source (TDS) on interest income other than interest on securities. It covers interest from bank FDs, recurring deposits, private loans, and corporate deposits paid to resident individuals and entities.

The standard rate is 10% when a valid PAN is furnished by the payee. If PAN is not provided, the rate doubles to 20% under Section 206AA. TDS is NIL if a valid Form 15G or Form 15H (Form 121 from April 2026) has been submitted.

The threshold is ₹1,00,000 per financial year for senior citizens (aged 60 and above) earning interest from banks, cooperative societies, or post offices. This was raised from ₹50,000 by the Finance Act, 2025.

No. Interest earned on a standard savings bank account is specifically exempt from TDS under section 194A. However, it remains taxable income and must be declared under “Income from Other Sources” in the ITR.

No. Section 194A applies exclusively to payments made to resident Indians. TDS on interest paid to Non-Resident Indians (NRIs) is governed by Section 195, which involves different rates and treaty considerations.

Form 15G is for resident individuals below 60 years and HUFs whose estimated total income is below the basic exemption limit and whose tax liability for the year is zero. Form 15H is for resident senior citizens (60 years or above) whose estimated tax liability for the year is zero no condition on gross income applies. Both are replaced by Form 121 from April 1, 2026.

Not under section 194A. Partner interest was historically exempt under Section 194A(3)(iv). However, since April 1, 2025, such payments are governed by the new Section 194T, which requires 10% TDS if aggregate payments to a partner (salary, interest, commission, bonus) exceed ₹20,000 in a financial year.

Interest income subject to TDS under section 194A is classified under “Income from Other Sources” as per Section 56(2)(id). Exception: if the interest forms part of a money-lending business, it may be reported under “Profits and Gains of Business or Profession.”

Understanding 194 A of Income Tax Act is one of the most practically useful tax provisions for Indian taxpayers and business owners alike. Whether you are a salaried employee with bank FDs, a senior citizen living off interest income, or a business operator extending loans and receiving interest — section 194A directly affects your cash flows and compliance obligations.

The key takeaways for FY 2025-26 are straightforward. The threshold for bank interest has increased to ₹50,000 for general taxpayers and ₹1,00,000 for senior citizens. The TDS rate remains 10% with PAN, but doubles to 20% without it. Partnership firms must now deduct TDS on partner interest under Section 194T, not Section 194A. And from April 1, 2026, both Form 15G and Form 15H will be replaced by Form 121 under the Income Tax Act, 2025.

TDS deducted under section 194A is not a final tax. You must still declare all interest income in your ITR under “Income from Other Sources” and reconcile your actual tax liability against what has already been withheld. If you are eligible, submit Form 15G or Form 15H — now Form 121 — at the start of every financial year to avoid unnecessary deductions entirely.