Missing the income tax return filing deadline in 2026 is no longer a small procedural mistake. The Income Tax Department now uses AI-driven compliance systems, AIS/TIS verification, and automated risk assessment engines to identify delayed filings and income mismatches much faster than before. For salaried professionals, startup employees, freelancers, consultants, and business owners in Delhi NCR and Gurgaon, understanding the difference between a belated return and an updated return has become extremely important.

Assessment Year 2026-27 operates in a unique transition phase where the compliance ecosystem is becoming increasingly automated under the Income Tax Act 2025 framework, while filings are still governed largely by the Income Tax Act, 1961. In this environment, taxpayers who miss deadlines must carefully choose the correct correction route because filing the wrong type of income tax return can lead to penalties, refund loss, or even scrutiny notices.

This guide explains the difference between belated, revised, and updated income tax return filing for AY 2026-27, along with deadlines, penalties, AI-based scrutiny risks, and compliance strategies specifically relevant for Delhi NCR taxpayers.

Understanding Belated vs Updated Income Tax Return in 2026

An income tax return filed after the original due date but before December 31, 2026, is treated as a belated return under Section 139(4). This provision gives taxpayers a final opportunity to report income and complete compliance after missing the standard filing deadline.

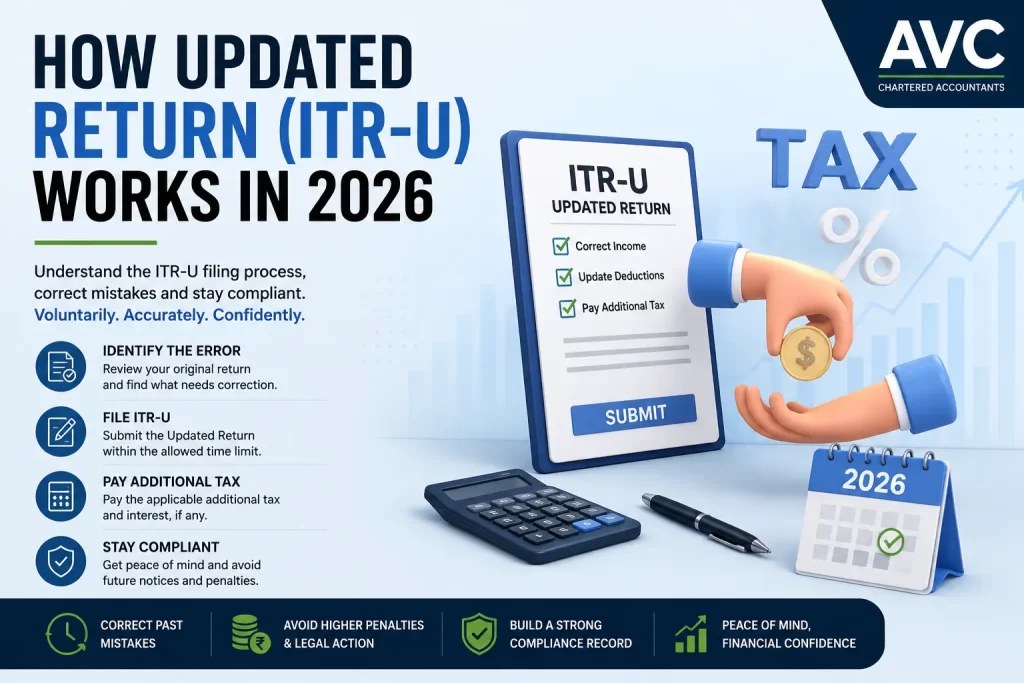

An updated return under Section 139(8A), commonly called ITR-U, is very different. It is designed for taxpayers who either failed to file entirely or later discovered major omissions in already-filed returns. The updated return system allows corrections for up to 48 months from the end of the relevant assessment year, but it comes with additional tax liability and strict restrictions.

For Delhi NCR professionals with ESOPs, capital gains, crypto investments, or freelance income, understanding this distinction is critical because AI-based scrutiny systems now compare filings against AIS, TIS, GST, and banking records automatically.

Important Deadlines for Income Tax Return Filing AY 2026-27

For AY 2026-27, the Income Tax Department has structured multiple compliance deadlines depending on the taxpayer category and return type.

Return Type

Last Date

Key Impact

Original ITR

July / August / October 2026

Full compliance benefits

Belated Return

31 December 2026

Late fee & loss restrictions

Revised Return

31 March 2027

Correction of errors allowed

Updated Return (ITR-U)

31 March 2031

Additional tax mandatory

Taxpayers in Gurgaon and Delhi NCR should avoid waiting until the last moment because AI-based verification systems become stricter during late filing periods.

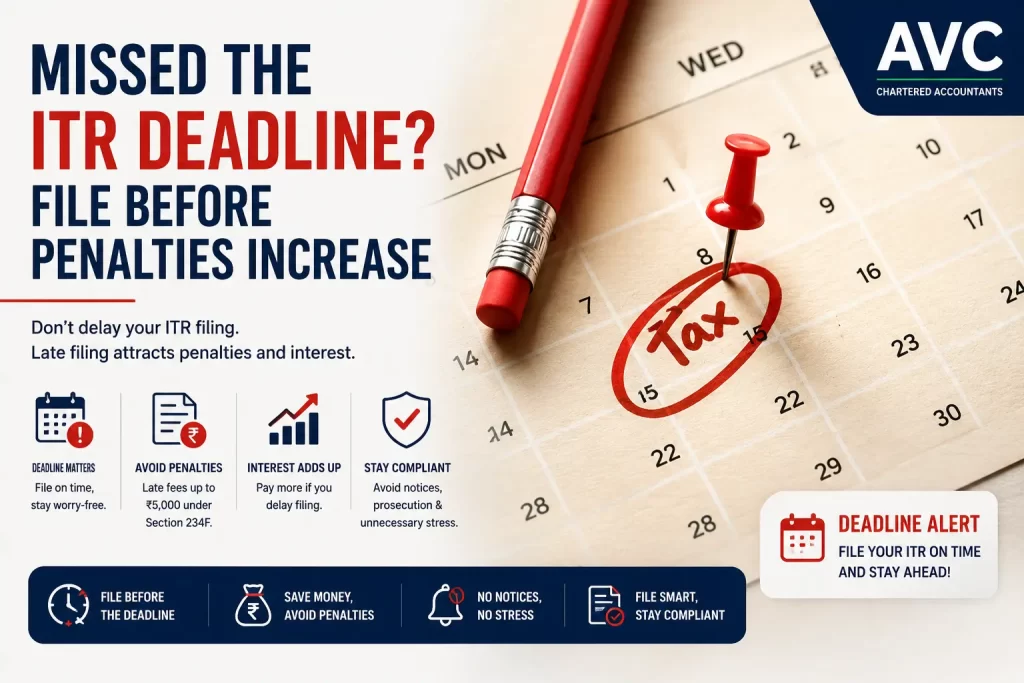

What Happens If You File a Belated Income Tax Return

A belated income tax return allows taxpayers to complete compliance after missing the original deadline, but it carries several disadvantages. Apart from late filing fees under Section 234F, taxpayers may lose the ability to carry forward certain losses, especially capital losses and business losses. In 2026, belated returns are also more likely to be reviewed by automated compliance systems because delayed filings are considered higher-risk behavior patterns. If the AIS and TIS data do not match the declared income, the department may automatically issue notices or refund hold alerts. For salaried professionals in Gurgaon who switch jobs frequently or receive bonuses, ESOPs, or stock incentives, late filing increases the probability of salary mismatch notices.

Understanding Updated Income Tax Return Under Section 139(8A)

The updated income tax return mechanism was introduced to encourage voluntary compliance. Unlike a revised return, an updated return is not merely for correcting typing mistakes or small omissions. It is mainly used when taxpayers realize they failed to disclose income properly.

However, filing an updated return comes with heavy financial consequences. The taxpayer must pay: pending tax,interest,and additional tax ranging from 25% to 70%.

The longer the delay, the higher the additional tax burden becomes. This makes updated returns significantly more expensive for Delhi NCR professionals with unreported capital gains, crypto income, foreign assets, or ESOP taxation issues.

Another major restriction is that updated returns cannot generally be used for claiming refunds or increasing refund amounts.

Revised Income Tax Return vs Updated Income Tax Return

Many taxpayers confuse revised returns with updated returns, but both serve completely different purposes.

A revised income tax return under Section 139(5) is meant for correcting genuine mistakes discovered after filing the original or belated return. In AY 2026-27, revised returns can generally be filed until March 31, 2027.

An updated income tax return, on the other hand, is intended for taxpayers who missed disclosures completely or failed to file returns at all. Because updated returns are treated as voluntary disclosures of previously hidden income, they attract additional scrutiny and higher tax costs.

For startup employees, freelancers, and investors in Gurgaon, revised returns are generally safer and less expensive compared to updated returns.

AI-Based Scrutiny for Late Income Tax Return Filing in 2026

The Income Tax Department’s Project Insight system has transformed tax compliance in India. AI-driven algorithms now compare:

AIS records, bank transactions, GST turnover, property transactions, stock market activity, and crypto exchange data. When a belated or updated income tax return is filed, the system immediately evaluates whether the taxpayer’s declared income matches the financial activity linked to the PAN. For example, if a Gurgaon-based consultant reports income of ₹12 lakh but the AIS reflects high-value foreign remittances or trading activity, the AI system may automatically flag the return for further scrutiny. This is why taxpayers should never file belated or updated returns without proper reconciliation of AIS, Form 26AS, and financial records.

Common Mistakes While Filing Belated or Updated Income Tax Return

One of the biggest mistakes taxpayers make is selecting the wrong return type. Many people attempt to use updated returns simply to claim refunds, which is not permitted under the law. Another common issue involves incorrect additional tax calculations in ITR-U filings. Taxpayers often calculate the surcharge only on base tax while ignoring interest under Sections 234A, 234B, and 234C. This can result in defective filing status.

Professionals in Delhi NCR also commonly make AIS mismatch errors by forgetting:

bank interest income, stock market gains, crypto transactions,or freelance receipts. These mismatches are now easily detectable through automated compliance systems.

Delhi NCR Taxpayer Scenarios Most Affected in 2026

The Delhi NCR region has one of the highest concentrations of complex taxpayers in India. Gurgaon’s startup ecosystem, Noida’s technology sector, and Delhi’s high-net-worth residential zones create unique compliance risks.Startup employees with ESOPs often fail to report foreign stock holdings correctly. Freelancers receiving international payments through PayPal or Upwork frequently face AIS mismatch issues. High-income professionals with multiple properties may struggle with capital gains and rental income reporting.The rise of crypto investments among young tech professionals in Gurgaon has also significantly increased scrutiny related to Schedule VDA disclosures.

How to Avoid Penalties & Notices for Late Income Tax Return Filing

Avoiding scrutiny in 2026 requires proactive compliance instead of reactive filing. Taxpayers should reconcile AIS, TIS, Form 26AS, salary records, and investment statements before filing any belated or updated return.

Taxpayers should also verify:

correct ITR form selection,proper disclosure of all income sources,capital gains calculations,foreign asset reporting,and timely e-verification.Professionals with ESOPs, foreign investments, or complex tax structures should ideally consult qualified tax experts before filing late returns.

Why Professional Assistance Matters for Belated & Updated ITR Filing

Belated and updated income tax return filing in 2026 involves much more than simply uploading numbers on the portal. AI scrutiny systems now evaluate behavioral patterns, mismatch trends, and transaction anomalies automatically.

Professional tax consultants help taxpayers:

reconcile AIS mismatches,calculate additional tax correctly,avoid defective returns,and reduce scrutiny risks.For Gurgaon professionals dealing with startup compensation, capital gains, or international income, expert review before filing can prevent expensive future litigation.

Frequently Asked Questions (FAQs)

What is a belated income tax return?

A belated return is an income tax return filed after the original due date but before December 31 of the assessment year under Section 139(4).

What is an updated return under Section 139(8A)?

An updated return or ITR-U allows taxpayers to voluntarily disclose missed income or file corrections for up to 48 months after the assessment year.

Can I claim refund through updated return?

Generally, no. Updated returns cannot usually be used for claiming or increasing refunds.

: What is the penalty for late income tax return filing in 2026?

Late filing fees under Section 234F can reach up to ₹5,000 depending on total income and filing delay.

Can I revise a belated return?

Yes. Belated returns can generally be revised before March 31, 2027.

Conclusion

The difference between belated and updated income tax return filing has become critically important in AY 2026-27. While belated returns provide a short-term correction window after missing the original deadline, updated returns act as a long-term compliance correction mechanism with significantly higher financial consequences.For taxpayers in Delhi NCR and Gurgaon, the growing use of AI-based scrutiny means that even small reporting mistakes can trigger notices, refund delays, or compliance proceedings. Accurate reconciliation of AIS, proper ITR form selection, and timely filing are now essential for avoiding future complications.Whether you are a salaried employee, startup founder, freelancer, investor, or consultant, understanding these rules properly can help you stay compliant and financially protected in 2026.