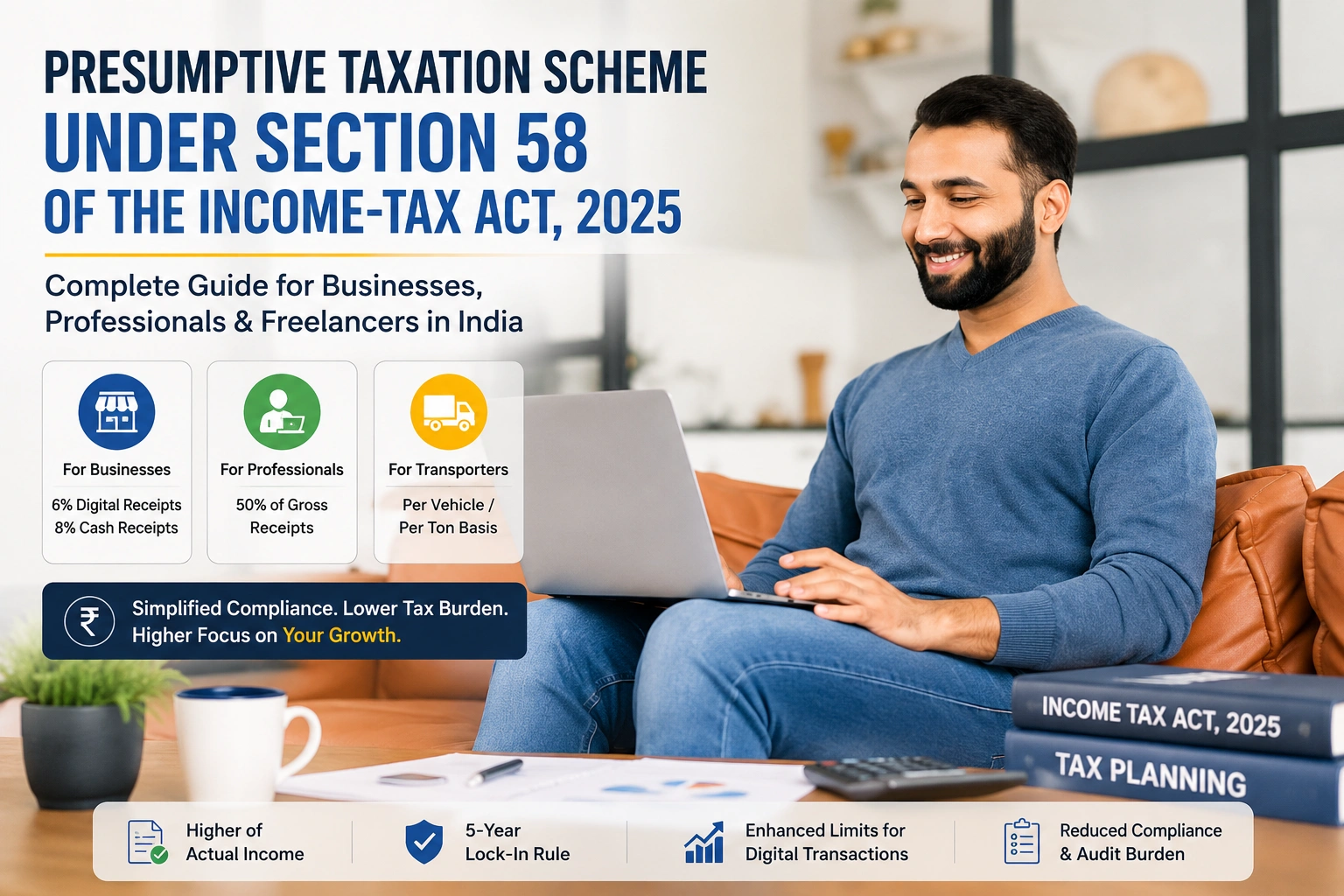

Presumptive Taxation Scheme Under Section 58 of the Income-tax Act, 2025 Complete Guide for Businesses, Professionals & Freelancers in India

Home taxation Presumptive Taxation Scheme Under Section 58 of the Income-tax Act, 2025 Complete Guide for Businesses, Professionals & Freelancers in India