-

-

Tax Services

-

Audit & Assurance

-

Business Setup

-

Accounting & Payroll

-

Advisory

-

India does not have a separate gift tax. Gifts received by any person are taxed under Section 56(2)(x) of the Income Tax Act, 1961 in the hands of the recipient not the giver. Gifts from specified relatives are fully exempt with no upper limit. Gifts from non-relatives are tax-free only up to ₹50,000 per financial year. Once that threshold is crossed, the entire amount becomes taxable not just the excess. Understanding these rules is not just a compliance requirement. Done right, gifting between family members is one of the most effective and completely legal tax-saving strategies available to Indian taxpayers. This guide covers everything the relatives list, worked examples, the car-versus-jewellery distinction, the ₹2 lakh cash penalty, clubbing traps, gift tax on ₹1 crore, and a specific section for Gurgaon residents on the state’s stamp duty advantage. All facts are verified against the Income Tax Act, 1961 and the official Income Tax Department website (incometaxindia.gov.in).

NO there is no separate gift tax in India today. India’s original Gift Tax Act (1958) was abolished on 1 October 1998. But that did not make gifts tax-free. Parliament reintroduced gift taxation inside the Income Tax Act itself. Since 1 April 2017, the governing provision is Section 56(2)(x) of the Income Tax Act, 1961, under which gifts are taxed as “Income from Other Sources” in the recipient’s hands. There is no special gift tax rate. A taxable gift is simply added to the recipient’s total income and taxed at their applicable slab rate 5%, 20%, or 30%, plus surcharge and cess.

Note for FY 2026-27 onwards: Under the new Income-tax Act, 2025, gift taxation moves to Section 92, which carries forward the same rules and ₹50,000 threshold. For FY 2025-26 (AY 2026-27), Section 56(2)(x) continues to apply.

Under Section 56(2)(x), three types of receipts are covered:

Money :any sum received without consideration, whether as cash, cheque, demand draft, NEFT, RTGS, or UPI, whether in one lump sum or accumulated across the financial year.

Immovable property : land, flat, house, or commercial property received without consideration, or for a price significantly below the stamp duty value (circle rate × area).

Specified movable property : a closed statutory list: shares and securities, jewellery, archaeological collections, drawings, paintings, sculptures, any work of art, bullion, and virtual digital assets (crypto and NFTs, added from 1 April 2022).

One important point that confuses many people: the law taxes the recipient, not the giver. The person giving a gift has no gift tax liability. The giver may separately have capital gains liability if gifting an appreciated asset but that is governed by Section 47, not gift tax.

The threshold is ₹50,000 per financial year but the way it operates surprises most people. If the aggregate value of all gifts received from non-relatives during a financial year crosses ₹50,000, the entire aggregate amount is taxable not just the portion above the threshold.

| Scenario | Amount | Taxable Amount |

|---|---|---|

| ₹45,000 from One Friend | ₹45,000 | ₹0 — Below Threshold |

| ₹55,000 from One Friend | ₹55,000 | ₹55,000 — Entire Amount Taxable |

| ₹30,000 from Friend A + ₹25,000 from Friend B | ₹55,000 Aggregate | ₹55,000 — Entire Amount Taxable |

| Five Friends Giving ₹15,000 Each | ₹75,000 Aggregate | ₹75,000 — Entire Amount Taxable |

| ₹5 Lakh Gift from Father | ₹5,00,000 | ₹0 — Relative, Fully Exempt |

| ₹10 Lakh Wedding Gift from a Colleague | ₹10,00,000 | ₹0 — Marriage Exemption Applies |

The threshold resets every 1 April. It applies to the full financial year, not per transaction or per donor.

Gifts from specified relatives are fully tax-free with no upper limit. A parent gifting ₹2 crore to a child zero tax. A spouse transferring ₹50 lakh zero tax. No paperwork requirement beyond good documentation practice.

| Relationship | Tax-Free Gift? |

|---|---|

| Spouse | ✅ Yes — No Limit |

| Brother or Sister | ✅ Yes — No Limit |

| Brother or Sister of Spouse | ✅ Yes — No Limit |

| Brother or Sister of Either Parent (Uncle/Aunt) | ✅ Yes — No Limit |

| Lineal Ascendant — Parents, Grandparents, Great-Grandparents | ✅ Yes — No Limit |

| Lineal Descendant — Children, Grandchildren | ✅ Yes — No Limit |

| Lineal Ascendant or Descendant of Spouse | ✅ Yes — No Limit |

| Spouse of Any Person Listed Above | ✅ Yes — No Limit |

| For HUF: Any Member of the HUF | ✅ Yes — No Limit |

Practical clarity on commonly confused relationships:

Father to son → ✅ exempt. Son to father → ✅ exempt. Both directions work. Mother to daughter → ✅ exempt. Daughter to mother → ✅ exempt. Brother to sister → ✅ exempt. Sister to brother → ✅ exempt. Father-in-law to son-in-law → ✅ exempt (lineal ascendant of spouse). Mother-in-law to daughter-in-law → ✅ exempt (lineal ascendant of spouse). Uncle or aunt to nephew/niece → ✅ exempt (uncle/aunt = brother/sister of either parent).

| Relationship | Taxable? |

|---|---|

| Cousin (Son or Daughter of Uncle/Aunt) | Taxable |

| Nephew / Niece | Taxable |

| Friend or Colleague | Taxable |

| Business Partner | Taxable |

| Girlfriend / Boyfriend | Taxable |

| Fiancé / Fiancée (Before Marriage Is Solemnised) | Taxable |

Cousins are a common misconception. An uncle is a relative, but a cousin the uncle’s child is not on the statutory list.

Beyond the relatives list, certain occasions create unconditional exemptions that apply even from strangers and non-relatives:

On the occasion of your own marriage :Any gift cash, jewellery, property received at the time of your wedding, from anyone, is fully exempt. No upper limit. This applies only to the person getting married. Birthday gifts, anniversary gifts, Diwali gifts, and festival gifts from non-relatives do not qualify under this clause.

Under a will or by inheritance: Money or property received after someone’s death, through a will or intestate succession, is fully exempt at the point of receipt. Capital gains may apply if you later sell the inherited asset.

In contemplation of death: Gifts made by a seriously ill person anticipating imminent death legally called donatio mortis causa are exempt.

From registered charitable and religious trusts and institutions:Gifts from trusts registered under Section 12A, 12AA, or 12AB, and institutions under Section 10(23C), including hospitals and educational institutions, are fully exempt.

From local authorities: Gifts received from a municipality, panchayat, cantonment board, or port trust are exempt.

When a gift is taxable, the amount added to income depends on what is being gifted:

Cash: The full amount received.

Immovable property received without consideration: The stamp duty value (circle rate × area) is the taxable amount, provided it exceeds ₹50,000.

Immovable property received at below-market price: If the stamp duty value exceeds the actual consideration paid, and the difference is more than the higher of ₹50,000 or 10% of the consideration, the excess stamp duty value is taxable. (The 10% safe harbour was introduced by Finance Act 2020; previously it was 5%.)

Specified movable property received without consideration: The Fair Market Value (FMV) is the taxable amount if FMV exceeds ₹50,000.

Specified movable property received at below-FMV: If (FMV − consideration paid) exceeds ₹50,000, the shortfall is taxable.

Shares and securities: FMV is computed per CBDT prescribed method average of highest and lowest quoted price on the date of receipt for listed shares; net asset value/book value per Rule 11UA for unlisted shares.

Virtual Digital Assets (crypto/NFTs): Taxable at FMV on date of receipt. No deduction for cost of acquisition is available for gifted VDAs.

“Gift tax on 1 crore in India” is one of the most searched questions in this space. Here are four real scenarios with actual numbers.

Scenario 1 :Gift from your father (relative) Your father gifts you ₹1 crore via bank transfer. Tax on recipient: ₹0. Father is a lineal ascendant a specified relative. Fully exempt with no upper limit. Income later earned on this ₹1 crore is taxed in your hands (no clubbing applies for parent-to-adult-child gifts).

Scenario 2 :Gift on your wedding day (from anyone) A business associate gifts you ₹1 crore on your wedding day. Tax on recipient: ₹0. Marriage occasion exemption applies to any donor, any amount. However, do not receive more than ₹2 lakh in cash from any one person (Section 269ST explained below).

Scenario 3: Gift from a friend (non-relative) Your friend gifts you ₹1 crore by bank transfer. The entire ₹1 crore is added to your “Income from Other Sources.” Approximate tax:

This is illustrative. The exact figure depends on your regime (old/new), other income, and applicable surcharge slab.

Scenario 4: Property “sold” by a friend at below market value Your friend sells you a flat for ₹70 lakh. Stamp duty value is ₹1 crore. Difference = ₹30 lakh. 10% of ₹70 lakh = ₹7 lakh. Since ₹30 lakh exceeds ₹7 lakh, ₹30 lakh is added to your income from other sources. The seller may also face capital gains implications under Section 50C. Undervalued property transactions are closely watched.

This is where it gets genuinely interesting and it is the legal principle behind the viral CA reel.

Under Section 56(2)(x), only “specified movable property” is taxable when gifted. The law defines this as a closed list: shares and securities, jewellery, archaeological collections, drawings, paintings, sculptures, works of art, bullion, and virtual digital assets (crypto/NFTs).

A motor car is not on this list. So if a friend gifts you a car worth ₹15 lakh, Section 56(2)(x) simply does not apply no gift tax.

There is a second legal layer. Under Section 2(14) of the Income Tax Act, a “capital asset” is defined as any property held by a person. But personal-use movable property called “personal effects” is specifically excluded. The definition reads: “personal effects, that is to say, movable property including wearing apparel and furniture, but excluding jewellery.” A personal-use car is a personal effect. So it is also excluded from the capital asset definition. This means even if you later sell the gifted car, no capital gains tax applies.

The CA’s advice in the reel was perfectly correct and here is the exact legal basis.

Jewellery is explicitly named in Section 56(2)(x)’s closed list of movable property. A gift of jewellery worth ₹3 lakh from a non-relative friend taxable in full. And in Section 2(14), the personal effects exclusion specifically says “excluding jewellery” meaning jewellery remains a capital asset. When you sell gifted jewellery, the profit is taxable under capital gains. This car-vs-jewellery contrast is one of the most important practical distinctions in Indian gift taxation, and almost no mainstream article explains it clearly.

The relatives exemption removes income tax on the gift itself. But there is a separate rule that catches income earned on gifted money and many people walk into it unknowingly.

Gift to your spouse: The gift is tax-free (spouse is a relative). But any income earned from that gifted amount FD interest, rental income, dividends is “clubbed” back to you and taxed in your hands under Section 64(1)(iv). Example: you gift ₹20 lakh to your wife; she puts it in a fixed deposit earning ₹1.4 lakh interest. That ₹1.4 lakh is added to your taxable income, not hers.

Gift to a minor child: Income from the gifted amount is clubbed with the higher-earning parent (Section 64(1A)). A small exemption of ₹1,500 per child per year applies.

Gift to parents or adult children: No clubbing. The income is genuinely taxed in their hands at their own slab rate.

This is why gifting to parents is one of the most effective and completely legal tax-saving strategies available. If your parents are senior citizens or in a lower tax bracket, their income from the gifted amount is taxed at their rate not yours. The gift itself is tax-free (they are relatives). There is no clubbing. And senior citizens have a higher basic exemption limit. Document it with a gift deed and a clear bank trail.

This is the most overlooked trap in gift taxation and every person who receives a large cash gift as a “tax-free relative gift” must know it.

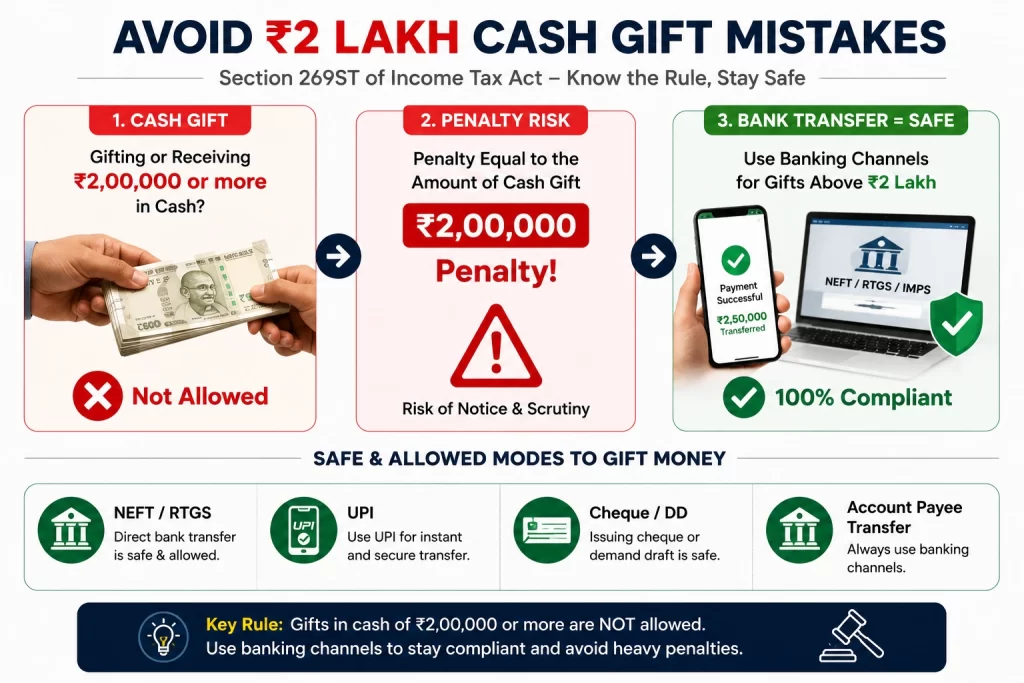

Section 269ST of the Income Tax Act prohibits receiving ₹2,00,000 or more in cash from one person on:

The penalty for violating this under Section 271DA is 100% of the amount received imposed on the receiver, not the payer.

This applies even to otherwise tax-free gifts from relatives.

If your father gifts you ₹10 lakh in cash, the gift is exempt from income tax (father is a relative under Section 56(2)(x)). But if received in cash, Section 269ST is violated. The penalty: ₹10 lakh. On a tax-free gift. That is not a typo.

The rule: All large gifts from relatives or non-relatives must be received via account payee cheque, demand draft, NEFT, IMPS, UPI, or other electronic mode. Never in cash above ₹2 lakh. The only entities exempt from Section 269ST are the Government, banking companies, post office savings banks, and co-operative banks.

When you eventually sell an asset you received as a gift, capital gains tax applies. Two things carry over from the original owner:

Cost of acquisition: The cost is whatever the original owner paid, not the value on the date of the gift.

Holding period: Your holding period includes the time the donor held the asset. So if your father bought shares in 2018 and gifted them to you in 2023, and you sell in 2025, the holding period is from 2018 — making them long-term capital assets.

The post-July 2024 change (Finance Act, 2024):

For immovable property sold on or after 23 July 2024, LTCG is taxed at 12.5% without indexation (previously 20% with indexation). However, if the property was acquired before 23 July 2024, you can choose whichever option results in lower tax — 12.5% without indexation, or 20% with indexation. Use whichever is beneficial; the law permits both calculations and you pay the lower figure. For listed equity and equity mutual funds: LTCG above ₹1,25,000 is taxed at 12.5% (no indexation). STCG (held under 12 months) is taxed at 20%.

For immovable property (land, flat, house), a registered gift deed is legally mandatory under the Transfer of Property Act and the Registration Act, 1908. Registration must happen at the Sub-Registrar’s office. For cash and movable property, a gift deed is not legally required but is strongly recommended. It is your primary defence if the Income Tax Department sends a Section 68 notice treating the amount as an “unexplained cash credit.” A documented, signed gift deed with a clear relationship declaration and bank trail is evidence of genuineness. A proper gift deed should contain: full names and addresses of donor and donee, their relationship, a precise description of the asset being gifted, a declaration that the gift is voluntary and without consideration, the date and place of execution, and signatures of two witnesses.

If you are in Gurgaon or anywhere in Haryana, gifting immovable property to a blood relative carries a benefit that is unique to this state and missed by almost every mainstream article.

Under income tax law: A gift of property to a relative (parents, children, siblings, spouse) is fully exempt under Section 56(2)(x). Zero income tax.

Under Haryana stamp duty law: Per Haryana Notification No. S.O. 62/C.A. 2/1899/S. 9/2014 (dated 16 June 2014), issued under Section 9(1)(a) of the Indian Stamp Act, stamp duty is remitted in full (0%) on instruments transferring immovable property to parents, children, grandchildren, siblings, and spouses. The result: if a Gurgaon parent transfers a flat to their child, the transaction attracts zero income tax and zero stamp duty. You pay only the registration fee — 1% of the property value, capped at ₹50,000. For a ₹1 crore flat, this is a saving of approximately ₹5–7 lakh in stamp duty (the rate applicable to non-relatives) plus complete exemption from income tax.

Important: Stamp duty notifications can be amended. Before registering any gift deed, verify the current applicable rate with your Sub-Registrar or at revenueharyana.gov.in and jamabandi.nic.in. Also ensure the stamp duty value is computed on the higher of declared value or the current circle rate for that locality.

Failing to report gifts even exempt ones is one of the most common mistakes that leads to unnecessary notices.

Taxable gifts (from non-relatives, above ₹50,000): Declare under “Income from Other Sources” Schedule OS in ITR-2 or ITR-3.

Exempt gifts (from relatives, on marriage, by inheritance): Report under Schedule EI (Exempt Income). This tells the Income Tax Department that the amount was received legitimately and explains why no tax was paid. It takes two minutes and eliminates future scrutiny risk.

Why this matters: Every bank transfer above a certain threshold appears in your Annual Information Statement (AIS), which is generated automatically by the department and shared with you before you file. A mismatch between AIS and your ITR triggers automated scrutiny under Section 143(1). Reporting exempt gifts in Schedule EI pre-empts that mismatch.

Clubbed income: If you gifted money to your spouse and income from it is clubbed back to you, that income must be disclosed in your ITR not your spouse’s.

| Gift | Taxable? | Why |

|---|---|---|

| ₹10 lakh cash from father | No (if via bank) | Father is treated as a relative under the Income Tax Act. |

| ₹10 lakh cash from friend | Yes — Full Amount | Friend is a non-relative and the gift exceeds ₹50,000. |

| Car worth ₹15 lakh from friend | No | Car is not classified as a specified movable property. |

| Jewellery worth ₹3 lakh from friend | Yes — Full Amount | Jewellery is a specified movable property under tax provisions. |

| Wedding gift of ₹5 lakh from colleague | No | Gifts received on the occasion of marriage are exempt. |

| Property inherited via will | No | Inheritance through a will is exempt from tax. |

| Crypto worth ₹80,000 from friend | Yes | Virtual Digital Assets (VDA) are treated as specified movable property. |

| ₹2 lakh cash from father | Tax-Free but Section 269ST Risk | Gift is exempt, but cash receipt of ₹2 lakh or more may violate Section 269ST. |

It depends on the source and amount. Gifts from specified relatives are fully tax-free with no upper limit. Gifts from non-relatives are tax-free only up to ₹50,000 in a financial year. Beyond that, the entire amount is taxable as income from other sources.

There is no upper limit for gifts between specified relatives. A parent can gift ₹5 crore to a child zero tax. The no-limit exemption applies only to the relatives defined under Section 56(2)(x).

There is no separate gift tax rate. The taxable gift amount is added to your total income and taxed at your applicable income slab rate 5%, 20%, or 30%, plus applicable surcharge and cess.

No, if it is for personal use. A motor car is not included in the definition of “specified movable property” under Section 56(2)(x), so receiving a car as a gift is not taxable even from a non-relative.

Yes, if it comes from a non-relative and the total value exceeds ₹50,000 in the financial year. Jewellery is explicitly listed as “specified movable property” under Section 56(2)(x).

No. A father is a “lineal ascendant” of the son a specified relative under the Income Tax Act. Gifts from a father to a son are fully exempt with no upper limit.

Under Haryana state notification (2014), stamp duty is fully remitted (0%) on property gifted to blood relatives (parents, children, siblings, spouse). Only the registration fee (1% of value, capped at ₹50,000) applies. Verify the current rate with your Sub-Registrar before proceeding.

No not above ₹2 lakh. Even if the gift itself is fully tax-exempt, receiving ₹2 lakh or more in cash from a single person in a single day or for one occasion violates Section 269ST. The penalty under Section 271DA is 100% of the cash amount received. Always use bank transfer or cheque.

Assuming all family gifts are automatically tax-free. They are but only from specified relatives as defined in Section 56(2)(x). Cousins, nephews, nieces, and friends are not relatives under the law.

Receiving large cash gifts from relatives. The gift may be exempt under Section 56(2)(x). The cash receipt above ₹2 lakh is still a violation of Section 269ST with a 100% penalty.

Gifting to a spouse to split income. The gift is tax-free. The income earned on it is clubbed back to you under Section 64. The tax saving is illusory.

Not reporting exempt gifts in ITR. Large transfers appear in your AIS. An unreported gift even an exempt one creates a mismatch that triggers automated scrutiny. Report all significant gifts in Schedule EI.

Confusing the donor’s tax position with the recipient’s. The giver has no gift tax. But if the giver is transferring an appreciated capital asset, they may have capital gains liability at the time of gifting (Section 45 applies; Section 47 provides relief only in specific cases).