Every company that is registered in India under the Goods and Services Tax (GST) is required to uphold adherence to legal requirements. On the other hand, noncompliance may result in the cancellation of GST registration, a severe compliance problem that may disrupt business operations and pose a financial risk.

In this detailed guide, we explain:

Why GST registration gets cancelled

How revenue officers initiate cancellation

How businesses should respond to show-cause notices

The revocation process to reinstate GST registration

Section 29 of the CGST Act, 2017 – Registration cancellation

GST Rules 2017 – Procedure for cancellation & revocation

Specific forms prescribed under the GST Rules for notices and responses

3. Common Reasons Why GST Registration Gets Cancelled

Cancellation is generally initiated when one or more of the following occur:

A. Failure to File Returns

One of the most frequently mentioned reasons is failing to file returns for consecutive tax periods. If returns are not received, GST authorities have the right to cancel registration and issue a show-cause notice.

B. Non-Compliance or Fraud

Revenue authorities may cancel if:

Information provided at registration was false

The business is not traceable at the declared address

There is evidence of tax evasion

C. Demise / Insolvency / Business Closure

If a business legally closes or the proprietor dies, registration can be cancelled.

4. How the GST Cancellation Procedure Works (Step by Step)

In order to adhere to natural justice, cancellation of an officer’s motion must follow a specific procedure:

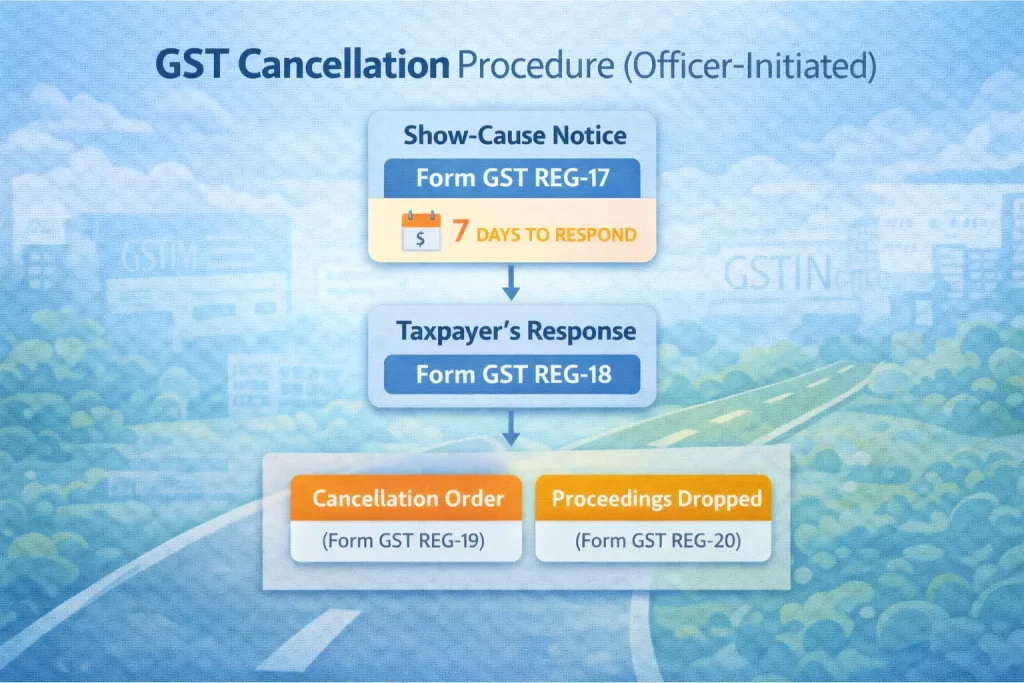

Step 1: Issue of Show-Cause Notice (Form GST REG-17)

The taxpayer receives a notice outlining the reasons for the proposed cancellation and requesting justifications for not proceeding with the cancellation.

Typical timeline: Usually 7 days to respond (unless extended)

Step 2: Taxpayer’s Response (Form GST REG-18)

The taxpayer must reply with:

Grounds against cancellation

Supporting documents

Return filings (if pending)

Evidence of business continuity

Common mistakes business owners make at this stage:

Unsigned / incomplete replies

No documentary evidence

Ignoring the deadline

Step 3: Officer’s Order

After reviewing the reply, the officer may:

Drop the cancellation proceedings (Form GST REG-20)

Issue a final cancellation order (Form GST REG-19)

Once cancelled, the taxpayer is notified and all GST obligations cease.

5. How to Apply for Revocation of Cancelled GST Registration

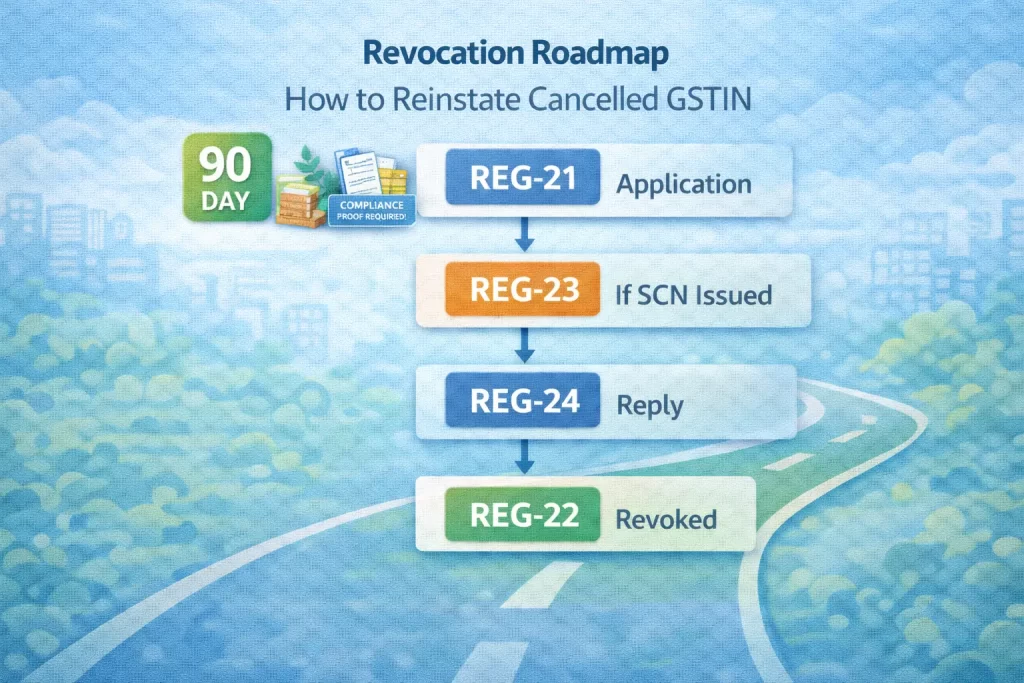

If your registration is cancelled, you can apply for revocation i.e., reinstating GST registration subject to conditions:

Eligibility

Cancellation must have been initiated on officer’s motion

Business needs to demonstrate compliance (returns, tax payments)

Application must be within the statutory time window (typically 90 days)

Step-by-Step Revocation Process

Revocation Application (Form GST REG-21):

Submit this form with:

Reason for revocation

Outstanding returns served

Tax payments evidence

Officer’s Review:

Authority examines:

Past compliance

Pending dues

Reasonableness of application

Possible Show-Cause Notice (Form GST REG-23):

If the authority is not satisfied, a notice is issued for further clarification.

Reply to Revocation SCN (Form GST REG-24):

Detailed response with documents.

Final Outcome:

Revocation Order (Form GST REG-22) If satisfied

Rejection (Form GST REG-05) If not

Note: Forms must be submitted within specified timeframes.

6. Practical Pitfalls & Compliance Tips

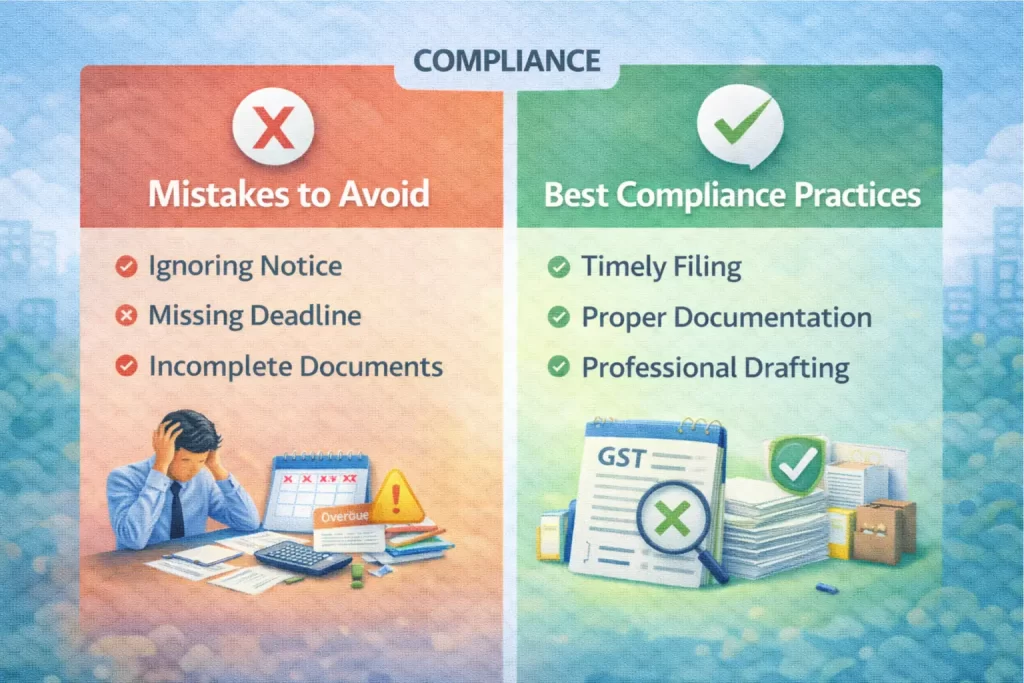

Even when statutory procedures are followed, businesses often slip up due to:

Common Mistakes

Missing show-cause notice deadlines

Attaching incomplete evidence

Not clearing pending returns before applying for revocation

Filing late replies without an error explanation

Practical Compliance Tips

✔ Maintain timely GST return filings ✔ Reconcile GSTR-2B and GSTR-3B every month ✔ Keep proof of business existence & operations ✔ Respond in Form GST REG-18 comprehensively ✔ Consult a professional for notice replies

7. Timeline Summary (Flow Chart)

Stage 1 – Show-Cause Notice (GST REG-17)

Time Window: Usually, 7 days to respond

Stage 2 – Reply by Taxpayer (GST REG-18)

Time Window: As per the notice

Stage 3 – Final Cancellation Order (GST REG-19)

Time Window: Once reviewed

Stage 4 – Revocation Application (GST REG-21)

Time Window: Within 90 days (or as allowed)

Stage 5 – Final Revocation Order (GST REG-22)

Time Window: Post review

8. FAQ

What is GST cancellation, and how does it happen?

GST cancellation is the withdrawal of GSTIN due to non-compliance, and it occurs after proper notice and opportunity to respond.

Which GST form is used for cancellation?

Show-cause: Form GST REG-17

Final cancellation: Form GST REG-19

Can GST registration be revoked after cancellation?

Yes, through Form GST REG-21 before the specified statutory window closes.

How many days do I have to respond to a GST cancellation notice?

Typically around 7 days, but timelines may vary based on notice.

What documents are needed for revocation?

Return filings, proof of business operations, tax payment receipts, and a detailed explanation for compliance.

9. Why Professional Help Matters

Responding to GST cancellation and revocation notices requires:

Accurate legal interpretation

Timely replies with correct forms

Strong supporting evidence

Understanding of procedural fairness

At AVC India, our GST experts: ✔ Review notices carefully ✔ Draft replies with legal precision ✔ Help reconcile overdue returns ✔ Guide you through revocation process

Contact AVC India to protect your GST registration and maintain uninterrupted compliance.