Mistakes in tax returns are more common than most taxpayers realize.

Missed bank interest, forgotten capital gains, incorrect deductions, or unreported foreign income can easily lead to compliance risks. Recognizing this reality, the Indian government introduced Section 139(8A) through the Finance Act 2022, allowing taxpayers to correct past errors using an Updated Return (ITR-U).

This mechanism allows individuals, professionals, startups, and MSMEs to voluntarily disclose missed income and correct errors, even years after the original filing deadline.

In this comprehensive guide by AVC India, we explain:

What an Updated Return under Section 139(8A) is

Who can file ITR-U and when

Additional tax under Section 140B

Real-world examples for freelancers, startups, and MSMEs

Step-by-step ITR-U filing process

Compliance strategy to avoid income tax notices

What Is an Updated Return (ITR-U)?

An Updated Return is a special tax return filed under Section 139(8A) of the Income Tax Act, 1961 that allows taxpayers to correct previously filed returns or declare missed income.

Unlike revised returns, updated returns are designed primarily for voluntary disclosure of under-reported income.

The objective is simple:

Encourage voluntary compliance while reducing litigation and tax disputes.

The government introduced this mechanism as part of its “trust-based tax governance” approach.

Difference Between Revised Return and Updated Return

Feature

Revised Return

Updated Return

Purpose

Correct mistakes

Declare missed income

Filing deadline

31 December of the assessment year

Up to 48 months after AY

Additional tax

No additional tax

25%–70% additional tax

Refund

Can increase the refund

Refund cannot increase

Loss

Can increase loss

Loss can only decrease

Filing frequency

Multiple revisions allowed

Only once

This means ITR-U should only be used for compliance correction, not tax planning.

Who Can File Updated Return (Section 139(8A))?

Any taxpayer can file an updated return, including:

Individuals

Freelancers and consultants

Startups and founders

Companies and LLPs

MSMEs and partnership firms

NRIs with Indian income

Updated returns can be filed whether or not an original return was filed.

Situations Where ITR-U Is Useful

Updated return filing is commonly used when taxpayers discover:

Missed Income

Examples include:

Bank interest income

Dividend income

Freelance payments not reported

Capital gains from shares or crypto

Incorrect Tax Calculation

Errors in:

Slab calculation

Advance tax estimation

Foreign tax credit claims

Incorrect Deductions

Sometimes deductions are wrongly claimed under:

Section 80C

Section 80D

Section 80G

Wrong Tax Regime Selection

Taxpayers who mistakenly chose the wrong regime may need corrections.

Situations Where an Updated Return Cannot Be Filed

The law restricts ITR-U in several cases.

An updated return cannot be filed if:

It reduces tax liability

It increases refund amount

It increases loss amount

Search or seizure proceedings have started

Assessment proceedings are ongoing

Prosecution has begun under the Income Tax Act

The mechanism exists strictly for additional disclosure of income.

Time Limit to File Updated Return

Following the Finance Act amendments, taxpayers can file updated returns up to 48 months from the end of the relevant assessment year.

Example

Financial Year

Assessment Year

Last Date for Updated Return

FY 2022-23

AY 2023-24

31 March 2028

FY 2023-24

AY 2024-25

31 March 2029

This extended window provides taxpayers ample time to correct mistakes discovered later.

Additional Tax under Section 140B

Filing an updated return comes with an additional tax cost.

The government charges a compliance premium depending on how late the correction is made.

Time after Assessment Year

Additional Tax

Up to 12 months

25% additional tax

12–24 months

50% additional tax

24–36 months

60% additional tax

36–48 months

70% additional tax

This additional tax applies to:

Tax payable

Interest under sections 234A, 234B, and 234C

Late filing fees

The longer a taxpayer waits, the higher the penalty.

Step-by-Step Process to File Updated Return (ITR-U)

Here is the practical process followed by tax professionals.

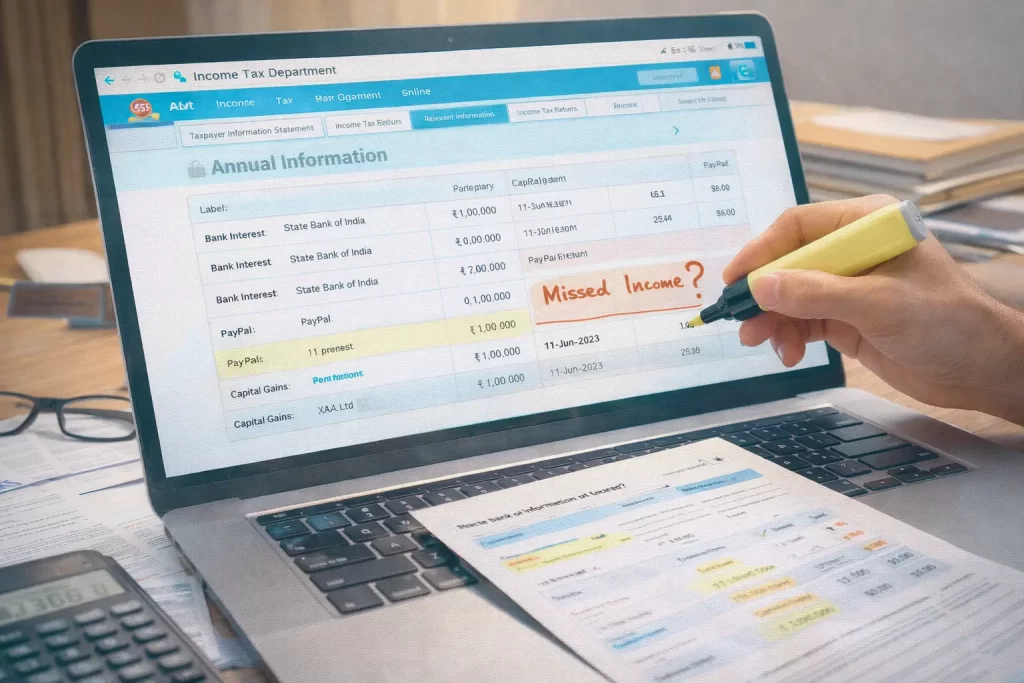

Step 1: Review AIS and Form 26AS

Analyze the Annual Information Statement (AIS) and Taxpayer Information Summary (TIS) to identify mismatches.

Step 2: Identify Missing Income

Reconcile:

Bank statements

capital gains statements

business income records

foreign assets or income

Step 3: Choose the Correct ITR Form

Select the same ITR form used previously (ITR-1, ITR-2, ITR-3 etc.).

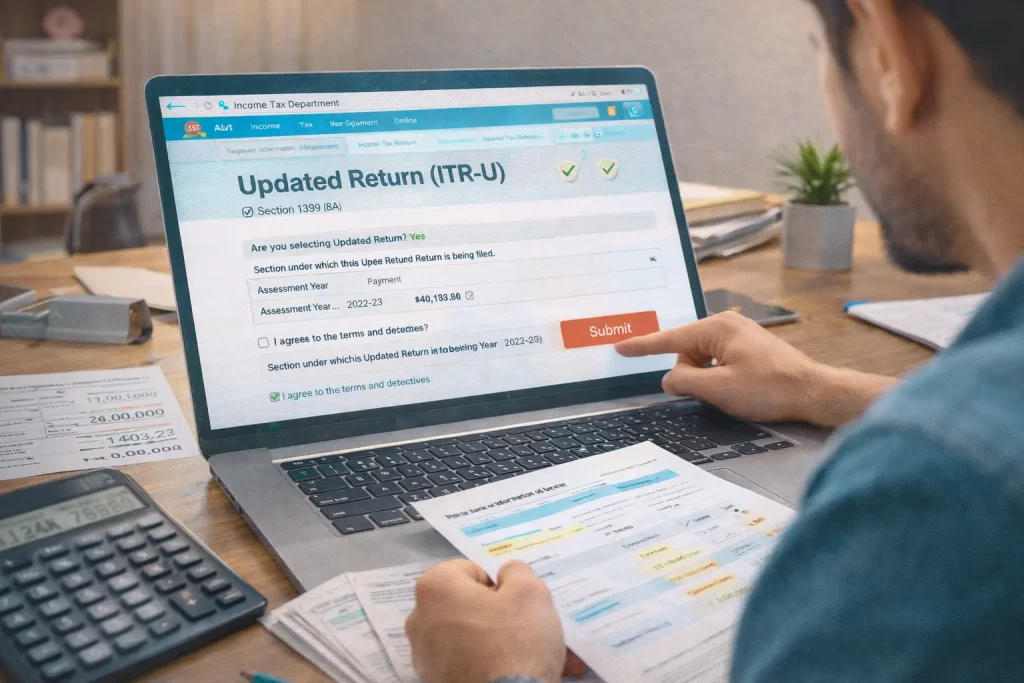

Step 4: Select Filing Type

Choose “Updated Return under Section 139(8A)” on the income tax portal.

Step 5: Pay Additional Tax

Before filing, tax must be paid using Challan ITNS 280.

Step 6: Upload ITR-U

Submit the updated return through the Income Tax e-filing portal.