Tax saving is no longer just about investing in LIC or PPF.

With the introduction of the new tax regime, updates from Budget 2026, and the upcoming Income Tax Act 2025, the way Indians save tax has fundamentally changed.

Today, this guide is all about the Tax Saving Strategies India 2026. Tax planning is about strategy, timing, and choosing the right structure; not just deductions.

In this guide by AVC India, we break down:

Latest tax-saving rules for FY 2025–26

Old vs New tax regime comparison

Best tax-saving strategies for salaried, freelancers & businesses

Investments that actually save tax

Year-end planning checklist

These are all the Tax Saving Strategies India 2026.

Understanding the New Tax Environment (2026)

India is currently in a transition phase:

Old Income Tax Act, 1961 → transitioning to Income Tax Act, 2025

New Tax Regime → now the default option

Increased focus on digital tracking (AIS, TIS)

👉 This means:

Tax saving is shifting from “investment-based” to “strategy-based planning.”

Old vs New Tax Regime: Which Saves More Tax?

This is the most searched tax question in India right now.

Feature

Old Tax Regime

New Tax Regime

Tax rates

Higher

Lower

Deductions

Allowed

Mostly not allowed

Complexity

High

Simple

Best for

High deductions

Low deductions

Key Insight (2026)

Under the new regime:

Income up to ₹12,00,000 → ZERO tax (Section 87A rebate)

With ₹75,000 standard deduction → ₹12.75 lakh tax-free income

This changes everything for salaried individuals.

When to Choose Old Regime

Choose old regime if you have:

High deductions (₹2–4 lakh+)

Home loan interest

Multiple tax-saving investments

When to Choose New Regime

Choose new regime if:

You don’t invest heavily

You want simplicity

You are a freelancer or startup founder

How to Choose the Best Tax Saving Strategies India 2026 Based on Your Income

Choosing the right tax saving strategy is no longer about blindly investing in 80C instruments. In 2026, the best tax saving strategies depend on your income level, financial goals, and the tax regime you choose.

A one-size-fits-all approach does not work anymore.

Below is a practical breakdown to help you select the most effective tax saving strategies India 2026 based on your income bracket.

1. Income Up to ₹12 Lakh (New Regime Advantage Zone)

If your taxable income is within ₹12 lakh:

You may pay zero tax due to Section 87A rebate

With ₹75,000 standard deduction → up to ₹12.75 lakh becomes tax-free

Best Strategy:

Prefer New Tax Regime

Avoid unnecessary investments just for tax saving

Focus on liquidity and wealth building instead of locking funds

Ideal for:

Young professionals

First-job earners

Freelancers with moderate income

2. Income Between ₹12 Lakh – ₹20 Lakh (Decision Zone)

This is the most critical income bracket where choosing the right strategy matters.

You must compare:

Old Regime (with deductions) vs

New Regime (lower tax rates)

Best Strategy:

Choose Old Regime if:

You can claim ₹2–4 lakh deductions (80C, 80D, HRA, home loan)

Choose New Regime if:

You don’t have significant deductions

You prefer simplicity and higher cash flow

Ideal for:

Mid-level salaried employees

Consultants

Growing freelancers

3. Income Above ₹20 Lakh (Optimization Zone)

At higher income levels, tax planning becomes more strategic.

Best Tax Saving Strategies India 2026 for this group:

Salary restructuring (HRA, allowances)

Capital gains planning

Tax-efficient investments

Business expense optimization (for professionals)

In many cases:

Old Regime may still be beneficial if deductions are high

But New Regime works better if deductions are limited

Ideal for:

Senior professionals

High-income freelancers

Business owners

4. Freelancers & Business Owners (Flexible Strategy Zone)

Unlike salaried individuals, freelancers have more control.

Best strategies:

Use presumptive taxation (44AD / 44ADA)

Claim business expenses strategically

Align GST and income reporting

Plan advance tax properly

Decision:

New Regime → better for simplicity

Old Regime → better if deductions are high

Biggest Advantage: Flexibility in structuring income

5. Startups & Founders (Long-Term Strategy Zone)

For founders, tax saving is not just about current savings.

It impacts:

Funding

Valuation

Profitability

Best strategies:

Choose the right business structure

Plan losses and carry-forward properly

Optimize ESOP taxation

Align personal and business tax planning

Key Decision Formula (Simple Rule)

Use this thumb rule:

Low deductions → New Regime

High deductions → Old Regime

High income → Strategic planning required

Common Mistakes to Avoid

Many taxpayers:

❌ Invest ₹1.5 lakh in 80C without checking if it actually saves tax ❌ Ignore new tax regime benefits ❌ Copy others’ strategies

👉Instead:

Choose tax saving strategies based on your actual financial situation, not assumptions.

Top Tax Saving Strategies (FY 2025–26)

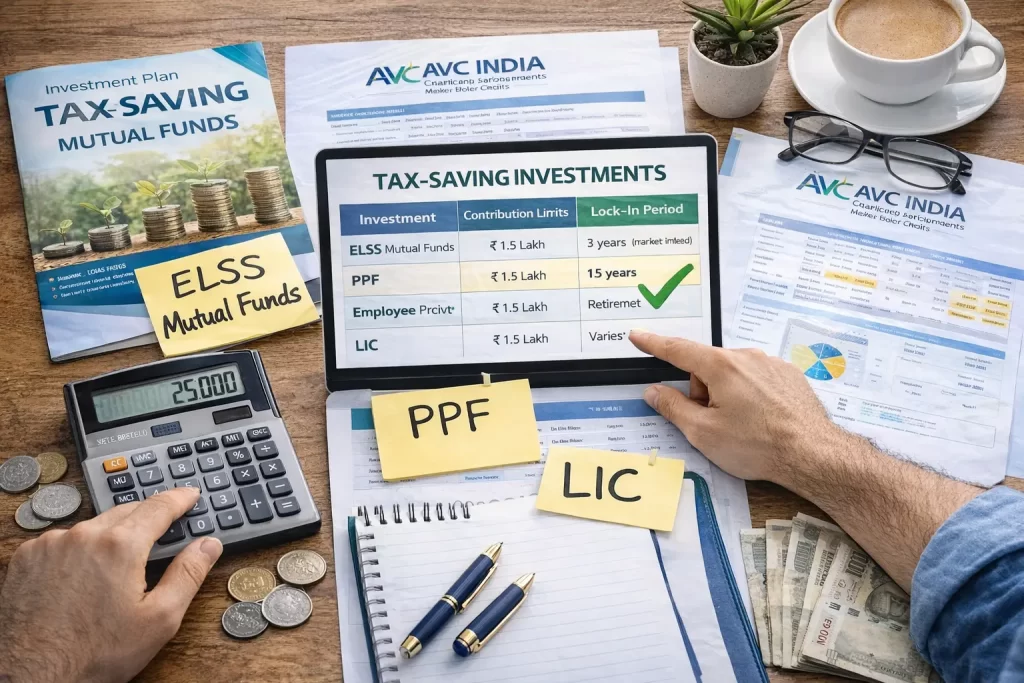

1. Smart Use of Section 80C (₹1.5 Lakh Deduction)

Still one of the most powerful tools under the old regime.

Best Options:

ELSS Mutual Funds

PPF

Life Insurance

EPF

Strategy Tip: ELSS offers both tax saving + market returns, making it superior for long-term wealth.

2. Health Insurance (Section 80D)

You can claim:

₹25,000 (self & family)

₹50,000 (senior citizens)

Not just tax saving, this is risk management + compliance benefit

3. Home Loan Benefits (Section 24 + 80C)

₹2 lakh deduction on interest

Principal under 80C

Best for:

Salaried individuals

Long-term asset builders

4. Salary Structuring for Tax Saving

If you’re salaried, your CTC structure matters.

Tax-saving components:

HRA (House Rent Allowance)

LTA (Leave Travel Allowance)

Food allowance

Fuel reimbursement

This is often ignored but can save ₹50,000–₹1 lakh/year

5. Capital Gains Tax Planning

For investors:

Use long-term holding benefits

Offset losses strategically

Plan asset selling across financial years

Critical for:

Stock traders

Crypto investors

Real estate owners

6. Presumptive Taxation (Freelancers & MSMEs)

Under Sections 44AD / 44ADA:

Pay tax on a fixed % income

No need for detailed bookkeeping

Ideal for:

Freelancers

Consultants

Small business owners

Tax Saving Strategies India 2026 for Salaried, Freelancers & Businesses

Salaried Individuals

Best approach:

Compare regimes every year

Optimize salary structure

Use 80C + 80D fully

Maximize standard deduction

Freelancers & Consultants

Focus on:

Presumptive taxation

Expense tracking

GST + income alignment

Biggest mistake: Not planning advance tax → leads to penalties

Startups & Founders

Strategy:

Choose the correct entity (Pvt Ltd vs LLP)

Optimize losses & carry forward

Plan ESOP taxation

Tax planning directly impacts funding & valuation

MSMEs

Focus on:

GST + income tax alignment

Compliance before savings

Cash flow vs tax balance

Budget 2026: Key Tax Saving Changes

No major slab changes

MAT reduced (for companies)

Focus on compliance, not incentives

Foreign asset disclosure scheme introduced

Government focus: Transparency > loopholes

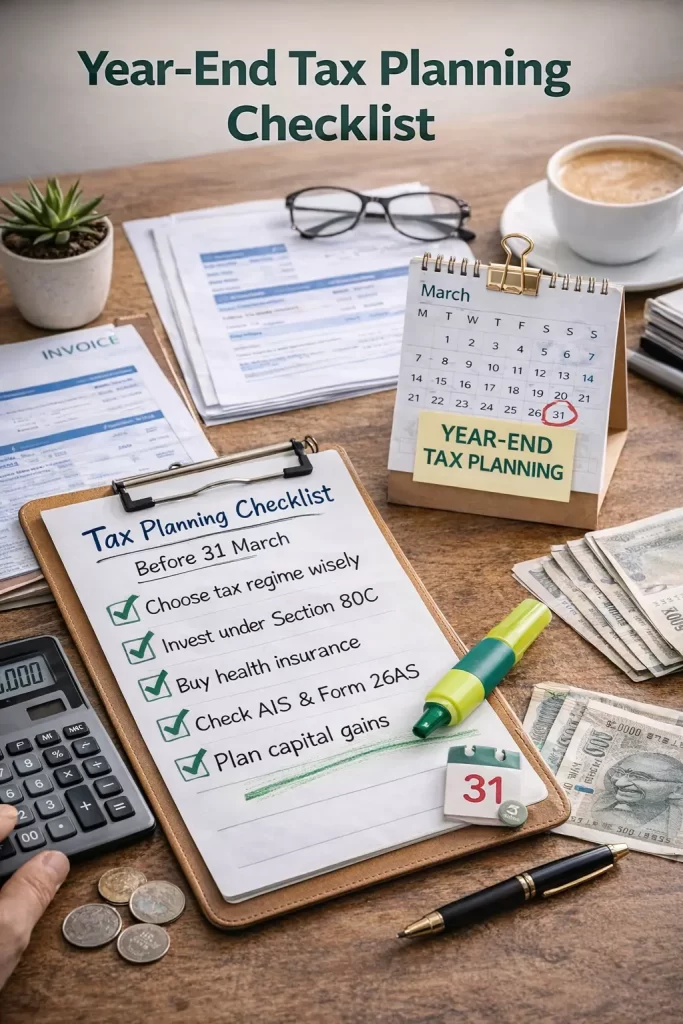

Year-End Tax Planning Checklist (Before 31 March)

Choose tax regime wisely

Invest under Section 80C

Buy health insurance

Check AIS & Form 26AS

Plan capital gains

Pay advance tax

Common Tax Saving Mistakes

Investing only to save tax

Ignoring the new tax regime

Not tracking AIS mismatches

Filing a return without planning

Missing advance tax

FAQs on Tax Saving Strategies India 2026

How can I save tax in India legally?

By using deductions (80C, 80D), choosing the right tax regime, and planning investments strategically.

Which tax regime is better in 2026?

The new regime is better for most taxpayers with fewer deductions, while the old regime benefits those with high investments.

What is the best tax saving investment?

ELSS mutual funds are considered one of the best options due to tax benefits and high return potential.

Can freelancers save tax?

Yes, through presumptive taxation, expense deductions, and proper tax planning.