A single tax mistake in AY 2026-27 can cost an Indian taxpayer anywhere from ₹10,000 to over ₹10 lakh, depending on the mistake. The Income Tax Department now cross-verifies every return against AIS, TIS and Form 26AS in real time, which means errors that once went unnoticed for years are now flagged within weeks of filing. This guide breaks down the seven costliest mistakes taxpayers make under the Income Tax Act, 2025, with the exact rupee impact of each including a Gurgaon-specific HRA error that catches even experienced salaried professionals off guard.

Why Tax Mistakes Are More Expensive in 2026 Than Ever Before

For AY 2026-27 (income earned in FY 2025-26, return due 31 July 2026), the compliance environment has changed on three fronts simultaneously. First, the Income Tax Act, 2025 replaced the 1961 Act from 1 April 2026, renumbering the penalty and procedural sections that most taxpayers and even some advisors still refer to by their old numbers. Second, AIS and TIS have matured into the Department’s primary reconciliation tools, matching every reported transaction salary, interest, dividends, mutual fund redemptions, property sale against your PAN before your return is even processed. Third, Form 26AS itself is being renamed Form 168 from Tax Year 2026-27 onwards, though it still governs your current AY 2026-27 filing. The practical effect is that the Department frequently knows about a piece of income before you file your return. Your task is no longer to avoid disclosure it is to disclose accurately, on the correct form, under the correct section, within the correct deadline. The seven mistakes below are where that accuracy most commonly breaks down, and what each one actually costs.

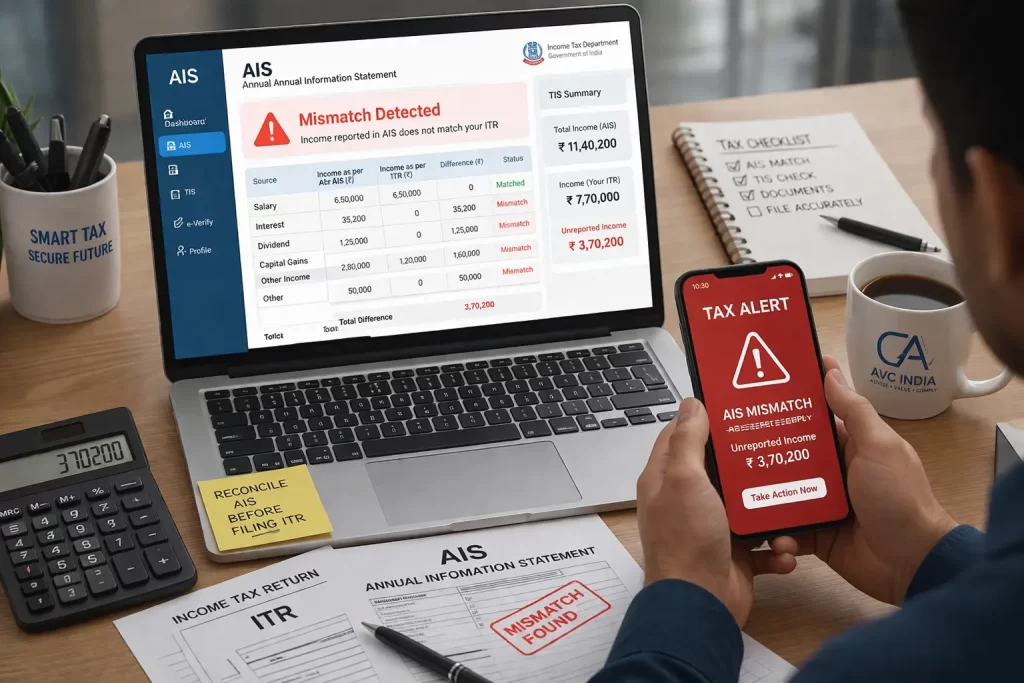

Mistake 1: Filing Without Reconciling AIS, TIS and Form 26AS

The single most common trigger for a post-filing notice is a mismatch between what a taxpayer reports and what AIS already shows. Taxpayers routinely file based on Form 16 and a bank statement, while AIS independently captures savings account interest, dividend income, mutual fund capital gains, and freelance TDS that never appears on either document. Because AIS pulls data directly from banks, registrars, and brokers, any gap between your return and AIS is visible to the Department’s automated systems before you receive any communication from them. The financial consequence is governed by Section 439 of the Income Tax Act, 2025 the renumbered version of the familiar Section 270A. Under-reporting of income attracts a penalty of 50% of the tax payable on the under-reported amount. If the under-reporting results from misrepresentation, a false entry, or an unsubstantiated deduction claim, it is reclassified as misreporting and the penalty rises to 200% of the tax due, in addition to interest under Sections 234B and 234C.

Scenario

Amount

Freelance income missing from the Income Tax Return (ITR) but reflected in AIS.

₹5,00,000

Tax payable on the omitted income (assuming the 30% tax slab).

₹1,50,000

Penalty for under-reporting of income (50% of the tax payable).

₹75,000

Penalty if the case is treated as misreporting of income (200% of the tax payable).

₹3,00,000

Total potential exposure in the worst-case scenario (excluding additional interest under applicable provisions).

Over ₹4.5 Lakh

The fix costs nothing but ten minutes: download AIS, TIS and Form 26AS from the e-filing portal before you begin filling out your return, and reconcile every entry, not just the ones your Form 16 already accounts for. Our detailed walkthrough of how these three documents differ is covered inAIS vs TIS vs Form 26AS: Key Checks Before Filing ITR.

Mistake 2: Choosing the Wrong Regime and the Gurgaon HRA Error Nobody Talks About

Most taxpayers select a tax regime based on a colleague’s advice or a generic online comparison, rather than calculating actual liability under both regimes using their own salary structure. A wrong regime choice routinely costs a salaried taxpayer ₹50,000 to ₹2 lakh a year in avoidable tax but for Gurgaon-based employees specifically, there is a second, less obvious error layered on top of this. Gurgaon is not an official metro city for HRA exemption purposes. The metro city list under the Income Tax Rules expanded from four to eight cities from FY 2026-27 covers Delhi, Mumbai, Kolkata, Chennai, Bengaluru, Hyderabad, Pune and Ahmedabad. Gurugram, despite sitting inside the National Capital Region and hosting a large share of Delhi-NCR’s salaried workforce, is officially a non-metro city, entitled to the 40% HRA exemption rate rather than 50%. In practice, many employers informally apply the 50% rate to NCR cities including Gurgaon, on the assumption that proximity to Delhi qualifies as metro treatment. This is not a settled legal position it is a grey area that varies by employer policy, and it has never been formally extended by an amendment to the Act. If your employer’s payroll system computes your HRA exemption at 50% without written confirmation of that treatment, you are carrying risk you may not know about.

Basic Salary (Annual)

Rent Paid (Annual)

HRA Received

Exemption at 40% (Correct Default)

Exemption at 50% (Commonly Assumed)

Difference Exposed to Disallowance

₹12,00,000

₹4,20,000

₹5,00,000

₹3,00,000

₹4,20,000*

Up to ₹1,20,000 of HRA exemption may be disallowed and become taxable at the applicable income tax slab rate.

Subject to the lower of the three HRA formula limbs; figures illustrate the metro-vs-non-metro gap, not a complete HRA computation.

The practical fix is not to assume either rate. Ask your employer’s payroll or HR team for written confirmation of how your HRA exemption is being classified, and if you are self-computing HRA outside of Form 16, use 40% as the default for Gurgaon unless you have documented confirmation otherwise.

Mistake 3: Misreporting Capital Gains

Capital gains are among the most heavily tracked categories in AIS, since stock exchanges, depositories, mutual fund registrars and property registrars all report transactions independently of the taxpayer. Common errors include omitting stock or mutual fund profits entirely, misclassifying short-term gains as long-term (or vice versa) by miscalculating the holding period, and failing to report crypto asset gains, which are taxed at a flat rate with no set-off against other losses. Because these transactions are reported by a third party before you file, a mismatch is detected almost immediately rather than during a later scrutiny cycle. On an unreported gain of ₹10 lakh, the combination of tax, interest under Sections 234B/234C, and a Section 439 penalty for under-reporting can push total exposure to ₹3–5 lakh depending on how the mismatch is classified. Maintain a running log of every sale date of purchase, date of sale, cost, and proceeds rather than reconstructing it at filing time, and cross-check the capital gains schedule in AIS before you finalise your Schedule CG.

Mistake 4: Ignoring Advance Tax Obligations

Any taxpayer salaried, freelance, or business owner whose estimated tax liability for the year exceeds ₹10,000 after TDS is legally required to pay advance tax in quarterly instalments. Freelancers and consultants are the most common defaulters here, because TDS deducted by clients rarely covers their full liability once professional income crosses the exemption threshold. Failure to pay attracts interest under two separate provisions: Section 234B for shortfall in advance tax paid by the financial year-end, and Section 234C for deferring instalments within the year, both charged at 1% per month (simple interest) on the shortfall. On a liability shortfall of ₹3 lakh carried for six months, this alone adds roughly ₹18,000 in interest before any penalty for the underlying under-reporting if the income itself was also underdeclared. Business owners who cross the Section 44AB tax audit threshold turnover above ₹1 crore (₹10 crore where at least 95% of receipts and payments are digital) or professional receipts above ₹50 lakh take on additional TDS deduction obligations of their own, which is covered in detail in our guide toSection 194A TDS on interest payments.

Mistake 5: Claiming Deductions Without Documentation

Sections 80C and 80D remain the most misused deduction provisions, not because taxpayers are dishonest, but because eligibility rules are narrower than commonly assumed. Claiming a life insurance premium paid for a sibling, tuition fees for a third child, or double-counting EPF contributions already reflected in Form 16 are among the most frequent errors, alongside claiming 80D premiums without a valid policy document on record. Under Section 439’s misreporting limb, a deduction claim unsupported by evidence is treated more severely than an honest omission it can attract the 200% penalty rate rather than the 50% under-reporting rate, since “claim of expenditure not substantiated by any evidence” is one of the specific grounds listed for misreporting. Keep every supporting document premium receipts, investment proofs, rent agreements on file for at least the assessment period, and cross-check each claim against the eligibility conditions before submission rather than after a query is raised.

Mistake 6: GST Non-Compliance for Business Owners and MSMEs

For Gurgaon’s dense population of startups, consultancies and small businesses, GST compliance failures are a distinct but related risk. Missed return filings, incorrect input tax credit (ITC) claims, and invoice mismatches against GSTR-2B routinely result in blocked ITC, which is a direct working-capital loss rather than just a compliance penalty. A business carrying ₹5 lakh in blocked ITC due to invoice mismatches effectively loses that amount from its cash flow until the reconciliation is resolved, on top of any late fee or interest that accrues. Reconciling GSTR-2B against your purchase register every month, rather than at year-end, is the only reliable way to catch these mismatches before they compound.

Mistake 7: Not Disclosing Foreign Assets or Income

This is the highest-stakes mistake on this list, and the one where taxpayers most often underestimate the actual exposure. Any resident (other than a not-ordinarily-resident) holding a foreign bank account, overseas investment, or signing authority over a foreign account must disclose it in Schedule FA of the ITR regardless of whether it generated any taxable income, and regardless of value, except where aggregate foreign bank balances stay below ₹5 lakh through the year. The Black Money Act, 2015 treats disclosure and taxation as two separate failures, each with its own penalty:

Provision

Trigger

Penalty

Section 43, Black Money Act

Foreign asset is held but not disclosed, or is inaccurately disclosed, in Schedule FA of the Income Tax Return.

Flat penalty of ₹10 lakh, irrespective of the asset value (subject to the ₹5 lakh foreign bank account balance exclusion).

Section 42, Black Money Act

Failure to file an Income Tax Return despite holding a reportable foreign asset.

Flat penalty of ₹10 lakh.

Section 41 read with Section 10, Black Money Act

Undisclosed foreign income or foreign assets detected during assessment or investigation.

Tax at a flat 30% (without deductions or exemptions), plus a penalty equal to three times the tax, resulting in a total liability of approximately 120% of the undisclosed amount.

On a foreign account worth ₹1 crore that goes undisclosed and is later detected, the arithmetic is stark: ₹30 lakh in tax, ₹90 lakh in penalty, for a combined liability of ₹1.2 crore against the original amount before accounting for possible prosecution under Section 51, which carries imprisonment of six months to seven years in serious cases. This is not a mistake that resolves itself with a revised return once detected; the government has opened a one-time window under the Foreign Assets of Small Taxpayers (FAST) Disclosure Scheme, 2026 for taxpayers to come forward voluntarily, which is worth exploring before the assessment stage rather than after.

What Every Mistake Actually Costs

Mistake

Governing Provision

Realistic Cost Range

AIS / TIS mismatch or unreported income

Section 439 (formerly Section 270A)

₹75,000 – ₹4.5 Lakh+

Wrong tax regime selection or incorrect Gurgaon HRA classification

Tax Regime Rules & HRA Exemption Provisions

₹50,000 – ₹2 Lakh

Capital gains misreporting

Section 439 & Schedule CG

₹3 Lakh – ₹5 Lakh

Ignoring advance tax liability

Sections 234B & 234C

₹10,000 – ₹1 Lakh+

Claiming unsupported or unsubstantiated deductions

Section 439 (Misreporting of Income)

Up to 200% of the tax relating to the disallowed claim

GST non-compliance

CGST Act & Input Tax Credit (ITC) Rules

Working capital loss, along with applicable penalty and interest

Failure to disclose foreign assets

Sections 41, 42 & 43 of the Black Money Act

Flat ₹10 Lakh penalty, with exposure up to approximately 120% of the undisclosed asset value

On a foreign account worth ₹1 crore that goes undisclosed and is later detected, the arithmetic is stark: ₹30 lakh in tax, ₹90 lakh in penalty, for a combined liability of ₹1.2 crore against the original amount before accounting for possible prosecution under Section 51, which carries imprisonment of six months to seven years in serious cases. This is not a mistake that resolves itself with a revised return once detected; the government has opened a one-time window under the Foreign Assets of Small Taxpayers (FAST) Disclosure Scheme, 2026 for taxpayers to come forward voluntarily, which is worth exploring before the assessment stage rather than after.

What Every Mistake Actually Costs

Mistake

Governing Provision

Realistic Cost Range

AIS / TIS mismatch or unreported income

Section 439 (Formerly Section 270A)

₹75,000 – ₹4.5 Lakh+

Wrong tax regime selection or Gurgaon HRA misclassification

Tax Regime Rules & HRA Exemption Provisions

₹50,000 – ₹2 Lakh

Capital gains misreporting

Section 439 & Schedule CG

₹3 Lakh – ₹5 Lakh

Ignoring advance tax liability

Sections 234B & 234C

₹10,000 – ₹1 Lakh+

Unsubstantiated deductions

Section 439 (Misreporting)

Up to 200% of the tax on the disallowed claim

GST non-compliance

CGST Act & ITC Rules

Working capital loss plus applicable penalty and interest

Undisclosed foreign assets

Sections 41, 42 & 43 of the Black Money Act

Flat ₹10 Lakh penalty, with exposure up to 120% of the undisclosed asset value

How the Department Actually Tracks Your Income in 2026

Every mistake above is detectable because the Department’s data architecture no longer depends on the taxpayer’s own disclosure as the first source of truth. AIS aggregates individual transactions from banks, brokers, mutual fund registrars and employers; TIS deduplicates that data into clean category-wise totals; and Form 26AS (soon Form 168) remains the authoritative record for TDS credit validation specifically. GST filings, PAN-linked banking transactions and high-value financial activity feed into the same profile. Our detailed comparison of how these three systems interact is available inAIS vs TIS vs Form 26AS: Key Checks Before Filing ITR, and our guide to what triggers a notice specifically for salaried employees is covered inIncome Tax Notice for Salaried Employees: Common Reasons & How to Respond.

A Practical Checklist Before You File

Reconcile AIS, TIS and Form 26AS line by line rather than relying on Form 16 alone. Confirm your HRA classification in writing if you are based in Gurgaon or elsewhere in the NCR. Calculate your liability under both tax regimes using your actual salary structure before selecting one. Pay advance tax on a realistic income estimate if your liability crosses ₹10,000 after TDS. Retain documentary proof for every deduction claimed under 80C, 80D or elsewhere. Reconcile GSTR-2B monthly if you run a business. Disclose every foreign asset in Schedule FA regardless of whether it generated income. Verify your return within 30 days of filing an unverified return is treated as not filed at all. The exact due date for most individual taxpayers filing ITR-1 and ITR-2 for AY 2026-27 remains 31 July 2026 unless extended by the CBDT, a deadline covered in more detail inIncome Tax Return Last Date of Filing (2026): Due Dates & Penalties

FAQs on Tax Mistakes in India 2026

What happens if I make a mistake in ITR?

You may receive a notice and face penalties or interest.

Can I correct tax mistakes later?

Yes, using updated return (ITR-U), but with additional tax.

How much penalty can I face?

Penalties can go up to 200% of tax in serious cases.

Why am I getting tax notices?

Mostly due to AIS mismatch or income under-reporting.