Receiving a scrutiny notice of income tax in 2026 is no longer a rare event reserved only for large corporations or high-profile taxpayers. The Income Tax Department now uses AI-powered compliance systems, AIS/TIS reconciliation engines, and real-time financial risk analysis under Project Insight to identify discrepancies automatically. For salaried professionals, startup employees, consultants, freelancers, and investors in Gurgaon and Delhi NCR, even small reporting mismatches can trigger automated notices under Section 143(2). Assessment Year 2026-27 represents a critical transition period in India’s tax administration ecosystem. While procedural systems now operate under the Income Tax Act 2025 framework, the actual assessments for FY 2025-26 continue to remain largely governed by the Income Tax Act, 1961. This dual regulatory environment has created confusion among taxpayers, especially regarding scrutiny notices, faceless assessments, AIS mismatches, and reporting obligations. This guide explains how scrutiny notices work in 2026, why taxpayers in Gurgaon and Delhi NCR are receiving more notices, how AI-based tax scrutiny operates, and what steps should be taken immediately after receiving a scrutiny notice of income tax.

Understanding Scrutiny Notice of Income Tax Under Section 143(2)

A scrutiny notice of income tax under Section 143(2) is issued when the Income Tax Department is not fully satisfied with the income declared in a taxpayer’s return. Unlike a defective return notice under Section 139(9), which usually relates to technical or filing errors, a Section 143(2) notice signals that the department wants to verify the correctness of income, deductions, exemptions, or financial disclosures. For AY 2026-27, scrutiny notices are mostly generated through automated risk assessment systems instead of manual officer selection. These systems compare taxpayer returns with AIS, TIS, Form 26AS, GST data, banking records, stock market activity, property registrations, and international remittance data. If discrepancies appear significant, the system flags the return and initiates scrutiny proceedings.

The Legal Timeline for Scrutiny Notice of Income Tax in 2026

For AY 2026-27, the law provides a strict statutory timeline for issuing scrutiny notices. The department must issue the Section 143(2) notice within three months from the end of the financial year in which the return was filed. For example, if a taxpayer files an income tax return in July 2026, the department generally gets time until June 30, 2027, to issue the scrutiny notice. Notices issued beyond this timeline may become legally challengeable. Taxpayers in Delhi NCR often ignore notice timelines and assume all portal communications are valid. However, carefully checking the notice date, DIN number, and portal authenticity is extremely important.

Limited Scrutiny vs Complete Scrutiny in Income Tax

The scrutiny notice of income tax process generally falls into two categories: Limited Scrutiny and Complete Scrutiny.

Type of Scrutiny

Purpose

Risk Level

Limited Scrutiny

Verification of a specific issue like AIS mismatch or property transaction

Moderate

Complete Scrutiny

Full financial examination of income, deductions, assets, and disclosures

High

In limited scrutiny, the Assessing Officer can generally investigate only the specified issue unless higher authorities approve expansion of scope. Complete scrutiny, however, allows detailed review of the taxpayer’s entire financial structure.

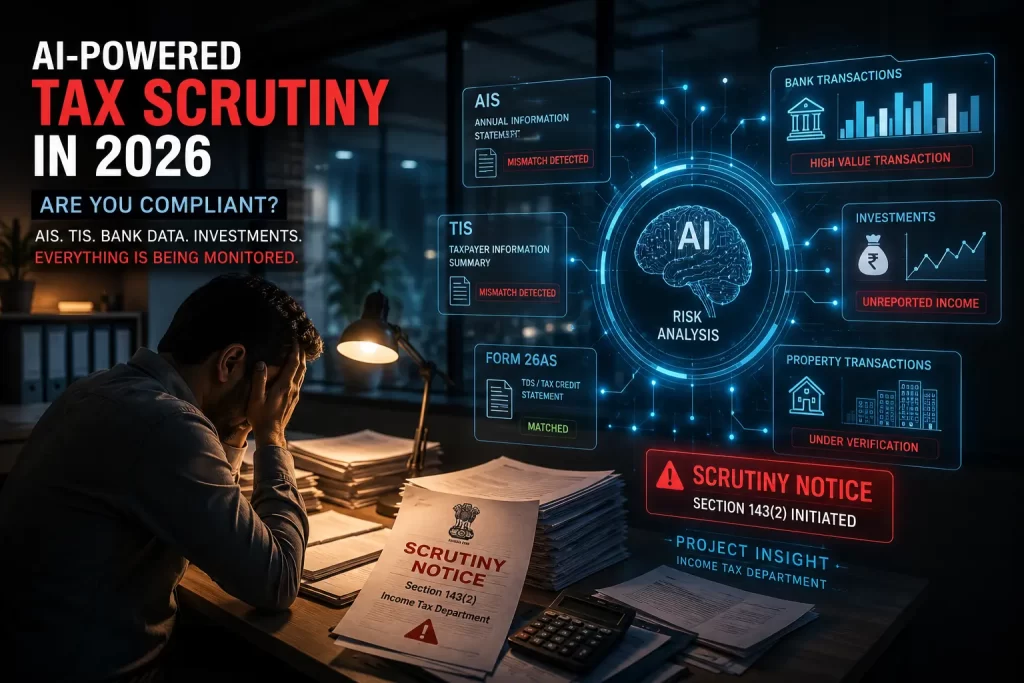

How AI-Based Scrutiny Works Under Project Insight

The Income Tax Department’s Project Insight platform has transformed compliance enforcement in India. Every PAN holder now has a digital financial profile created through integrated databases. The system automatically compares:

AIS and TIS entries, GST turnover,stock broker data,property transactions,and foreign remittance activity. If a taxpayer’s declared income appears inconsistent with lifestyle indicators or financial transactions, the AI engine assigns a higher compliance risk score. For example, if a Gurgaon-based salaried employee reports income of ₹14 lakh but the AIS reflects high-value crypto transactions, luxury property investments, or international travel spending beyond expected limits, the return may automatically move into the scrutiny pipeline.

Top Reasons Why Taxpayers Receive Scrutiny Notice of Income Tax in 2026

AIS & TIS Mismatch

AIS mismatch remains one of the biggest reasons behind scrutiny notices in AY 2026-27. Many taxpayers still rely solely on Form 16 and fail to reconcile bank interest, dividend income, capital gains, or crypto transactions appearing in AIS. The department’s AI systems now treat AIS as the primary compliance data source. Altering pre-filled values without filing AIS feedback can trigger automated scrutiny alerts instantly.

High-Value Property Transactions in Delhi NCR

Real estate scrutiny has intensified significantly in Delhi NCR. Under Section 50C, if a property is sold below circle rate valuation, the department may treat the circle rate as deemed consideration for capital gains purposes. High-value transactions in South Delhi, Gurgaon, and Noida are now cross-verified with:property registrar databases,banking records,and housing loan information. This has increased scrutiny related to capital gains exemptions and reinvestment claims under Sections 54 and 54F.

ESOP & RSU Reporting Errors in Gurgaon Startups

Startup professionals in Gurgaon frequently receive scrutiny notices because of incorrect ESOP or RSU reporting. Employees often fail to declare perquisite taxation correctly when stock options are exercised. Since employers report ESOP taxation through salary TDS filings, the department can easily identify mismatches between salary disclosures and filed returns. Foreign stock holdings and US-based RSUs must also be properly disclosed under Schedule FA. Failure to report these assets can lead to severe scrutiny consequences.

Wrong Presumptive Taxation Claims by Freelancers

Freelancers and consultants in Delhi NCR often misuse presumptive taxation provisions under Section 44AD instead of Section 44ADA. The department now automatically checks whether:TDS was deducted under Section 194J,GST filings indicate professional activity,and the taxpayer selected the correct presumptive taxation scheme. This mismatch has become a major scrutiny trigger for consultants, tech professionals, and digital freelancers.

Crypto & Foreign Asset Non-Disclosure

Crypto scrutiny has become far stricter in 2026 because exchanges now report PAN-linked transactions directly to authorities. Non-reporting of VDA transactions under Schedule VDA is treated as high-risk behavior. Similarly, Gurgaon professionals working for multinational companies often fail to disclose:

foreign brokerage accounts,overseas shares,RSUs,or foreign bank accounts. These omissions can trigger scrutiny under both income tax law and the Black Money Act.

Faceless Assessment & E-Proceedings in 2026

The scrutiny process is now almost entirely faceless. Taxpayers no longer physically visit tax offices because all proceedings occur digitally through the e-filing portal. After receiving a scrutiny notice of income tax, taxpayers must upload:supporting documents,explanations,bank statements,capital gains reports,and reconciliations through the e-Proceedings section. The department has also integrated the AI-based “Kar Saathi” chatbot to guide taxpayers through notice responses and procedural queries.

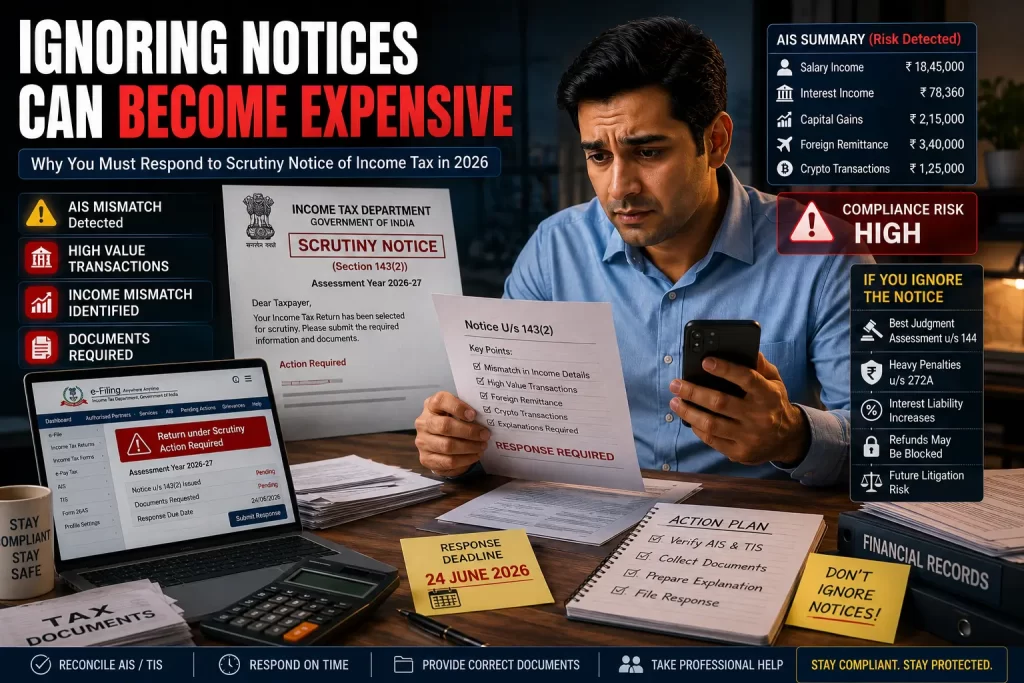

What Happens If You Ignore a Scrutiny Notice of Income Tax

Ignoring a scrutiny notice can create severe financial and legal consequences. If the taxpayer fails to respond within the prescribed timeline, the department may proceed with a Best Judgment Assessment under Section 144. In such cases, taxable income may be calculated entirely based on AIS, SFT, and external data records, often resulting in inflated tax demands. Non-compliance may also lead to: penalties under Section 272A, refund holds,interest liability,and future litigation complications. For high-income taxpayers in Gurgaon and Delhi NCR, ignoring scrutiny notices can create long-term compliance risks.

Step-by-Step Process to Respond to a Scrutiny Notice

The first step after receiving a scrutiny notice of income tax is verifying the authenticity of the notice directly on the Income Tax portal. Taxpayers should confirm the DIN number, notice section, and response deadline carefully. Next, all financial records should be reconciled against:

AIS,Form 26AS,bank statements,GST data,and investment records. Responses should be professionally drafted with supporting evidence and proper explanations. In complex cases involving ESOPs, foreign assets, crypto income, or capital gains, professional CA assistance becomes highly recommended.

Why Gurgaon & Delhi NCR Taxpayers Face Higher Scrutiny Risk

Delhi NCR remains one of India’s highest-risk regions for tax scrutiny because of its concentration of: startup founders,multinational employees,high-income professionals,property investors,and stock market traders. Gurgaon especially has a large number of ESOP holders, remote international workers, consultants, and startup employees with complex tax structures. This makes the region highly visible to AI-based compliance systems. The department’s predictive analytics now actively monitors high-value taxpayers whose spending patterns, investments, or financial activities appear inconsistent with declared income.

Professional Assistance for Scrutiny Notice of Income Tax

Modern scrutiny proceedings involve much more than simply replying to notices. Taxpayers now need:

AIS reconciliation, capital gains computation, legal response drafting, faceless assessment management, and detailed documentation support. Professional tax advisors help reduce litigation risks, improve response quality, and ensure procedural compliance during scrutiny assessments. For Gurgaon professionals dealing with ESOPs, foreign assets, startup compensation, or property investments, expert assistance can significantly reduce scrutiny exposure.

Frequently Asked Questions (FAQs)

What is scrutiny notice of income tax under Section 143(2)?

A scrutiny notice under Section 143(2) is issued when the Income Tax Department wants to verify the correctness of income, deductions, or disclosures reported in the return.

Can AIS mismatch trigger scrutiny notice?

Yes. AIS mismatch is one of the biggest triggers for automated scrutiny notices in AY 2026-27.

What happens if I ignore scrutiny notice of income tax?

Ignoring scrutiny notices may lead to Best Judgment Assessment under Section 144, penalties, refund holds, and litigation risks.

Is crypto income monitored by the Income Tax Department?

Yes. Crypto exchanges now report PAN-linked VDA transactions directly to authorities, making non-disclosure highly risky.

How long does scrutiny assessment take?

The timeline depends on the complexity of the case, but faceless scrutiny proceedings generally continue until final assessment completion under Section 143(3).

Conclusion

The scrutiny notice of income tax process in 2026 has become highly data-driven and technology-focused. AI-powered systems under Project Insight now analyze taxpayer behavior, financial transactions, and reporting patterns automatically, making even small mismatches capable of triggering scrutiny. For taxpayers in Gurgaon and Delhi NCR, the most common scrutiny triggers involve AIS mismatches, ESOP taxation errors, foreign asset disclosure failures, crypto non-reporting, presumptive taxation misuse, and high-value property transactions. Understanding how scrutiny notices work, responding within legal timelines, and maintaining accurate documentation are now essential parts of modern tax compliance. In an era of faceless assessments and AI-based scrutiny, proactive reconciliation and professional advisory support are more important than ever before.