For many salaried employees, receiving an Income Tax Notice for Salaried Employees can be stressful. Most taxpayers immediately assume they have done something wrong or that they may face penalties from the Income Tax Department. However, not every notice means serious trouble. In many cases, notices are generated because of small mismatches, incomplete disclosures, or automated verification systems used by the department. Over the last few years, the Income Tax Department has significantly upgraded its data analytics and AI-based scrutiny systems. Information from AIS, TIS, banks, mutual funds, employers, and financial institutions is now cross verified automatically. As a result, even salaried taxpayers with simple income structures are increasingly receiving income tax notices for mismatches, incorrect reporting, or missing disclosures. Understanding why an Income Tax Notice for Salaried Employees is issued and how to respond correctly has become extremely important for salaried employees in India. This guide will help you understand common reasons, AIS mismatch issues, and the right steps to handle notices safely.

What Is an Income Tax Notice?

An income tax notice is an official communication sent by the Income Tax Department to a taxpayer regarding discrepancies, verification requirements, compliance issues, or additional information related to the Income Tax Return (ITR). For salaried employees, notices are commonly issued because of mismatch in salary income, incorrect deduction claims, TDS discrepancies, high-value transactions, or incomplete ITR filing. In most situations, these notices are generated automatically through the department’s compliance monitoring systems.

Why Salaried Employees Receive Income Tax Notices

Many salaried taxpayers believe that proper TDS deduction by employers completely eliminates the possibility of receiving tax notices. However, this assumption is no longer correct. Modern compliance systems compare information from multiple sources simultaneously. Even small inconsistencies can trigger automated notices. In many cases, mismatches between Form 16, AIS, Form 26AS, and filed ITR data become the primary reason behind these notices. Salaried employees who change jobs during the financial year, claim deductions incorrectly, fail to disclose interest income, or engage in high-value financial transactions are more likely to receive scrutiny communications from the department.

Most Common Income Tax Notices for Salaried Employees

Salaried employees can receive different types of notices depending on the nature of the issue identified by the Income Tax Department.

Notice TypePurpose

Section 143(1)Intimation after return processing

Section 139(9)Defective return notice

Section 148Income escaping assessment

AIS/TIS Mismatch NoticeData mismatch verification

Scrutiny NoticeDetailed examination of return

TDS Mismatch NoticeDifference in TDS reporting

Many taxpayers panic after seeing these section numbers without understanding what they actually mean. In reality, several notices are informational or procedural and can be resolved easily if addressed properly within the prescribed timeline.

Notice Under Section 143(1)

Section 143(1) is one of the most common notices received by salaried employees. In many situations, it is simply an intimation after processing the ITR. This notice may contain refund information, confirmation of return processing, tax demand, or adjustment details arising due to mismatches in deductions or reported income. For example, if deductions claimed in the ITR are not properly reflected in AIS or Form 16, the department may automatically recompute taxable income and issue an adjustment notice. Although this notice is generally not serious, taxpayers should still review it carefully to ensure there are no incorrect adjustments.

Defective Return Notice Under Section 139(9)

A notice under Section 139(9) is one of the most common types of Income Tax Notice for Salaried Employees and is issued when the Income Tax Department considers the filed return defective or incomplete. This usually happens because of incorrect salary disclosures, selection of the wrong ITR form, missing information, or inaccurate deduction reporting. The department normally provides a limited time window to correct the defective return. If the taxpayer fails to respond within the deadline, the return may be treated as invalid. For salaried employees, this can create complications in refund processing, future compliance records, and even increase the risk of further income tax notices for mismatches.

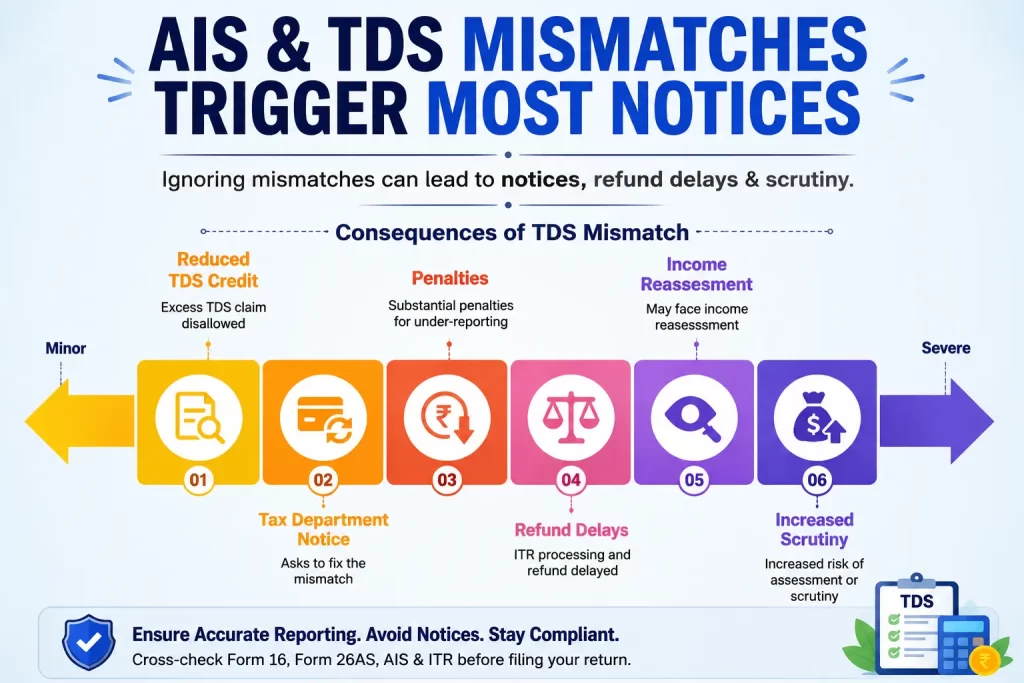

AIS and TDS Mismatch Notices

One of the biggest reasons behind the recent rise in Income Tax Notice for Salaried Employees is the implementation of AIS and TIS systems. The Annual Information Statement now captures salary income, bank interest, dividends, stock transactions, mutual fund investments, foreign remittances, and various high-value transactions. If the information reported in the ITR does not match these records, automated income tax notices for mismatches may be generated. Similarly, TDS mismatch notices arise when Form 16 information differs from Form 26AS or when tax credits are claimed incorrectly. Even minor reporting inconsistencies can now trigger verification notices because the Income Tax Department’s systems have become far more data-driven and AI-powered than before.

High-Value Transactions That Trigger Notices

Many salaried employees are unaware that large financial transactions are continuously monitored and reported to the Income Tax Department. Transactions such as large cash deposits, expensive foreign travel, heavy credit card spending, substantial stock market investments, property purchases, and mutual fund investments are commonly tracked through financial reporting systems. If these activities appear inconsistent with declared salary income, the department may issue notices seeking clarification. This is particularly common among salaried employees who maintain multiple bank accounts or actively participate in investment activities without proper income disclosure.

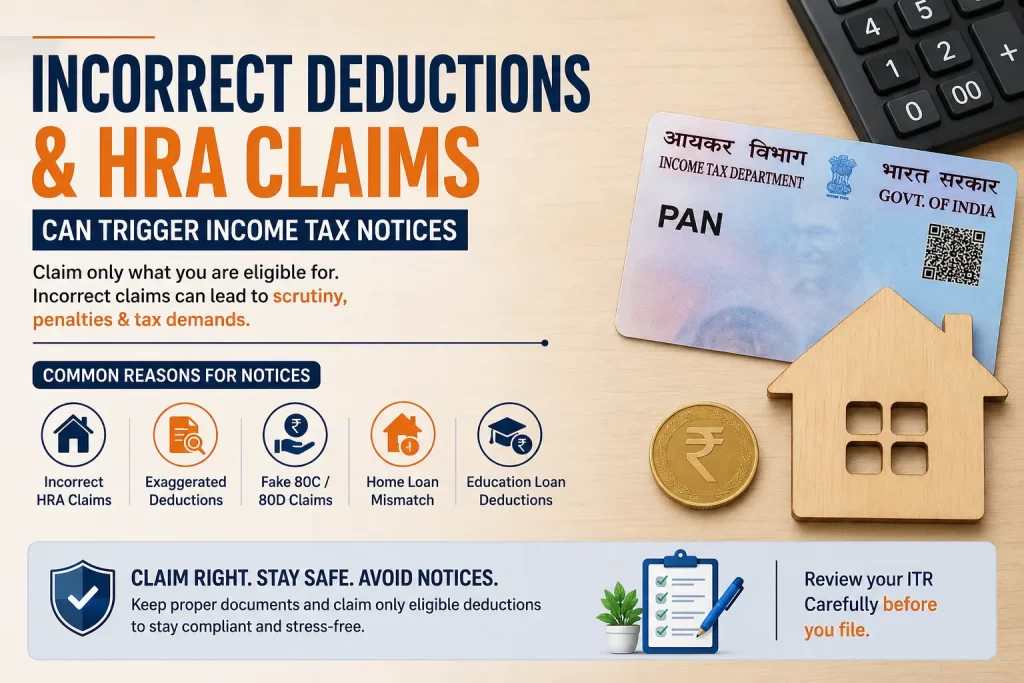

Incorrect Deduction Claims and Fake Exemptions

Another major trigger for Income Tax Notice for Salaried Employees is incorrect deduction reporting. Many taxpayers claim deductions without proper documentation, especially under:

Section 80C

Section 80D

HRA exemption

Home loan benefits

Education loan deductions

The Income Tax Department’s AI-driven analytics systems can now identify inconsistencies far more efficiently than before. For example, salaried employees claiming HRA exemption while also showing property ownership in the same city may attract verification scrutiny. Similarly, exaggerated deductions unsupported by actual investments, insurance payments, or eligible expenses can trigger income tax notices for mismatches and further compliance checks.

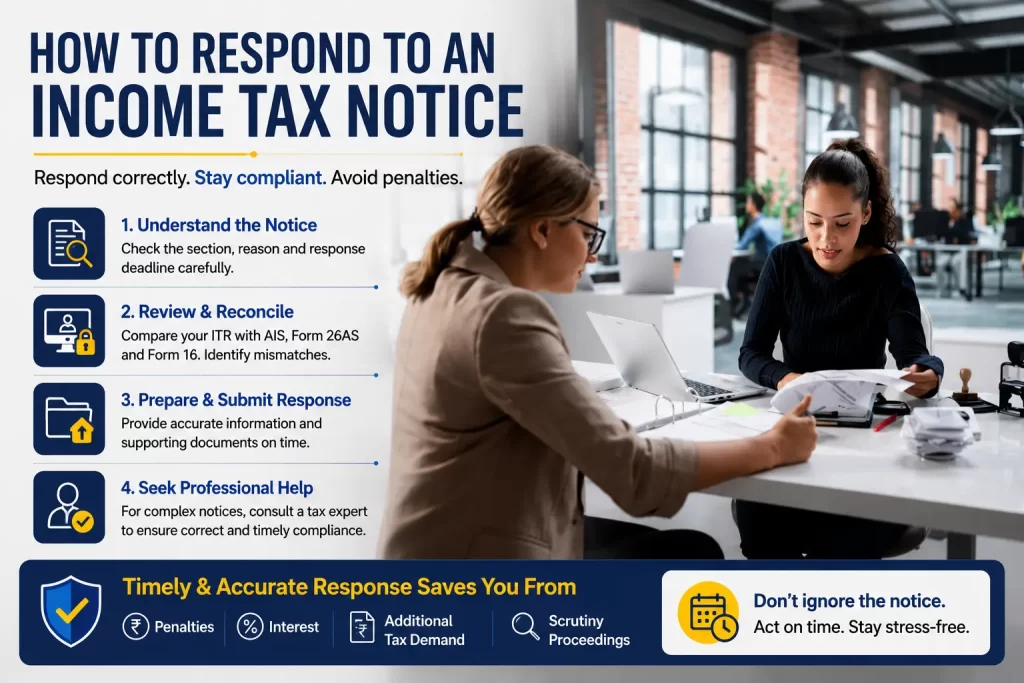

How to Respond to an Income Tax Notice

The most important thing salaried employees should understand is that income tax notices should never be ignored. The first step is to carefully identify the section under which the notice was issued, understand the reason mentioned in the communication, and verify the response deadline. Taxpayers should then log in to the income tax e-filing portal and compare their filed return with AIS, Form 26AS, and Form 16 records. In many cases, notices can be resolved simply by correcting mismatches or uploading supporting documents online. However, notices involving scrutiny assessments, reassessment proceedings, or complex financial disclosures should ideally be handled with professional tax assistance. Responding calmly and accurately is extremely important because unnecessary panic often leads to incorrect replies and additional complications.

What Happens If You Ignore an Income Tax Notice?

Ignoring notices can create much bigger compliance problems later. Depending on the type of notice issued, consequences may include penalties, additional tax demands, loss of refunds, interest liabilities, reassessment proceedings, or even prosecution in serious cases. The Income Tax Department now maintains detailed digital compliance histories, which means repeated non-compliance may increase the likelihood of future scrutiny as well. This is why even small notices should be reviewed and addressed properly within the specified deadline.

How Salaried Employees Can Avoid Income Tax Notices

Completely avoiding notices may not always be possible because many communications are system-generated. However, salaried employees can significantly reduce the chances of receiving notices by maintaining accurate reporting and proper documentation. Taxpayers should carefully reconcile AIS, Form 26AS, and Form 16 data before filing returns. They should also disclose all interest income, report investment transactions correctly, avoid fake deduction claims, and select the proper ITR form. Employees with multiple income sources, stock market activities, or freelance side income should be especially cautious while filing returns because mismatches are more common in such situations. Accurate disclosure and timely compliance remain the best ways to avoid unnecessary scrutiny.

Frequently Asked Questions (FAQs)

Is receiving an income tax notice serious?

Not always. Many notices are routine communications or mismatch intimations generated automatically by the Income Tax Department. However, they should never be ignored.

Can salaried employees get scrutiny notices?

Yes. Salaried employees can receive scrutiny notices if the department identifies income mismatches, incorrect deductions, or suspicious financial transactions.

What is the most common income tax notice for salaried employees?

Section 143(1) intimation notices and AIS mismatch notices are among the most common notices received by salaried taxpayers.

Can incorrect HRA claims trigger tax notices?

Yes. Incorrect or unsupported HRA exemption claims can trigger verification notices, especially if property ownership data creates inconsistencies.

How can I check if I have received an income tax notice?

Taxpayers can log in to the Income Tax e-filing portal and check the “Pending Actions” or “e-Proceedings” section.

Final Thoughts

The increase in income tax notices for salaried employees is largely driven by the government’s expanding data verification systems and AI-based compliance monitoring. In most cases, these notices are not signs of fraud investigations or criminal proceedings. They are often generated because of reporting mismatches, incomplete disclosures, AIS mismatch notice triggers, or automated verification systems. The key is to remain calm, understand the issue correctly, and respond within the deadline using accurate supporting information. Notices such as TDS mismatch notice, notice under section 139(9), notice under section 143(1), and even income tax notice after ITR filing are becoming increasingly common as the department strengthens digital scrutiny mechanisms. As compliance systems continue becoming more advanced under the new tax framework, salaried employees must become more proactive about proper ITR filing, AIS reconciliation, deduction documentation, and financial disclosure accuracy. Timely compliance today can help avoid high-value transaction notice risks and prevent major tax complications in the future.

Need Help Responding to an Income Tax Notice?

If you have received an income tax notice and are unsure how to respond, AVC’s tax professionals can help you review the notice, identify the issue, prepare accurate responses, and handle compliance professionally before deadlines expire.