The Income Tax Act, 1961 is no longer the primary law governing income tax in India. It has been replaced by the Income Tax Act, 2025, which came into force on April 1, 2026.

The 1961 Act still matters for one reason: it governs assessment of income earned in FY 2025-26 (Assessment Year 2026-27), since that income was earned before the new law took effect. Every return filed for FY 2025-26 and earlier will still rely on 1961 Act provisions, sections, and case law. From FY 2026-27 onward, the 2025 Act applies. For Gurgaon-based individuals and businesses currently filing returns or planning FY 2026-27 finances, both laws matter one for the year just closed, one for the year ahead.

Why This Question Is Confusing Right Now

If you’ve searched “Income Tax Act 1961” recently, you’ve probably also seen “Income Tax Act 2025” everywhere in news, in tax software updates, and in what your CA is telling you. That’s because India is in the middle of a tax-law transition, and most online content hasn’t caught up. Search results are split between old explainers of the 1961 Act, dense clause-comparison tables aimed at tax professionals, and government press notes that explain the why but not the what does this mean for me.This guide is written for that gap for salaried individuals, small business owners, and companies in Gurgaon who need a practical, current answer, not a law-school breakdown.

Income Tax Act 1961: The Law You've Known for 65 Years

The Income Tax Act, 1961 has been India’s primary direct tax statute since it replaced the Income Tax Act, 1922. Administered by the Central Board of Direct Taxes (CBDT) under the Ministry of Finance, it laid out:

How total income is computed under five heads (salary, house property, business/profession, capital gains, other sources)

Tax slabs, rates, and rebates

Deductions and exemptions (Sections 80C to 80U)

TDS and TCS provisions

Assessment, appeals, and penalty procedures

Provisions for firms, companies, trusts, and non-residents

Over six decades, the Act grew to more than 800 sections (with sub-sections, provisos, and explanations pushing the effective count well beyond that), amended almost every year through the Finance Act. That complexity dense cross-referencing, repealed-but-not-removed sections, and layered amendments is the main reason the government moved to replace it rather than amend it further.

Income Tax Act 2025: What Actually Changed

The Income Tax Act, 2025 was passed to simplify structure and language, not to overhaul tax policy overnight. Based on the government’s own stated objectives (per the Ministry of Finance’s official backgrounder), the key changes are:

Aspect

Income Tax Act, 1961

Income Tax Act, 2025

Number of Sections

800+ sections, including numerous sub-sections, explanations, provisos, and amendments.

Approximately 536 sections, reorganized and simplified for easier interpretation.

Terminology

Uses the concepts of Previous Year and Assessment Year.

Introduces a single concept called Tax Year, replacing both earlier terms.

Language Style

Complex legal drafting with frequent cross-references and multiple amendments.

Simplified drafting with clearer wording and greater use of structured tables and schedules.

Effective Date

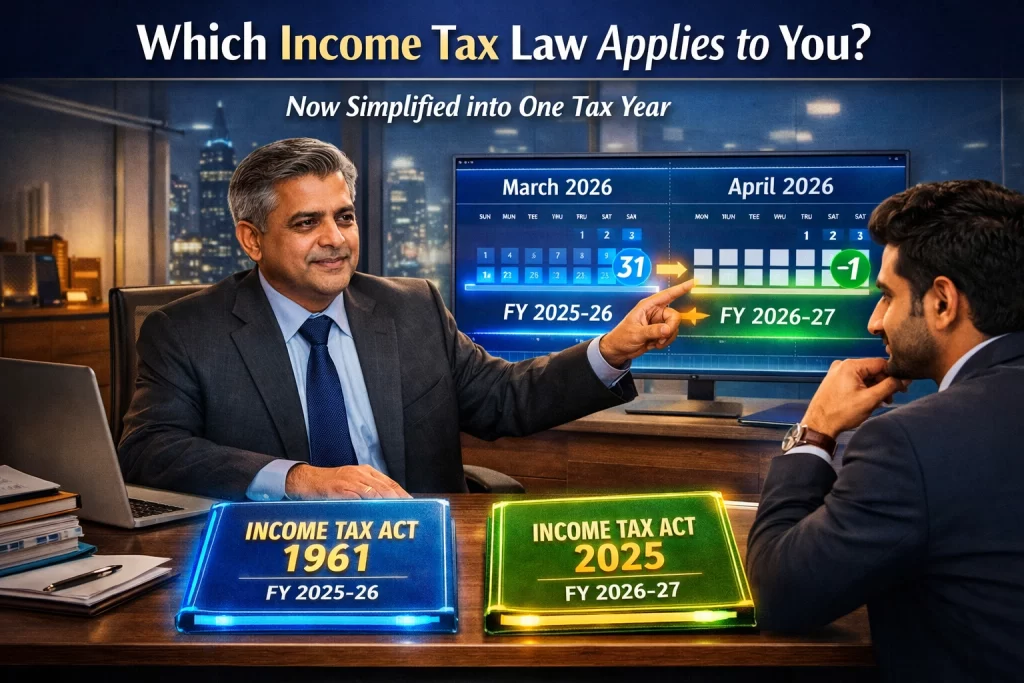

Applicable from 1962 up to 31 March 2026 for income relating to FY 2025–26 and earlier.

Effective from 1 April 2026 for FY 2026–27 (Tax Year 2026–27) onwards.

Core Tax Policy

Tax provisions are amended annually through the Finance Act while retaining the 1961 legislation.

Most tax policies continue from the earlier law, with future amendments also introduced through the annual Finance Act.

Structure

Chapters and sections evolved over decades, resulting in scattered provisions and numerous insertions.

Reorganized into consolidated chapters with schedules replacing several dispersed provisions for improved readability.

The most user-facing change is the “Tax Year” concept it replaces the old, frequently confused Previous Year / Assessment Year distinction with a single 12-month period aligned to when the income is earned. This alone resolves one of the most common questions Gurgaon taxpayers ask their CA every filing season.

Importantly, the 2025 Act is a restructuring, not a rewrite of tax policy. Most deduction sections, TDS logic, and computation principles that Gurgaon businesses and individuals rely on continue in substance just renumbered and reworded for clarity.

Is the Income Tax Act 1961 Still Applicable?

Yes for a specific, time-bound purpose. Any income earned during FY 2025-26 (April 2025 to March 2026) is assessed under the Income Tax Act, 1961, because that’s the law that was in force when the income was earned. This means:

ITR filing for AY 2026-27 (covering FY 2025-26 income) continues to reference 1961 Act sections

Pending assessments, appeals, and litigation for earlier years remain governed by 1961 Act provisions and established case law

Any scrutiny, notice, or reassessment relating to FY 2025-26 or earlier will cite the old Act

From FY 2026-27 (Tax Year 2026-27) onward, the Income Tax Act, 2025 governs all computation, filing, and assessment. In practice, this means Gurgaon taxpayers and firms are currently operating under both laws simultaneously for a transition period closing out 1961 Act compliance for the last old-regime year while planning FY 2026-27 finances under the new Act.

What This Means for Gurgaon Taxpayers and Businesses Right Now

Gurgaon’s tax base a mix of salaried professionals in corporate hubs like Cyber City and Golf Course Road, SMEs, and a large number of consultants and freelancers faces a few practical decisions during this transition:

Filing for FY 2025-26 (AY 2026-27): This return still follows 1961 Act rules. Don’t apply “Tax Year” terminology or 2025 Act section numbers when preparing this filing it will cause mismatches with the ITR utility and your CA’s working papers.

Advance tax and TDS planning for FY 2026-27: This is where the 2025 Act applies. If your business restructured compliance workflows, payroll TDS mapping, or vendor TDS categorization based on old section numbers, those references need updating for the current Tax Year.

Ongoing assessments or notices: If you have a pending income tax notice, scrutiny case, or appeal relating to any year up to FY 2025-26, the applicable law is still the 1961 Act the transition does not retroactively change how those cases are decided.

Businesses restructuring compliance calendars: With GST cycles, FLA Return deadlines, and now a renumbered Income Tax Act running concurrently, Gurgaon businesses are seeing more compliance-calendar confusion than usual this year. This is the single most common reason clients are reaching out to CA firms for a compliance health-check right now.

This dual-law period is temporary, but it’s exactly the kind of transition where filing errors, missed deadlines, and section-number confusion are most likely which is why professional review matters more this cycle than in a typical year.

Sections of the 1961 Act You'll Still Hear About

Even as the numbering changes under the 2025 Act, certain 1961 Act sections remain reference points because of accumulated case law, professional habit, and ongoing FY 2025-26 filings:

Section 80C deductions for investments (PPF, ELSS, life insurance, etc.)

Section 54 / 54F capital gains exemption on reinvestment in property

Section 44AB tax audit applicability thresholds

Section 143(1)/143(3) intimation and scrutiny assessment

Section 194 series TDS provisions across various payments

If you’re researching “notes” or looking for a structured breakdown of these sections for study or reference purposes, treat them as historically important and currently applicable only to FY 2025-26 and earlier filings not as a live reference for FY 2026-27 planning.

A Quick Note on Related Questions

Can gifts to a spouse be taxed? Gifts between spouses are generally exempt from tax in the hands of the recipient under both the outgoing and incoming law, but clubbing provisions apply income earned from the gifted asset (e.g., interest, rent) is typically clubbed back into the giver’s income for tax purposes. This is a common area where Gurgaon taxpayers assume “gift = tax-free” without accounting for clubbing rules, and it’s worth a specific consultation rather than a general answer, since treatment varies by asset type and amount.

Frequently Asked Questions

What is the Income Tax Act, 1961?

It is the law that governed direct taxation in India from 1962 until March 31, 2026, covering how income is computed, taxed, and assessed across five income heads.

Is the Income Tax Act, 1961 still applicable?

Yes, for income earned up to FY 2025-26 (Assessment Year 2026-27) and for any pending assessments or appeals relating to that period or earlier. From FY 2026-27 onward, the Income Tax Act, 2025 applies.

What is the Tax Act 1961?

“Tax Act 1961” commonly refers to the Income Tax Act, 1961 India’s principal direct tax legislation prior to its replacement by the Income Tax Act, 2025.

Can I gift ₹1 crore to my wife without tax implications?

The gift itself is typically exempt from tax for the recipient, but any income generated from that gifted amount is usually clubbed with the giver’s income under clubbing provisions. Treatment can vary based on how the funds are used, so it’s worth confirming with a tax advisor before making a large inter-spouse transfer.

What's the main difference between the Income Tax Act 1961 and 2025?

The 2025 Act restructures and simplifies the law fewer, more logically organized sections, simplified language, and a single “Tax Year” concept replacing the old Previous Year/Assessment Year system. Core tax policy (rates, major deductions) is largely carried forward rather than overhauled.

Need Help Navigating the Transition?

Whether you’re finalizing your FY 2025-26 return under the 1961 Act or restructuring your compliance calendar for the 2025 Act, getting the section references and filing timelines right matters more during a transition year than any other. Book a consultation with AVC’s Gurgaon tax advisory team to review your filing status, TDS mapping, and FY 2026-27 planning under the new law.