Income tax return last date of filing is one of the most important deadlines every taxpayer in India should be aware of. Whether you are a salaried employee, freelancer, business owner, or investor, understanding the income tax return filing due date is essential to avoid penalties, interest charges, and unnecessary compliance issues. Every year, the Income Tax Department prescribes specific deadlines for filing returns based on the taxpayer category. Missing the income tax return deadline can result in late filing fees, delays in refunds, loss of certain tax benefits, and even increased scrutiny in some situations. For Assessment Year (AY) 2026–27, taxpayers should be aware of the latest income tax return due date 2026, belated return provisions, revised return rules, and penalties applicable under the Income Tax Act. With the introduction of advanced compliance tools such as AIS (Annual Information Statement), TIS (Taxpayer Information Summary), and AI-based verification systems, timely and accurate filing has become more important than ever before. Taxpayers should also understand the consequences of ITR filing penalty provisions, including the section 234F penalty that may apply in cases of delayed filing. This guide explains the income tax return filing date, the income tax return last date of filing, ITR filing due date 2026 requirements, penalties for late filing, and the latest rules every taxpayer should know to remain compliant.

What Is the Income Tax Return Filing Due Date?

The income tax return filing due date is the last date prescribed by the Income Tax Department for submitting your Income Tax Return for a particular financial year. Filing your return before this deadline ensures compliance with tax laws and allows taxpayers to claim refunds, carry forward losses, and avoid penalties. The due date varies depending on the category of taxpayer. Salaried individuals generally have different filing deadlines compared to businesses that require tax audits or transfer pricing compliance. The primary purpose of prescribing filing deadlines is to ensure timely tax reporting and allow the government to process returns, verify information, and manage tax administration efficiently.

Why Filing ITR Before the Due Date Matters

Many taxpayers believe that filing an ITR is necessary only when taxes are payable. However, timely filing offers several important benefits beyond basic compliance. A return filed before the deadline helps taxpayers receive refunds faster because the Income Tax Department processes compliant returns more efficiently. It also preserves the right to carry forward eligible business losses and capital losses to future years. Financial institutions frequently request ITR acknowledgments when evaluating loan applications, credit facilities, and visa requests. A history of timely filing therefore contributes to stronger financial credibility. Most importantly, filing before the deadline helps taxpayers avoid penalties, interest liabilities, and unnecessary compliance complications.

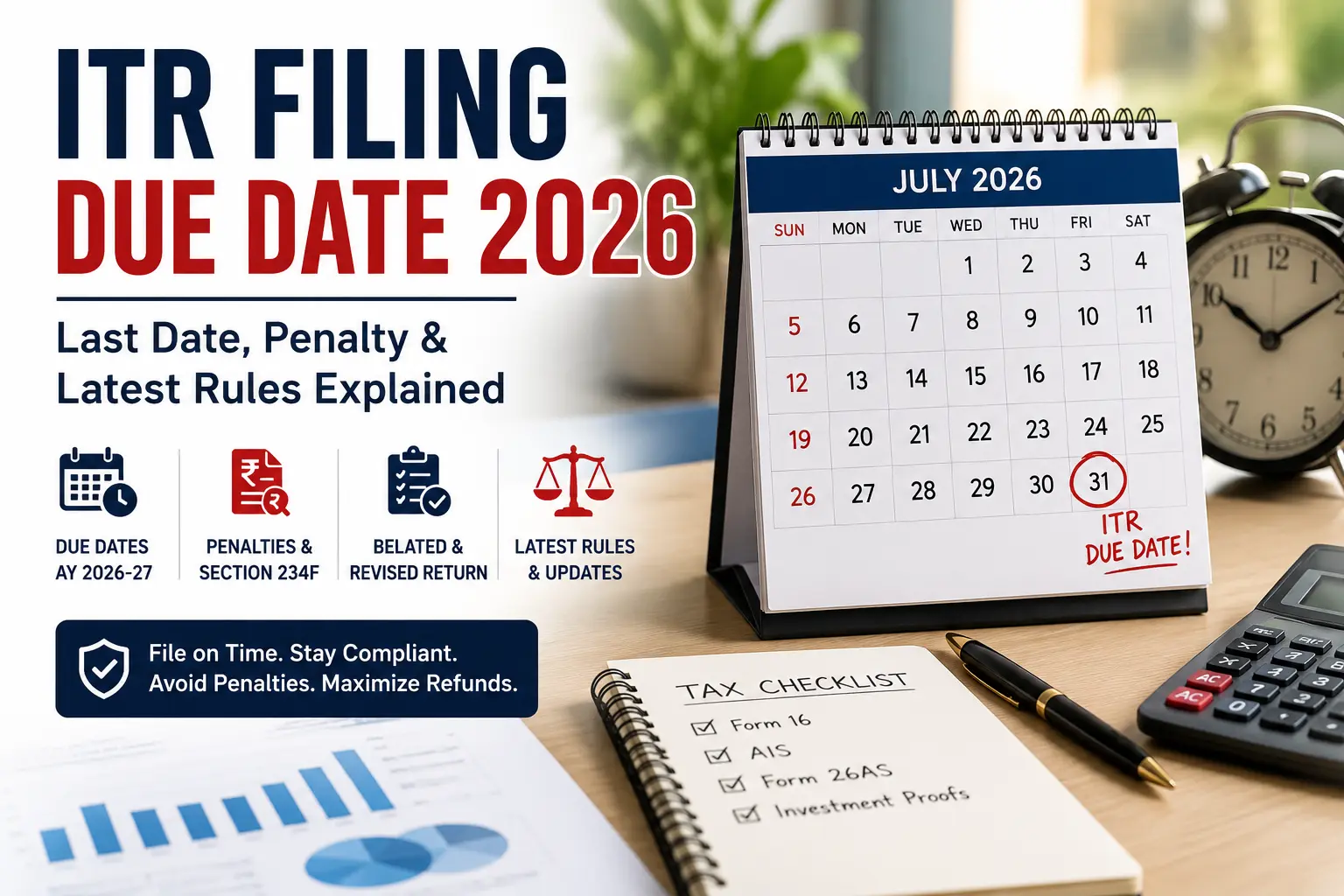

Income Tax Return Filing Due Date for AY 2026–27

The income tax return filing date depends on the taxpayer category and the complexity of tax reporting requirements. Understanding the income tax return last date of filing is important because different categories of taxpayers are subject to different compliance deadlines under the Income Tax Act.

Income Tax Return Filing Due Dates (AY 2026–27)

Taxpayer Category

Due Date (AY 2026–27)

Individuals / Salaried Employees

31 July 2026

Businesses Requiring Audit

31 October 2026

Transfer Pricing Cases

30 November 2026

Companies Requiring Audit

31 October 2026

Subject to changes or extensions announced by CBDT. For most salaried employees and individual taxpayers, the income tax return last date of filing is generally 31 July of the assessment year. This income tax return filing due date applies to taxpayers whose accounts are not required to be audited. Businesses requiring audits and taxpayers covered under transfer pricing provisions receive extended deadlines because of the complexity of their compliance obligations. Taxpayers should regularly monitor official announcements regarding the income tax return due date 2026, as the CBDT may extend deadlines due to technical issues, natural disasters, or exceptional circumstances. Missing the ITR filing due date 2026 can result in an ITR filing penalty, delayed refunds, and additional compliance requirements. Therefore, taxpayers should plan their documentation and filing activities well before the income tax return deadline to avoid last-minute issues.

Who Must File ITR Before the Due Date?

Many taxpayers assume that only high-income individuals need to file returns. In reality, filing obligations apply to a much broader group of taxpayers. The Income Tax Act imposes filing requirements on salaried individuals, freelancers, professionals, business owners, partnership firms, companies, and certain taxpayers involved in high-value financial transactions. Timely compliance becomes especially important for taxpayers expecting refunds, carrying forward losses, or requiring proof of income for future financial transactions.

Salaried Employees

Salaried employees whose income exceeds the applicable exemption limit are generally required to file an Income Tax Return. Even when employers deduct TDS correctly, filing an ITR remains important because it ensures proper tax reporting and allows taxpayers to claim refunds where applicable. Employees with multiple employers during the financial year, additional income sources, or significant investments should pay special attention to filing deadlines.

Freelancers and Professionals

Freelancers, consultants, doctors, architects, lawyers, and other professionals earning taxable income are also required to file returns within the prescribed timeline. Since professional income often comes from multiple clients and sources, maintaining proper records becomes essential to avoid last-minute filing challenges. Timely filing also helps professionals maintain compliance records and avoid unnecessary scrutiny.

Business Owners

Business owners, proprietors, and partnership firms are subject to filing requirements based on their turnover, audit applicability, and taxation method. Many small businesses operate under presumptive taxation schemes such as Section 44AD or Section 44ADA. However, even under simplified taxation systems, filing obligations continue to apply. Business taxpayers should ensure that bookkeeping and financial reporting are completed well before the due date to avoid delays.

Companies and LLPs

Companies and Limited Liability Partnerships (LLPs) are generally required to file income tax returns regardless of profit or loss situations. Because corporate compliance often involves audits and financial statement preparation, filing deadlines for companies differ from those applicable to individual taxpayers. Failure to comply can result in penalties and regulatory complications.

Taxpayers with High-Value Transactions

The Income Tax Department increasingly monitors high-value financial transactions through AIS and other reporting systems. Individuals involved in significant investments, stock market trading, foreign asset ownership, property transactions, or large banking activities may have filing obligations even when traditional income thresholds do not appear significant. Timely filing helps such taxpayers explain financial transactions properly and maintain transparent compliance records.

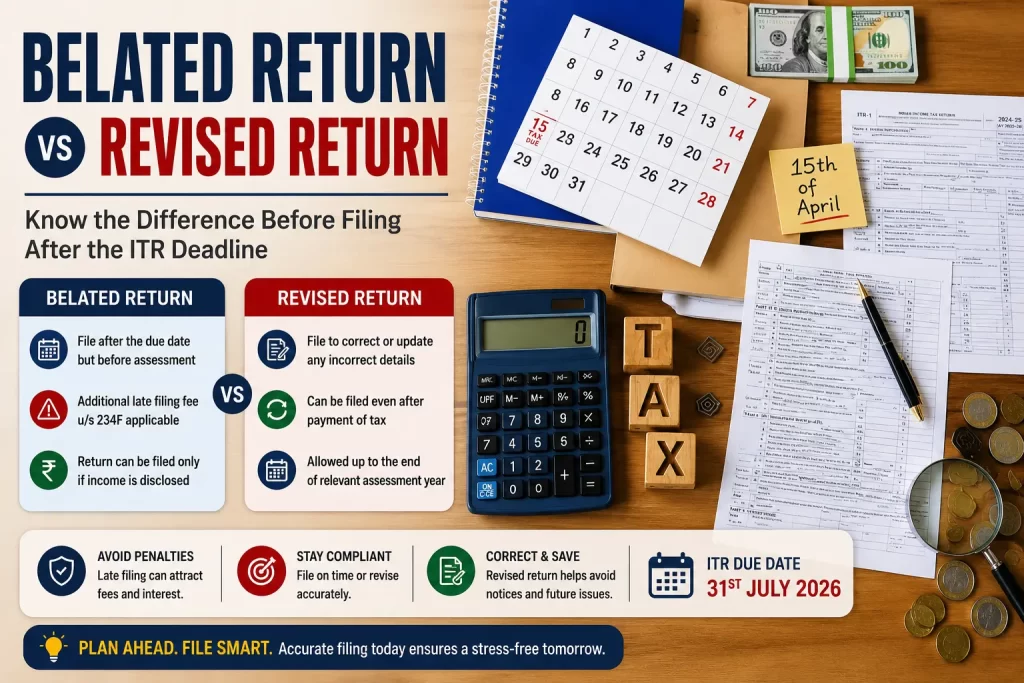

Income Tax Return Last Date of Filing vs Belated Return

One area that frequently creates confusion among taxpayers is the difference between an original return, a belated return, and a revised return. Understanding these distinctions is important for complying with the income tax return last date of filing and avoiding unnecessary penalties.

An original return refers to an ITR filed within the prescribed income tax return filing due date. This is considered the ideal form of compliance because taxpayers retain all available benefits under the Income Tax Act and avoid any ITR filing penalty. A belated return refers to an ITR filed after the income tax return deadline but within the period permitted by tax laws. While taxpayers can still file returns after missing the original deadline, certain penalties and restrictions may apply, including the section 234F penalty in eligible cases. A revised return allows taxpayers to correct mistakes or omissions in a previously filed return. This provision helps taxpayers rectify errors discovered after filing and maintain compliance with the applicable income tax return filing date requirements.

Return Type

Filing Timeline

Purpose

Original Return

Before Due Date

Regular Compliance

Belated Return

After Due Date

Late Filing Compliance

Revised Return

After Filing Original Return

Correct Errors or Omissions

Understanding the distinction between these return categories is important because each carries different implications and compliance requirements.

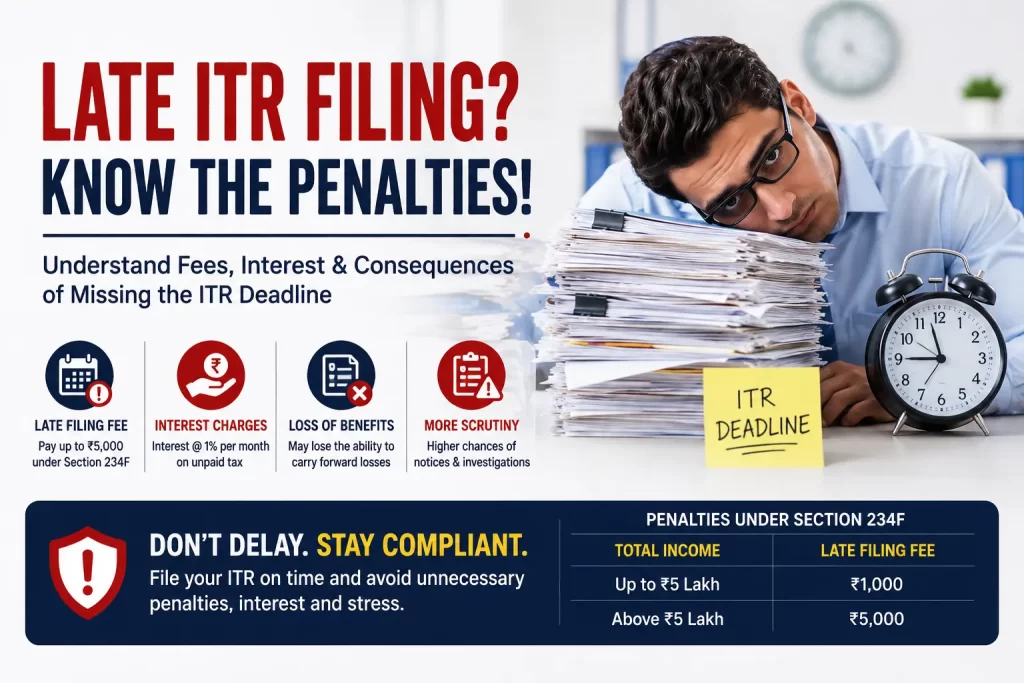

Penalty for Missing the ITR Filing Due Date

One of the biggest concerns for taxpayers is the financial consequence of missing the income tax return filing due date. The Income Tax Act imposes late filing fees and interest liabilities on taxpayers who fail to submit returns within the prescribed timeline. While the exact impact depends on the taxpayer’s circumstances, delayed filing almost always results in additional compliance costs. Taxpayers should therefore view the filing deadline as more than a procedural requirement. It directly affects financial obligations and future compliance status.

Section 234F Late Filing Fee

Section 234F of the Income Tax Act imposes a late filing fee on taxpayers who fail to submit returns before the prescribed due date. Depending on taxable income and the timing of filing, taxpayers may become liable for penalties that can reach several thousand rupees. Reduced penalties may apply to taxpayers within specified income thresholds. Although the penalty amount may appear manageable initially, it becomes an unnecessary financial burden that can easily be avoided through timely compliance.

Interest on Outstanding Tax

Apart from late filing fees, taxpayers may also face interest liabilities if any tax remains unpaid at the time of filing. Interest continues to accumulate until outstanding liabilities are fully settled. This means delayed filing can increase the overall tax burden significantly, particularly for taxpayers with substantial unpaid taxes. Understanding these implications is essential when deciding whether to postpone filing.

Loss of Benefits Due to Late Filing

Late filing can also affect valuable tax benefits. Certain losses that could otherwise be carried forward to future years may become ineligible if returns are not filed within the prescribed due date. Delayed filing may also slow refund processing and create complications when dealing with financial institutions. For taxpayers with investments, businesses, or complex income structures, these consequences can be far more costly than the penalty itself.

Consequences of Filing ITR After the Due Date

The effects of missing the income tax return filing date go beyond monetary penalties. Many taxpayers focus only on the late filing fee but overlook the broader compliance consequences that can arise from delayed filing. One of the most common consequences is a delay in receiving tax refunds. Returns filed after the due date may take longer to process because they often undergo additional verification procedures. Late filing can also affect the ability to carry forward certain losses. Taxpayers who earn capital losses or business losses may lose valuable tax-saving opportunities if they fail to file their returns within the prescribed timeline. Financial documentation may also be affected. Banks, lenders, and visa authorities frequently request recent ITR acknowledgments as proof of income. Repeated delays in filing can create unnecessary complications when applying for loans, mortgages, or international travel documentation. As compliance systems become increasingly digital, maintaining a consistent filing history is becoming more important for overall tax health.

Belated Return Filing Rules for AY 2026–27

Missing the original filing deadline does not necessarily mean taxpayers lose the opportunity to file their returns. The Income Tax Act allows taxpayers to submit a belated return if they fail to file within the prescribed due date. A belated return is essentially a delayed income tax return filed after the original deadline but within the period permitted under the law. This provision helps taxpayers remain compliant even if they miss the regular filing schedule due to personal, professional, or technical reasons. However, filing a belated return comes with certain disadvantages. Taxpayers may become liable for late filing fees under Section 234F, interest on unpaid taxes, and restrictions on carrying forward certain losses. For this reason, taxpayers should view the belated return option as a safety mechanism rather than a preferred filing method.

Who Can File a Belated Return?

Any taxpayer who was required to file an income tax return but missed the original due date can generally file a belated return within the period permitted under the Income Tax Act. This includes salaried employees, freelancers, professionals, business owners, and investors who discover that they failed to complete the filing process before the original deadline. For example, a salaried employee who forgets to file an ITR before the due date can still submit a belated return, subject to applicable rules and penalties.

Common Mistakes While Filing Belated Returns

Many taxpayers rush to complete their filing after realizing they have missed the deadline. Unfortunately, this often results in additional errors. Some taxpayers fail to verify AIS and Form 26AS information before filing. Others forget to disclose interest income, dividend income, capital gains, or other financial transactions that appear in departmental records. Another common mistake is selecting the wrong ITR form. Filing under an incorrect category can trigger defective return notices and additional compliance complications. Taxpayers should therefore approach belated filing with the same level of care as regular filing.

Revised Return Rules Explained

Even taxpayers who file their returns on time may occasionally make mistakes. This is where revised returns become important. A revised return allows taxpayers to correct errors, omissions, or inaccuracies in an already filed return. The Income Tax Department permits taxpayers to revise returns within the prescribed time limits. This facility is particularly valuable because many taxpayers discover mistakes only after reviewing AIS data, bank statements, investment reports, or tax documents in greater detail. The revised return mechanism ensures that genuine mistakes can be corrected without severe consequences when handled promptly.

When Can You Revise Your ITR?

A revised return can generally be filed when taxpayers discover errors or omissions after submitting the original return. The purpose of revision is to ensure that the information available with the Income Tax Department accurately reflects the taxpayer’s financial position and tax liability. Rather than ignoring mistakes, taxpayers should correct them as soon as possible through the revised return process.

Common Reasons for Revising Returns

One of the most common reasons for revising a return is forgotten income. Taxpayers often discover interest income, dividends, or investment gains that were accidentally omitted from the original return. In other situations, incorrect deduction claims, inaccurate salary disclosures, or errors in reporting capital gains may require revision. Some taxpayers also revise returns after identifying mismatches between AIS records and the originally filed return. The revised return facility allows taxpayers to correct these issues before they escalate into compliance problems.

Latest ITR Filing Rules and Updates for 2026

The tax filing environment has changed significantly in recent years. The Income Tax Department now relies heavily on AIS (Annual Information Statement) and TIS (Taxpayer Information Summary) for taxpayer verification. Information relating to salary income, interest income, stock market transactions, mutual fund investments, property transactions, and other financial activities is increasingly cross-verified through automated systems. Pre-filled ITR forms have also become more advanced. Taxpayers now receive returns populated with information already available to the department. While this simplifies filing, it also increases the importance of reviewing every entry carefully before submission. Artificial intelligence and data analytics are playing a larger role in compliance monitoring. Mismatches between filed returns and departmental records can trigger automated compliance communications and notices. As a result, taxpayers should focus not only on filing before the due date but also on ensuring complete and accurate disclosures.

Common Reasons Taxpayers Miss the ITR Filing Date

Every year, millions of taxpayers miss the income tax return filing due date for various reasons. Some individuals wait for Form 16 from their employers and delay filing until the last moment. Others struggle with collecting investment proofs, reconciling AIS information, or understanding which deductions they can legitimately claim. Business owners often face delays because bookkeeping records are incomplete or financial statements are still being finalized. Many taxpayers also underestimate the time required for filing and postpone compliance until the final few days before the deadline. Technical issues, website traffic congestion, and document-related problems can then create additional delays. Planning ahead remains the most effective strategy for avoiding last-minute filing stress.

Documents Required Before Filing ITR

Preparing documents in advance can make the filing process significantly smoother. Taxpayers should generally keep PAN, Aadhaar, Form 16, AIS, Form 26AS, bank statements, investment proofs, home loan statements, and details of capital gains or other income sources readily available before beginning the filing process. Having these documents organized helps reduce errors and improves the accuracy of tax reporting. It also minimizes the likelihood of notices arising from incomplete disclosures or reporting mismatches.

How to Avoid Penalties and File ITR on Time

The easiest way to avoid penalties is to start preparing well before the filing deadline. Taxpayers should review Form 16, reconcile AIS information, verify Form 26AS records, and organize supporting documents as early as possible. Waiting until the final week often increases the risk of mistakes and missed deadlines. Using the correct ITR form is equally important. Selecting the wrong form can result in defective return notices and unnecessary complications. Individuals with complex income sources, business income, stock market transactions, or foreign assets should consider seeking professional assistance rather than rushing through the filing process independently. A little preparation can save taxpayers significant time, money, and compliance stress later.

Frequently Asked Questions (FAQs)

What is the income tax return filing due date for AY 2026–27?

For most individual taxpayers and salaried employees, the income tax return filing due date is generally 31 July 2026 unless extended by the CBDT.

What happens if I miss the ITR due date?

Missing the due date may result in late filing fees under Section 234F, interest on unpaid taxes, delayed refunds, and restrictions on carrying forward certain losses.

Can I file a belated return?

Yes. Taxpayers who miss the original filing deadline can generally file a belated return within the period permitted under the Income Tax Act.

What is the penalty under Section 234F?

Section 234F imposes a late filing fee on taxpayers who fail to submit their income tax returns before the prescribed due date.

Can I revise my ITR after filing?

Yes. Taxpayers can revise their returns to correct mistakes, omissions, or inaccurate disclosures within the permitted timeline.

Will I lose my refund if I file late?

No. Eligible taxpayers can still receive refunds after filing a belated return. However, processing may take longer compared to returns filed on time.

Is filing ITR mandatory for salaried employees?

If income exceeds the applicable exemption limits or certain specified conditions are met, filing an ITR becomes mandatory.

What documents are required for ITR filing?

Commonly required documents include PAN, Aadhaar, Form 16, AIS, Form 26AS, bank statements, and investment-related documents.

Final Thoughts

Understanding the income tax return filing due date is essential for every taxpayer. Filing on time not only helps avoid penalties and interest but also ensures faster refunds, smoother financial documentation, and stronger compliance records. As tax administration becomes increasingly digital and data-driven, timely filing is no longer just a legal requirement—it is a key part of responsible financial management. Whether you are a salaried employee, freelancer, investor, or business owner, preparing documents early and filing accurately before the income tax return last date of filing can help you avoid unnecessary complications and stay compliant with the latest tax rules.

Need Help Filing Your ITR Before the Deadline?

If you are unsure about the correct income tax return filing date, need help filing a belated return, want to revise a previously filed return, or simply want professional guidance, AVC’s tax experts can assist you throughout the process. Our team helps individuals and businesses file accurate returns, avoid penalties, maximize eligible benefits, and stay compliant with the latest Income Tax Department regulations.