-

varun@avcindia.co.in

varun@avcindia.co.in

-

Inquire about Tax Services:

+91 9999 275 999

Inquire about Tax Services:

+91 9999 275 999

Every company that is registered in India under the Goods and Services Tax (GST) is required to uphold adherence to legal requirements. On the other hand, noncompliance may result in the cancellation of GST registration, a severe compliance problem that may disrupt business operations and pose a financial risk.

In this detailed guide, we explain:

Geographical Focus: India

Target Audience: MSME owners, startup founders, CFOs, compliance teams, accountants

GST registration cancellation is the formal withdrawal of a taxpayer’s GST number (GSTIN) by the tax authority, usually for non-compliance.

It can occur:

Cancellation means the business:

Must stop GST-dependent operations

India’s GST legal framework governs cancellation under:

Cancellation is generally initiated when one or more of the following occur:

One of the most frequently mentioned reasons is failing to file returns for consecutive tax periods. If returns are not received, GST authorities have the right to cancel registration and issue a show-cause notice.

Revenue authorities may cancel if:

If a business legally closes or the proprietor dies, registration can be cancelled.

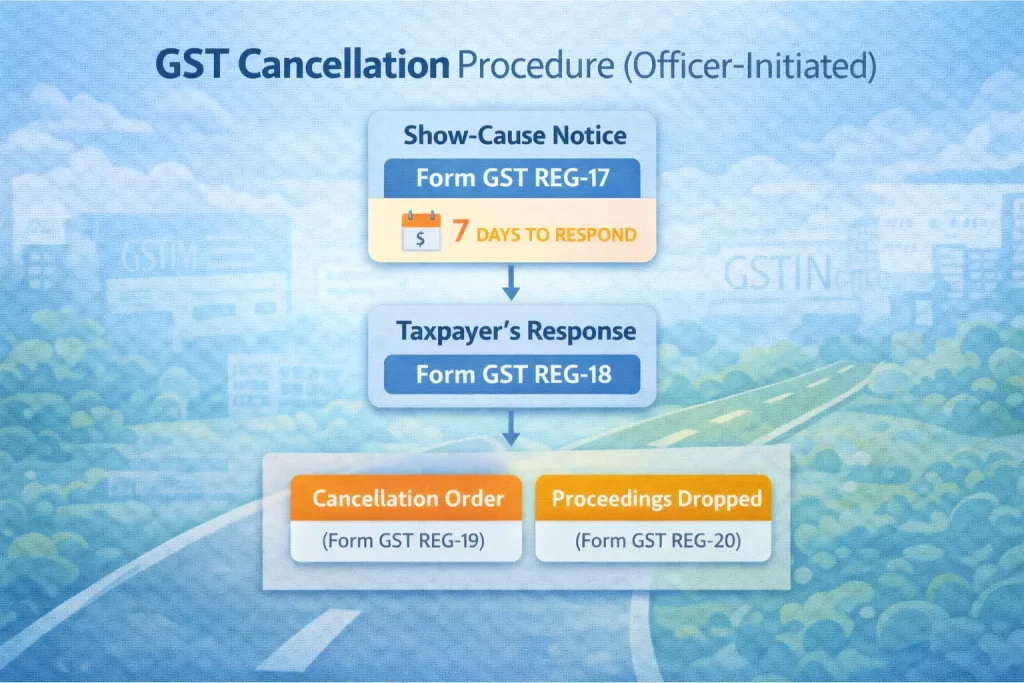

In order to adhere to natural justice, cancellation of an officer’s motion must follow a specific procedure:

The taxpayer receives a notice outlining the reasons for the proposed cancellation and requesting justifications for not proceeding with the cancellation.

Typical timeline: Usually 7 days to respond (unless extended)

The taxpayer must reply with:

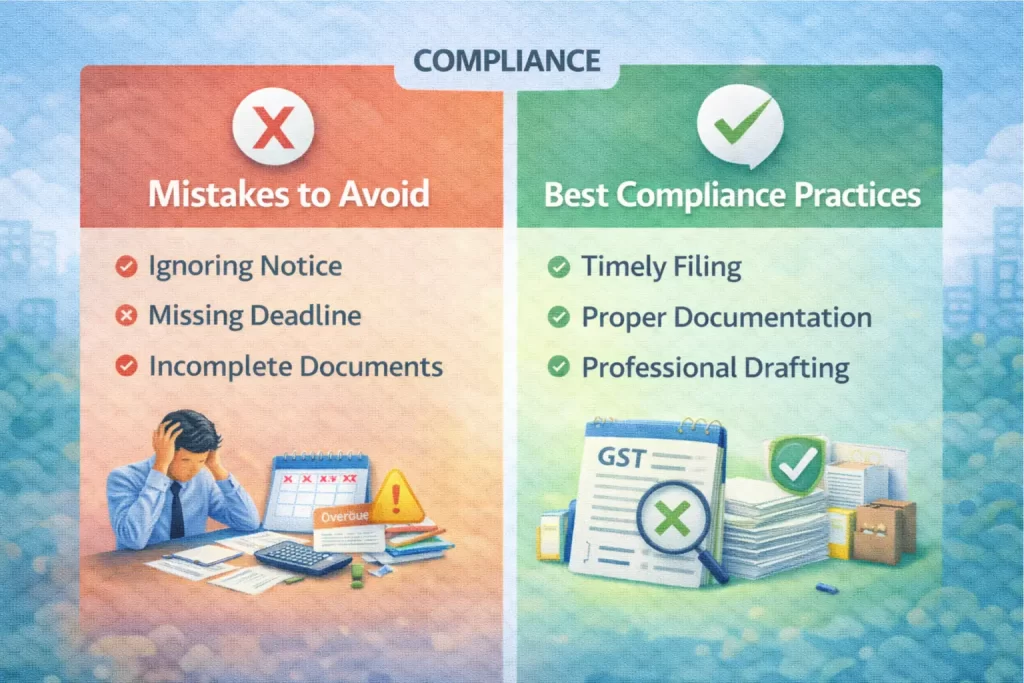

Common mistakes business owners make at this stage:

After reviewing the reply, the officer may:

Once cancelled, the taxpayer is notified and all GST obligations cease.

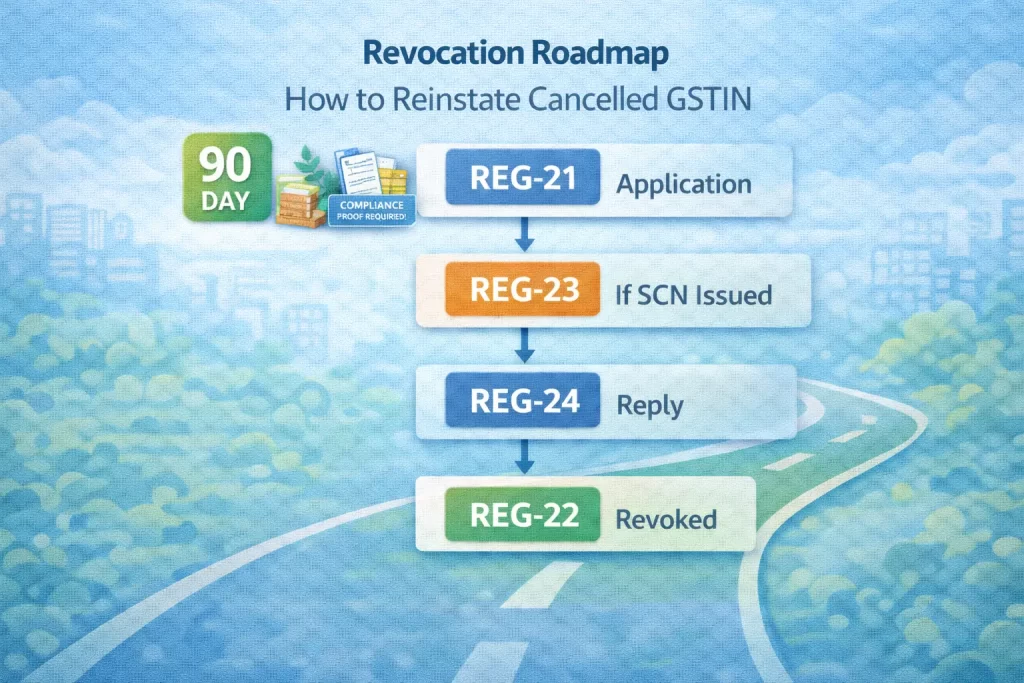

If your registration is cancelled, you can apply for revocation i.e., reinstating GST registration subject to conditions:

Note: Forms must be submitted within specified timeframes.

Even when statutory procedures are followed, businesses often slip up due to:

✔ Maintain timely GST return filings

✔ Reconcile GSTR-2B and GSTR-3B every month

✔ Keep proof of business existence & operations

✔ Respond in Form GST REG-18 comprehensively

✔ Consult a professional for notice replies

Time Window: Usually, 7 days to respond

Time Window: As per the notice

Time Window: Once reviewed

Time Window: Within 90 days (or as allowed)

Time Window: Post review

GST cancellation is the withdrawal of GSTIN due to non-compliance, and it occurs after proper notice and opportunity to respond.

Yes, through Form GST REG-21 before the specified statutory window closes.

Typically around 7 days, but timelines may vary based on notice.

Return filings, proof of business operations, tax payment receipts, and a detailed explanation for compliance.

Responding to GST cancellation and revocation notices requires:

At AVC India, our GST experts:

✔ Review notices carefully

✔ Draft replies with legal precision

✔ Help reconcile overdue returns

✔ Guide you through revocation process

Contact AVC India to protect your GST registration and maintain uninterrupted compliance.