Small business owners in India often struggle with tax compliance, bookkeeping, and audit requirements. To simplify taxation for small taxpayers, the government introduced Section 44AD of the Income Tax Act under the presumptive taxation scheme. Section 44AD allows eligible businesses to declare income at a fixed percentage of turnover instead of maintaining detailed books of accounts.

This significantly reduces compliance burdens for traders, shop owners, retailers, and small businesses. Understanding what is Section 44AD of Income Tax Act is important for taxpayers who want to simplify record-keeping and reduce compliance costs. Over the last few years, presumptive taxation under Section 44AD has become increasingly important because the Income Tax Department has strengthened digital scrutiny systems through AIS, TIS, AI-driven monitoring, and transaction-based verification.

As a result, businesses opting for Section 44AD of Income Tax Act must understand not only its benefits but also its limitations, Section 44AD eligibility conditions, audit triggers, and compliance obligations. Businesses should also monitor the Section 44AD turnover limit and the latest Section 44AD turnover limit 2026 updates to ensure continued eligibility under the scheme.

This guide explains Section 44AD of Income Tax Act in simple language, including turnover limits, tax calculation, Section 44AD applicability, eligibility conditions, audit rules, practical examples, and common mistakes taxpayers should avoid. It also covers how Section 44AD for partnership firms works and when businesses may benefit from choosing the presumptive taxation scheme.

What Is Section 44AD of Income Tax Act?

Section 44AD of Income Tax Act is a presumptive taxation provision under the Income Tax Act, 1961 that allows eligible small businesses to declare income at a prescribed percentage of turnover without maintaining detailed books of accounts. Under the presumptive taxation under Section 44AD framework, the government “presumes” a fixed percentage of business turnover as taxable income.

Instead of calculating every individual business expense, taxpayers can pay tax on presumptive income directly. The main objective behind Section 44AD of Income Tax Act is to reduce the compliance burden for small businesses and encourage voluntary tax compliance through the presumptive taxation scheme.

Understanding what is Section 44AD of Income Tax Act is important for business owners because the scheme offers a simplified taxation method while reducing bookkeeping requirements. The scheme is especially beneficial for small traders, retailers, local businesses, proprietorship concerns, and businesses that satisfy the Section 44AD eligibility criteria.

Businesses must also keep track of the Section 44AD turnover limit and the updated Section 44AD turnover limit 2026 provisions to ensure continued eligibility. This guide further explains Section 44AD applicability, the treatment of Section 44AD for partnership firms, and the practical benefits of opting for the presumptive taxation scheme.

Who Is Eligible Under Section 44AD?

Section 44AD is available only to specific categories of taxpayers and businesses. Resident individuals, Hindu Undivided Families (HUFs), and partnership firms can opt for presumptive taxation under this section. However, LLPs are not eligible for Section 44AD benefits. The scheme generally applies to small businesses engaged in trading, retailing, manufacturing, and similar business activities. However, certain businesses are specifically excluded from eligibility. Commission-based businesses, agency businesses, and professionals covered under Section 44ADA cannot opt for Section 44AD. Businesses earning income from brokerage or commission activities are also excluded from the scheme. Understanding eligibility properly is extremely important because incorrect usage of Section 44AD can trigger notices and audit complications later.

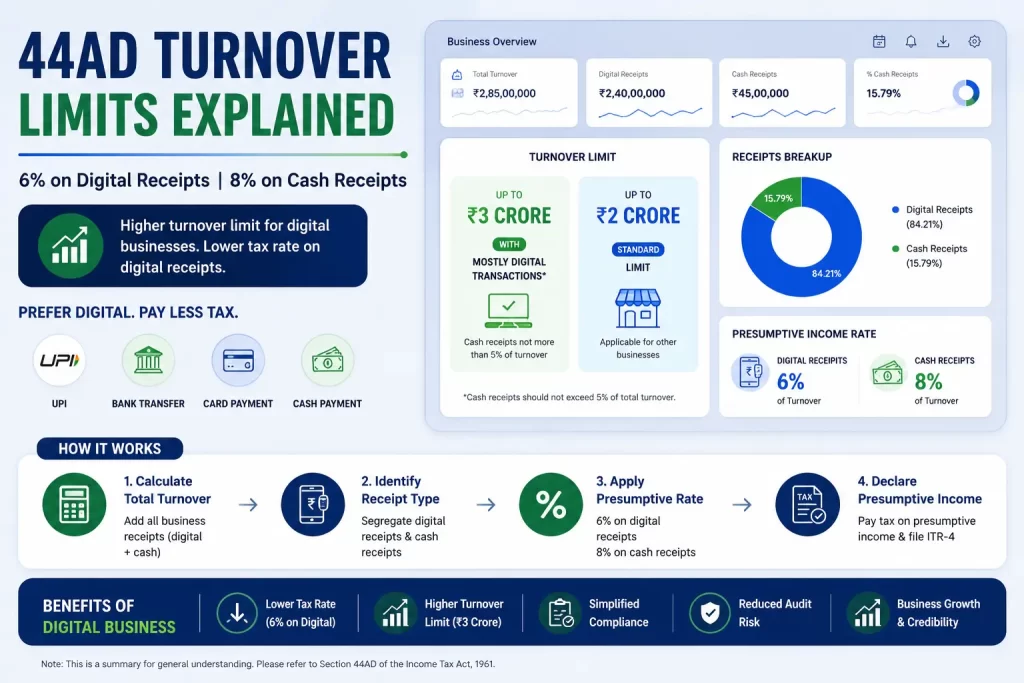

Section 44AD Turnover Limit for FY 2025–26

The turnover limit is one of the most important aspects of Section 44AD. Traditionally, the presumptive taxation scheme applied to businesses with annual turnover up to ₹2 crore. However, the government later introduced an enhanced threshold of ₹3 crore for businesses with predominantly digital transactions. To qualify for the ₹3 crore limit, cash receipts during the financial year should not exceed 5% of total turnover. This change was introduced to encourage digital transactions and formal financial reporting. Businesses with excessive cash transactions may still remain restricted to the standard ₹2 crore turnover limit.

6% and 8% Presumptive Income Rule

One of the most important features of Section 44AD is the presumptive income calculation mechanism.

Receipt Type| Presumptive Income Rate

Digital Receipts| 6%

Cash Receipts| 8%

Businesses receiving payments through UPI, bank transfer, cheque, or digital methods can declare income at 6% of turnover. However, cash receipts are taxed at 8% presumptive income. For example, if a business earns ₹80 lakh through digital receipts and ₹20 lakh through cash receipts, presumptive income will be calculated separately using both rates. This distinction has become extremely important because the government now strongly promotes digital business transactions.

How Income Is Calculated Under Section 44AD

Under Section 44AD, taxable income is calculated as a fixed percentage of turnover rather than actual profit. Suppose a retailer has annual turnover of ₹1 crore. If ₹90 lakh is received digitally and ₹10 lakh is received in cash, the presumptive income calculation would work as follows:

– 6% of ₹90 lakh = ₹5.4 lakh

– 8% of ₹10 lakh = ₹80,000

The total presumptive income becomes ₹6.2 lakh. The taxpayer can directly pay taxes on this presumptive income without maintaining extensive books of accounts. However, if the actual business profit is higher than presumptive income, taxpayers are expected to disclose accurate profits appropriately.

Benefits of Section 44AD for Small Businesses

Section 44AD offers major compliance advantages for small businesses. The biggest benefit is simplified taxation. Taxpayers do not need to maintain detailed accounting records like larger businesses. In most cases, businesses opting for Section 44AD can also avoid mandatory tax audits, which significantly reduces compliance costs. The scheme also simplifies ITR filing and makes tax calculation easier for small business owners who may not have advanced accounting systems. For many local traders and retailers, this reduces both financial and administrative pressure. Digital businesses benefit further because lower presumptive taxation rates apply to digital receipts.

Disadvantages and Risks of Section 44AD

Despite its simplicity, Section 44AD may not suit every business model. Businesses with high operating expenses may end up paying higher taxes because actual expenses cannot be separately claimed under presumptive taxation. The five-year lock-in rule also creates long-term compliance implications for taxpayers who frequently switch taxation methods. Additionally, businesses declaring unusually low profits despite large turnover may attract scrutiny from the Income Tax Department’s AI-driven compliance systems. Taxpayers should therefore compare presumptive taxation with normal taxation before opting into the scheme.

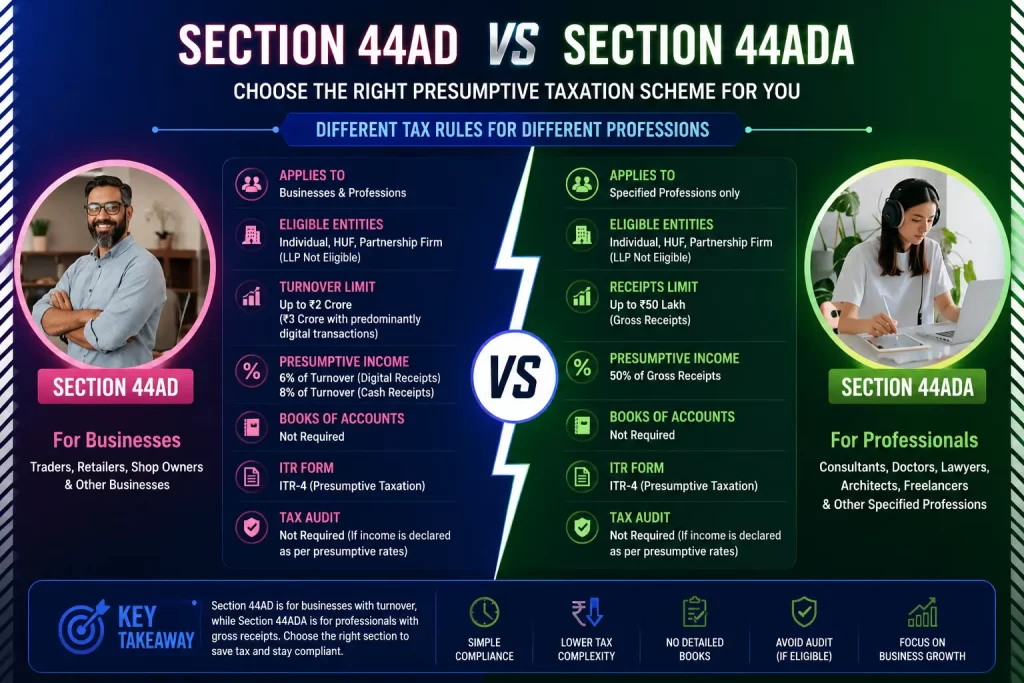

Section 44AD vs Section 44ADA

Many taxpayers confuse Section 44AD with Section 44ADA, but both provisions apply to different categories of taxpayers. Section 44AD applies mainly to businesses such as traders, retailers, and small commercial establishments. Section 44ADA, on the other hand, applies to specified professionals including consultants, architects, doctors, lawyers, and freelancers. Another major difference is the presumptive income percentage. Section 44ADA generally presumes 50% of professional receipts as taxable income, whereas Section 44AD follows the 6% and 8% turnover-based calculation system. Understanding this distinction is important because choosing the wrong presumptive scheme may create compliance issues.

Tax Audit Rules Under Section 44AD

One of the biggest reasons taxpayers opt for Section 44AD is to avoid tax audits under Section 44AB. However, audit exemption applies only if taxpayers comply properly with presumptive taxation conditions. If a taxpayer declares income lower than the prescribed presumptive rates while total income exceeds the basic exemption limit, tax audit requirements may become applicable. Similarly, businesses crossing turnover limits under Section 44AD may also become subject to regular audit provisions. This is why proper turnover reporting and income disclosure remain extremely important.

The 5-Year Lock-In Rule Explained

The five-year lock-in rule is one of the most misunderstood aspects of Section 44AD. Once a taxpayer opts for presumptive taxation under Section 44AD, the expectation is that the scheme will continue for five consecutive assessment years. If the taxpayer voluntarily opts out before completing the five-year period, they may become ineligible to use Section 44AD again for the next five years. Additionally, audit and bookkeeping requirements may apply during this period if income exceeds prescribed limits. Many small businesses ignore this rule while making short-term tax decisions, which later creates compliance complications.

Advance Tax Rules Under Section 44AD

Instead of paying advance tax in multiple installments, eligible taxpayers can generally pay 100% advance tax in a single installment before March 15 of the financial year. Failure to pay advance tax within the prescribed timeline may attract interest liabilities under applicable provisions.

Common Mistakes Taxpayers Make Under Section 44AD

Many taxpayers misuse Section 44AD because they misunderstand eligibility rules or presumptive taxation conditions. One common mistake is mixing professional income with business income. Professionals covered under Section 44ADA should not incorrectly file under Section 44AD. Another common issue is incorrect turnover reporting or ignoring digital transaction rules. Some businesses also assume that Section 44AD completely eliminates scrutiny risk. However, AI-based compliance systems now monitor turnover patterns, bank transactions, GST data, AIS records, and financial reporting more closely than before. Taxpayers should therefore maintain reasonable documentation even under presumptive taxation.

Is Section 44AD Beneficial for Your Business?

Section 44AD is highly beneficial for businesses with simple operations, limited accounting infrastructure, and moderate profit margins. Small retailers, local traders, shop owners, and businesses with mostly digital transactions often benefit significantly from simplified compliance and reduced audit burden. However, businesses with high operational expenses, fluctuating profits, or complex accounting structures may find normal taxation more beneficial. The decision should be based on long-term tax planning rather than only short-term compliance convenience.

Frequently Asked Questions (FAQs)

What is Section 44AD of Income Tax Act?

Section 44AD is a presumptive taxation provision that allows eligible small businesses to declare income at fixed prescribed rates without maintaining detailed books of accounts.

Who is eligible for Section 44AD?

Resident individuals, HUFs, and partnership firms engaged in eligible businesses can opt for Section 44AD.

What is the turnover limit under Section 44AD?

The standard turnover limit is ₹2 crore. However, businesses with mostly digital transactions may qualify for the enhanced ₹3 crore limit.

Can professionals use Section 44AD?

No. Professionals covered under Section 44ADA cannot opt for Section 44AD.

Is tax audit mandatory under Section 44AD?

Not usually. However, audit may become mandatory if income is declared below presumptive rates while exceeding exemption limits.

What is the 6% and 8% rule under Section 44AD?

Digital receipts are taxed at 6% presumptive income, while cash receipts are taxed at 8%.

Can LLP opt for Section 44AD?

No. LLPs are not eligible under Section 44AD.

Which ITR form is used for Section 44AD?

Eligible taxpayers generally file ITR-4 under presumptive taxation.

Final Thoughts on Section 44AD

Section 44AD remains one of the most useful tax compliance provisions for small businesses in India. It simplifies taxation, reduces audit burden, and encourages easier compliance for eligible taxpayers. However, businesses should not treat presumptive taxation as a shortcut without understanding its long-term implications. With increasing digital scrutiny, AI-based monitoring systems, and transaction-level verification, accurate reporting under Section 44AD has become more important than ever. Businesses should carefully evaluate turnover structure, digital transactions, audit risks, and future growth plans before opting into presumptive taxation.

Need Professional Help With Section 44AD Filing?

If you are unsure whether Section 44AD is suitable for your business, AVC’s tax professionals can help you evaluate eligibility, calculate presumptive income correctly, avoid audit risks, and file your ITR accurately under the Income Tax Act.