-

varun@avcindia.co.in

varun@avcindia.co.in

-

Inquire about Tax Services:

+91 9999 275 999

Inquire about Tax Services:

+91 9999 275 999

Mistakes in tax returns are more common than most taxpayers realize.

Missed bank interest, forgotten capital gains, incorrect deductions, or unreported foreign income can easily lead to compliance risks. Recognizing this reality, the Indian government introduced Section 139(8A) through the Finance Act 2022, allowing taxpayers to correct past errors using an Updated Return (ITR-U).

This mechanism allows individuals, professionals, startups, and MSMEs to voluntarily disclose missed income and correct errors, even years after the original filing deadline.

In this comprehensive guide by AVC India, we explain:

An Updated Return is a special tax return filed under Section 139(8A) of the Income Tax Act, 1961 that allows taxpayers to correct previously filed returns or declare missed income.

Unlike revised returns, updated returns are designed primarily for voluntary disclosure of under-reported income.

The objective is simple:

Encourage voluntary compliance while reducing litigation and tax disputes.

The government introduced this mechanism as part of its “trust-based tax governance” approach.

| Feature | Revised Return | Updated Return |

|---|---|---|

| Purpose | Correct mistakes | Declare missed income |

| Filing deadline | 31 December of the assessment year | Up to 48 months after AY |

| Additional tax | No additional tax | 25%–70% additional tax |

| Refund | Can increase the refund | Refund cannot increase |

| Loss | Can increase loss | Loss can only decrease |

| Filing frequency | Multiple revisions allowed | Only once |

This means ITR-U should only be used for compliance correction, not tax planning.

Any taxpayer can file an updated return, including:

Updated returns can be filed whether or not an original return was filed.

Updated return filing is commonly used when taxpayers discover:

Examples include:

Errors in:

Sometimes deductions are wrongly claimed under:

Taxpayers who mistakenly chose the wrong regime may need corrections.

The law restricts ITR-U in several cases.

An updated return cannot be filed if:

The mechanism exists strictly for additional disclosure of income.

Following the Finance Act amendments, taxpayers can file updated returns up to 48 months from the end of the relevant assessment year.

Example

| Financial Year | Assessment Year | Last Date for Updated Return |

|---|---|---|

| FY 2022-23 | AY 2023-24 | 31 March 2028 |

| FY 2023-24 | AY 2024-25 | 31 March 2029 |

This extended window provides taxpayers ample time to correct mistakes discovered later.

Filing an updated return comes with an additional tax cost.

The government charges a compliance premium depending on how late the correction is made.

| Time after Assessment Year | Additional Tax |

|---|---|

| Up to 12 months | 25% additional tax |

| 12–24 months | 50% additional tax |

| 24–36 months | 60% additional tax |

| 36–48 months | 70% additional tax |

This additional tax applies to:

The longer a taxpayer waits, the higher the penalty.

Here is the practical process followed by tax professionals.

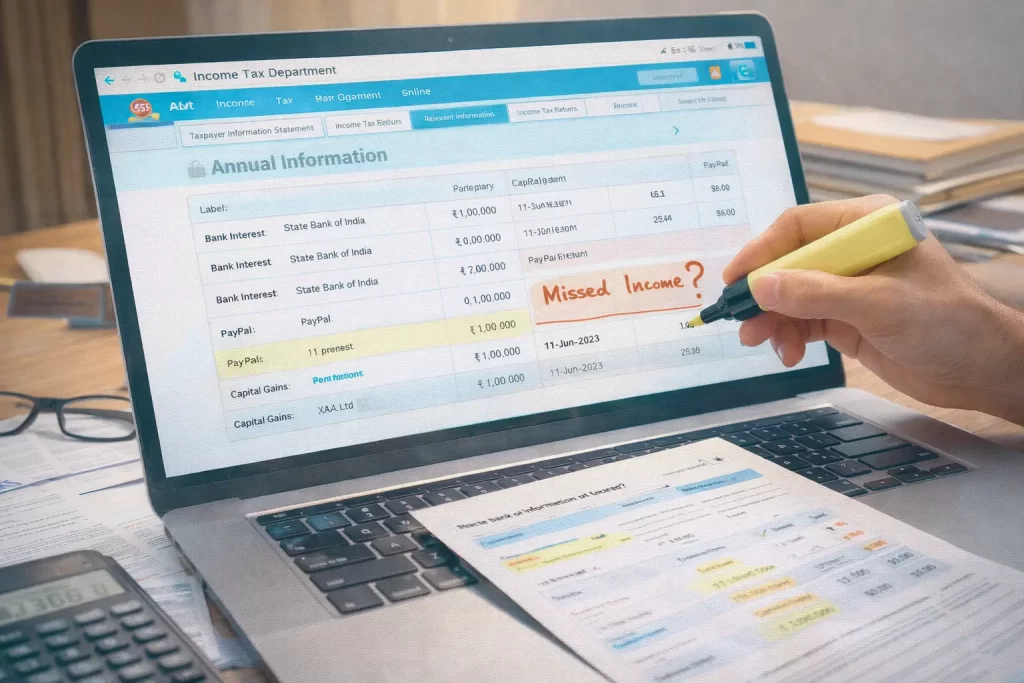

Analyze the Annual Information Statement (AIS) and Taxpayer Information Summary (TIS) to identify mismatches.

Reconcile:

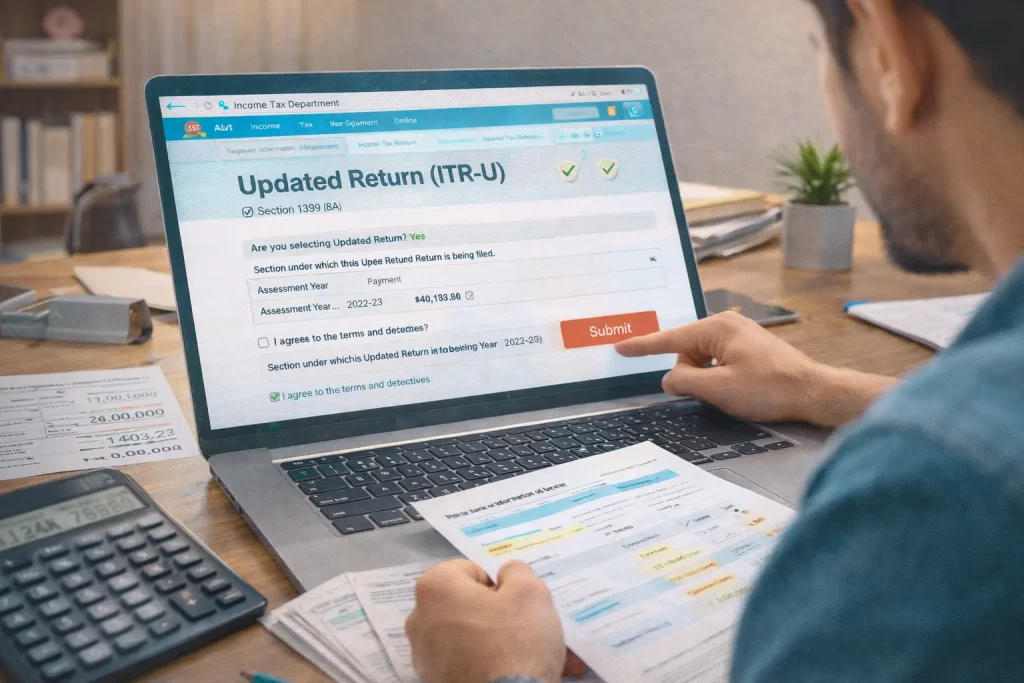

Select the same ITR form used previously (ITR-1, ITR-2, ITR-3 etc.).

Choose “Updated Return under Section 139(8A)” on the income tax portal.

Before filing, tax must be paid using Challan ITNS 280.

Submit the updated return through the Income Tax e-filing portal.

External reference:

https://www.incometax.gov.in

Verification can be done using:

The return must be verified within 30 days.

A freelance designer forgot to report ₹3 lakh received via PayPal.

Using ITR-U allows them to disclose the income voluntarily and avoid scrutiny notices.

A startup realised it overstated losses by ₹10 lakh.

Updated returns can be used to reduce carried-forward losses, ensuring clean books before raising funding.

An investor forgot to report cryptocurrency gains.

ITR-U allows correction before the department flags the transaction through AIS data.

Ignoring tax discrepancies can lead to serious consequences.

Possible outcomes include:

Voluntary correction through ITR-U significantly reduces litigation risk.

Tax professionals generally recommend filing ITR-U when:

However, taxpayers should avoid filing ITR-U without professional review because:

A critical issue arises when taxpayers disclose foreign assets.

While ITR-U allows disclosure of missed foreign income, the Black Money Act, 2015, does not fully recognize updated returns.

This means taxpayers must carefully evaluate a compliance strategy before using ITR-U for foreign asset corrections.

Professional guidance becomes essential in such cases.

ITR-U is an updated income tax return filed under Section 139(8A) to disclose missed income or correct errors.

Only once per assessment year.

No. Refund claims cannot be increased using ITR-U.

Yes, following recent amendments, losses can be reduced but not increased.

Additional tax ranges from 25% to 70% depending on the delay.

Filing an updated return requires careful tax analysis and accurate computation.

At AVC India, our chartered accountants assist with:

If you suspect errors in past tax returns, professional advice can prevent serious compliance issues.

👉 Contact AVC India for expert assistance with Income Tax Return corrections and ITR-U filing.