8 Common Income Tax Notice Reasons are one of the most searched topics during the ITR filing season, as taxpayers often receive notices due to data mismatches, reporting errors, or undisclosed financial activities. The 8 most common income tax notice reasons in India include a mismatch between your ITR and Form 26AS, income recorded in AIS that was not reported, salary discrepancies after changing jobs, inflated or unsupported deduction claims, large refund claims, high-value financial transactions not backed by declared income, non-disclosure of foreign assets, and unreported cryptocurrency gains. These notices are usually generated by the Income Tax Department’s automated CPC systems rather than manual scrutiny, meaning even a small data inconsistency can trigger a notice.

How the Income Tax Department Knows Your Financial Activity

Income Tax Notice Reasons are often linked to the Income Tax Department’s advanced data-matching systems. Many taxpayers believe the department can only see what they declare in their ITR. That is no longer true. Since AY 2021-22, the department has operated a fully automated data pipeline that ingests financial information from dozens of reporting entities and cross-checks it against your return in real time.

The automated data flow:

Banks / Brokers / Mutual Funds / Registrars / Employers / Crypto Exchanges → Report via Form 61A / Statement of Financial Transactions (SFT) → Income Tax Insight Portal → Annual Information Statement (AIS) + Taxpayer Information Summary (TIS) → CPC Automated Matching Engine → Income Tax Notice issued without any human review

Because this system runs automatically, many income tax notice reasons can be traced to data mismatches, unreported transactions, or inconsistencies detected by the CPC even before any Assessing Officer reviews the case.

Understanding AIS, TIS, and Form 26AS

Annual Information Statement (AIS)

AIS is one of the most important sources behind many Income Tax Notice Reasons because it serves as your complete financial transaction ledger for the year. It aggregates data submitted by third-party reporting entities and displays it under your PAN. AIS captures salary, interest income, dividend income, mutual fund transactions, share transactions, property transactions, foreign remittances, rental income, tax payments, and VDA/crypto transactions reported through Section 194S TDS.

Taxpayers can submit feedback on AIS entries through the e-filing portal to flag inaccurate or duplicate data before filing. Reviewing AIS carefully can help prevent common income tax notice reasons arising from mismatches between reported financial information and the income declared in your ITR.

Taxpayer Information Summary (TIS)

TIS is the deduplicated, category-wise summary derived from AIS. It removes duplicate entries, consolidates income into categories, and generates an “accepted value” after your feedback. Understanding these income tax notice details is important because the TIS accepted value is what pre-fills your ITR and what the CPC compares against your filed figures. Any mismatch between TIS and your return can become one of the common income tax notice reasons identified by the Income Tax Department.

Form 26AS

Form 26AS is the official tax credit statement. It records TDS deducted by employers, banks, and others; TCS collected; advance tax paid; and self-assessment tax paid. When a conflict exists between AIS and Form 26AS, Form 26AS takes precedence for tax credit verification.

Income-tax Act 2025 Transition Note: Under the Income-tax Act 2025, Form 26AS is referred to as Form 168 in the new section numbering. No action is required from taxpayers the portal still displays it as Form 26AS.

High-Value Transactions That Can Trigger an Income Tax Notice

Under Rule 114E, specified institutions report high-value transactions via Statement of Financial Transactions (SFT). These appear in AIS. If your income cannot plausibly explain these transactions, the return is flagged.

Transaction Type

Reporting Threshold

Who Reports

Cash Deposits in Savings Account

₹10 Lakh in a Financial Year

Banks

Cash Deposits / Withdrawals — Current Account

₹50 Lakh in a Financial Year

Banks

Fixed Deposit (FD) Receipts

₹10 Lakh

Banks / NBFCs

Credit Card Payments (Cash Mode)

₹1 Lakh per Transaction

Banks

Credit Card Bill Payment (Any Mode)

₹10 Lakh in a Year

Banks

Mutual Fund Purchases

₹10 Lakh

AMCs / RTAs

Share / Debenture Purchases

₹10 Lakh

Brokers / Companies

Immovable Property Transactions

₹30 Lakh

Registrar

Foreign Currency / Overseas Remittances

₹10 Lakh

Authorised Dealers

Purchase of Bonds / Debentures

₹10 Lakh

Companies

Crypto / VDA Transactions (TDS)

All Transactions Above ₹10,000

Crypto Exchanges (Section 194S)

8 Common Reasons You Can Get an Income Tax Notice in India

1. Mismatch Between Your ITR and Form 26AS

This is the single most common trigger. Every TDS credit claimed in your ITR is automatically verified against Form 26AS by the CPC. If the credit does not appear in Form 26AS, the CPC will reject it and issue a notice.

Common causes: incorrect PAN in TDS return; late TDS filing by employer; data entry error by deductor; job change with TDS under old employer’s details.

How to avoid it: Download Form 26AS at least two weeks before filing. Compare with your Form 16, Form 16A, and bank TDS certificates. Chase missing TDS entries before the filing deadline.

2. Income Appearing in AIS Not Reported in Your ITR

The CPC compares TIS accepted values with your ITR. Income present in TIS but absent from your return triggers a mismatch notice under Section 143(1)(a)(vi).

Frequently missed items: Interest income whether from fixed deposits, savings accounts, recurring deposits, or bonds is one of the most systematically under-reported income categories in India, largely because many taxpayers assume TDS deducted by the bank closes their tax liability. It does not. The bank deducts TDS at 10%, but if your total income pushes you into the 20% or 30% slab, additional tax remains payable. For a complete guide to how TDS on interest works, which thresholds apply bank-by-bank, and how to correctly report it in your ITR, read: Section 194A: TDS on Interest Income Complete Guide

How to avoid it: Open AIS on the e-filing portal. Review every line item. Submit feedback for incorrect entries. Include all correct items in your ITR.

3. Salary Mismatch After Changing Jobs

The department combines salary data from all employers and compares it with your ITR. Specific errors: omitting previous employer’s salary; claiming the standard deduction twice; not submitting Form 12B to the new employer.

How to avoid it: Collect Form 16 from every employer. Aggregate all salary in the ITR. Claim standard deduction only once (₹75,000 for FY 2025-26).

4. Incorrect, Inflated, or Unsubstantiated Deduction Claims

Deductions under Sections 80C, 80D, 80G, and HRA are scrutinised — especially when unusually high relative to income. Common errors: claiming 80C without actual investments; HRA without rent receipts; 80G without valid registration numbers.

How to avoid it: Maintain documentary evidence for every deduction claimed. Do not estimate figures.

5. Large or Unjustified Income Tax Refund Claims

Large refund claims automatically undergo risk-based assessment. The CPC may hold the refund or issue a notice requiring explanation.

How to avoid it: Ensure every TDS credit has a matching Form 26AS entry. Respond promptly to any 143(1) intimation before the refund is processed.

6. High-Value Transactions Not Supported by Declared Income

If your ITR shows modest income but AIS records large property purchases, significant MF investments, or large cash deposits, the CPC flags the inconsistency using an income-adequacy check.

How to avoid it: One legitimate source that frequently explains large transactions without proportionate income is a gift from a close relative — which is completely exempt from tax under Section 56(2)(x). However, the gift must be properly documented with a gift deed and, for cash gifts, must comply with the ₹2 lakh limit under Section 269ST. For a full explanation of which gifts are tax-free, which relatives qualify, and the Gurgaon-specific stamp duty benefit for property gifts, read: Gift Tax in India: Which Gifts Are Tax-Free and How to Save Tax Legally

7. Failure to Disclose Foreign Assets (Schedule FA)

Resident and Ordinarily Resident taxpayers must disclose all foreign assets in Schedule FA, regardless of income generated. Assets include: foreign bank accounts, US stocks, RSUs, ESOPs, foreign real estate, and signing authority in any foreign account.

Non-disclosure penalty under the Black Money Act: ₹10 lakh per asset.

How to avoid it: Report all foreign assets in Schedule FA, even if no income was earned.

8. Unreported or Incorrectly Reported Cryptocurrency Transactions

Crypto exchanges deduct 1% TDS under Section 194S of the Income Tax Acton transactions above ₹10,000 and report these to the department. Gains appear in AIS and Form 26AS. Under Section 115BBH, VDA gains are taxed at 30% flat no deductions except cost of acquisition, and no loss set-off against other income.

Common errors: not filling Schedule VDA; calculating gains incorrectly; attempting to set off crypto losses against non-VDA income.

How to avoid it: Export transaction history from every exchange. Calculate gains per asset. Fill Schedule VDA. Verify TDS against Form 26AS.

Income Tax Notice Reasons by Taxpayer Type

Salaried Employees: Salary mismatch from multiple employers, HRA without rent receipts, undeclared interest income, Form 26AS TDS mismatch.

Business Owners: GST turnover vs ITR income mismatch, large cash deposits, inconsistent profit margins.

Investors: Capital gains not reported, dividend mismatch, large SFT-reported transactions, crypto in Schedule VDA missing.

NRIs: Non-filing despite NRO interest TDS, rental income from Indian property, foreign asset disclosure on return to India.

Crypto Investors: Schedule VDA missing or incomplete, loss set-off attempted, foreign exchange TDS not in Form 26AS.

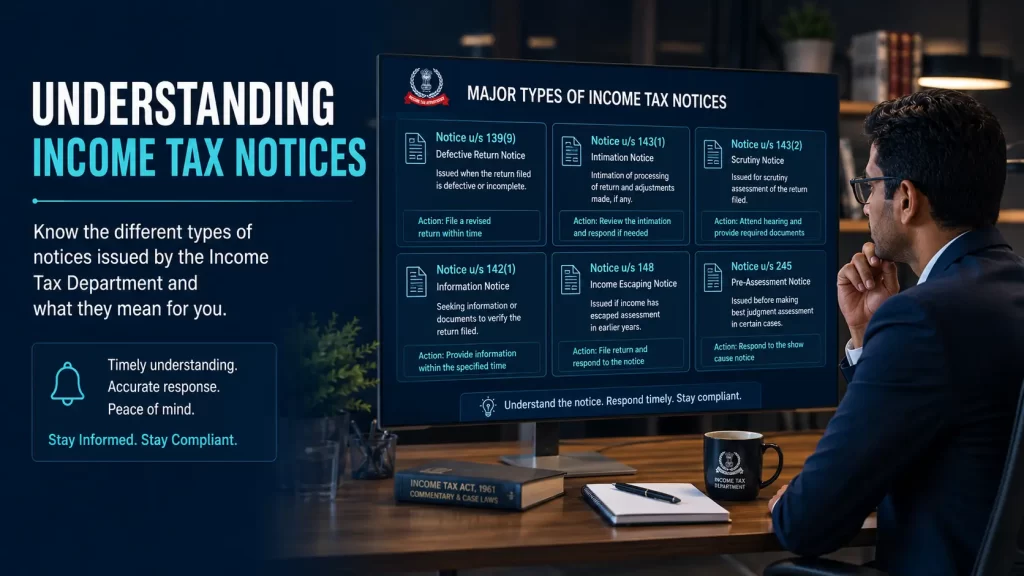

Types of Income Tax Notices in India (2026)

Section 139(9) – Defective Return Notice

An income tax notice under Section 139(9) is issued when the ITR is structurally incomplete or contains missing information. Taxpayers must respond within 15 days; otherwise, the return may be treated as not filed.

Section 143(1) – CPC Processing Intimation

One of the most common income tax notice details received by taxpayers is the Section 143(1) intimation. It may confirm that the return has been accepted or highlight adjustments. Respond within 30 days if a tax demand is raised.

Section 143(2) – Scrutiny Notice

Among the major income tax notice reasons, selection for scrutiny under Section 143(2) is one of the most important. This notice requires the taxpayer to provide additional information or explanations. For AY 2025-26, it must be issued by 30 June 2026.

Section 142(1) – Pre-Assessment Inquiry

An income tax notice Section 142(1) is issued when the department seeks documents, explanations, or even requires the filing of a return. Non-compliance can result in penalties under Section 272A.

Section 148A / Section 148 – Reassessment Notice

An income tax notice Section 148A ITR proceeding generally begins before a reassessment notice is issued under Section 148. These notices apply when the department believes income has escaped assessment. The reassessment period can extend up to 3 years or, in certain cases, up to 10 years.

Section 245 – Refund Adjustment Notice

This notice informs taxpayers that the department intends to adjust a pending refund against an outstanding tax demand. Taxpayers have the right to respond within 30 days before the adjustment is made.

Section 156 – Demand Notice

A Section 156 demand notice is issued after an assessment creates a tax liability. Taxpayers must pay the demanded amount within 30 days to avoid further consequences.

Income Tax Notice Time Limits (2026)

Notice Section

What It Covers

Time Limit

Section 143(1)

CPC Processing Intimation

Within 9 Months from End of AY

Section 143(2)

Scrutiny Selection

Within 3 Months from End of FY of Filing

Section 142(1)

Pre-Assessment Inquiry

During Assessment Proceedings

Section 148 (≤ ₹50 Lakh)

Reassessment — Smaller Cases

Up to 3 Years from End of AY

Section 148 (> ₹50 Lakh)

Reassessment — Larger Cases

Up to 10 Years from End of AY

Section 245

Refund Adjustment

Before the Refund is Released

Section 156

Demand Notice

After Assessment Completion

How to Check Income Tax Notice Online

All notices issued after October 2019 are delivered electronically through the e-filing portal. The electronic delivery date is the legally valid service date.

Go to incometax.gov.in and log in with your PAN and password.

Navigate to Pending Actions → e-Proceedings.

All pending notices and response deadlines will be listed.

To verify a notice using its DIN: use the Verify Notice/Order Issued by ITD tool on the portal no login required.

Check your registered email and portal mailbox for intimations.

Any notice without a valid DIN is not legally valid. Verify before responding or paying.

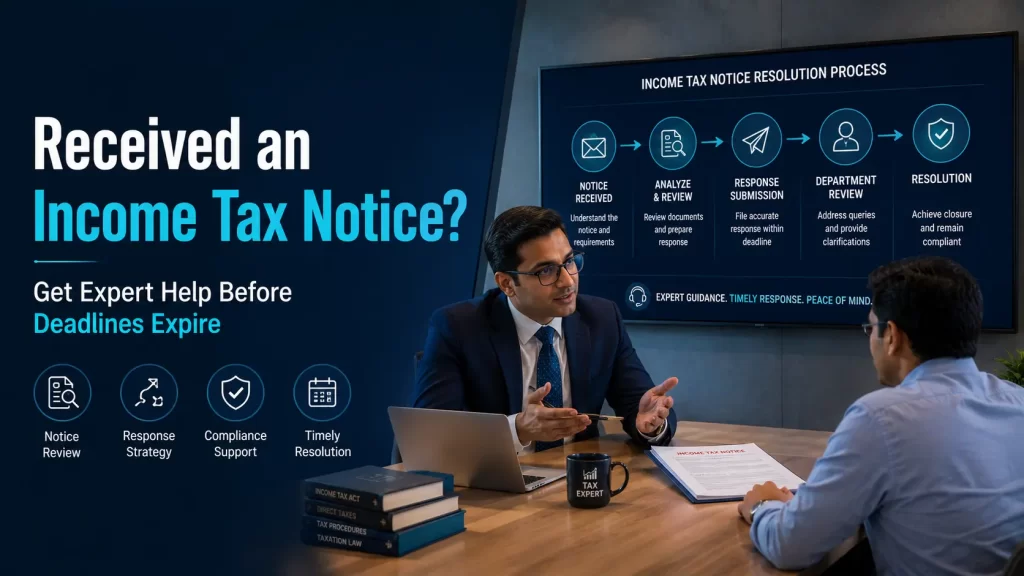

What to Do When You Receive an Income Tax Notice

Do not panic many notices are routine processing intimations.

Read the notice to identify exactly what is being asked.

Note the response deadline missing it can result in assessment under Section 144.

Gather all relevant documents: Form 16, Form 26AS, AIS, bank statements, investment certificates.

Respond through the e-filing portal: log in → e-Proceedings → select the notice → submit response.

Consult a Chartered Accountant for scrutiny notices, 148 notices, or large tax demands.

TIS is the deduplicated, category-wise summary derived from AIS. It removes duplicate entries, consolidates income into categories, and generates an “accepted value” after your feedback. The TIS accepted value is what pre-fills your ITR and what the CPC compares against your filed figures. Understanding these income tax notice details is essential because mismatches between TIS, AIS, Form 26AS, and your ITR are among the most common income tax notice reasons. Such discrepancies can trigger an income tax notice for salaried employees or an income tax notice for a salaried individual, while significant reporting differences may lead to an income tax notice under Section 142(1) seeking further information or an income tax notice under Section 148A for ITR-related issues where the department suspects income has escaped assessment.

Income Tax Notice Prevention Checklist (AY 2026-27)

Before filing your ITR, complete each of these steps:

Download AIS and review every line item

Submit AIS feedback for incorrect or duplicate entries

Download Form 26AS and verify every TDS entry against Form 16 and Form 16A

Reconcile salary from all employers (if you changed jobs)

Report all interest income: savings, FD, bonds, post office

Declare all dividend income check AIS for all company dividends

Report all capital gains equity, debt funds, property, gold

Fill Schedule VDA if you had any cryptocurrency transactions

Fill Schedule FA if you hold any foreign assets

Back every deduction (80C, 80D, 80G) with supporting documents

Document the source of funds for any high-value transaction

Prepare a GST ITR turnover reconciliation if applicable

Verify your ITR form choice is correct for your income type

File on time late filing can itself trigger notices

Frequently Asked Questions (FAQs)

Can I ignore an income tax notice?

No. Ignoring a notice leads to best judgement assessment under Section 144, penalties, interest, and possible prosecution. Always respond within the deadline.

Can salaried employees receive scrutiny notices?

Yes. Salary income mismatches frequently trigger scrutiny.

What is DIN in an income tax notice?

DIN is the Document Identification Number used to verify authenticity.

Can an AIS mismatch trigger a notice?

Yes. AIS mismatches are among the most common notice triggers.

Can I correct mistakes after receiving a notice?

In many cases, taxpayers can respond, rectify, or revise information depending on the notice type.

What is the income tax notice time limit for scrutiny?

A Section 143(2) scrutiny notice must be issued within 3 months from the end of the financial year in which the return was filed. For AY 2025-26, the deadline is 30 June 2026.

How do I check income tax notice online?

Log in to incometax.gov.in → Pending Actions → e-Proceedings. All pending notices appear here. Use the “Verify Notice/Order” tool to verify authenticity by DIN without logging in.

What is the time limit under Section 148?

For escaped income up to ₹50 lakh: up to 3 years from end of AY. For escaped income above ₹50 lakh: up to 10 years.

TIS is the deduplicated, category-wise summary derived from AIS. It removes duplicate entries, consolidates income into categories, and generates an “accepted value” after your feedback. The TIS accepted value is what pre-fills your ITR and what the CPC compares against your filed figures. Understanding these income tax notice details is essential because mismatches between TIS, AIS, Form 26AS, and your ITR are among the most common income tax notice reasons. Such discrepancies can trigger an income tax notice for salaried employees or an income tax notice for a salaried individual, while significant reporting differences may lead to an income tax notice under Section 142(1) seeking further information or an income tax notice under Section 148A for ITR-related issues where the department suspects income has escaped assessment.

Conclusion

Income tax notices in India today are generated by automated systems. The CPC and Insight Portal ingest data from banks, employers, brokers, mutual fund companies, crypto exchanges, and registrars. Every transaction above a reporting threshold appears in your AIS. Every TDS credit is checked against Form 26AS. Any gap between these sources and your ITR can generate a notice without any human reviewing your case.

The most effective defence is a disciplined pre-filing reconciliation routine: download AIS and TIS, check every income item, verify every tax credit in Form 26AS, and document the source of any large transaction. Taxpayers who make this an annual habit are significantly less likely to receive notices and far better prepared to respond when one arrives.